Morning Call For September 30, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps are up sharply by +1.23% and European stocks are up +2.53% as a rally in copper boosted miners and commodity producers. Also a rally in China's Shanghai Composite reduced Chinese economic concerns. European automakers rose, with Peugeot Citroen up over 6%, after China said it will cut the purchase tax in half on certain vehicles. Asian stocks settled higher: Japan +2.70%, Hong Kong +1.41%, China +0.48%, Taiwan +0.60%, Australia +2.10%, Singapore +0.11%, South Korea +1.25%, India +1.46%.

The dollar index is up +0.25%. EUR/USD is down -0.23% on the prospects for additional ECB stimulus after Eurozone Sep CPI unexpectedly fell for the first time in 6 months. USD/JPY is up +0.40%.

Dec T-note prices are down -13 ticks as the sharp rally in stocks reduces the safe-haven demand of government debt.

In an attempt to spur demand in China's housing market, the PBOC cut the minimum down payment for buyers in cities without property restrictions to 25% from 30%.

The Eurozone Sep CPI estimate unexpectedly fell -0.1% y/y, weaker than expectations of unch y/y and the first decline in 6 months. The Sep core CPI rose +0.9% y/y, right on expectations.

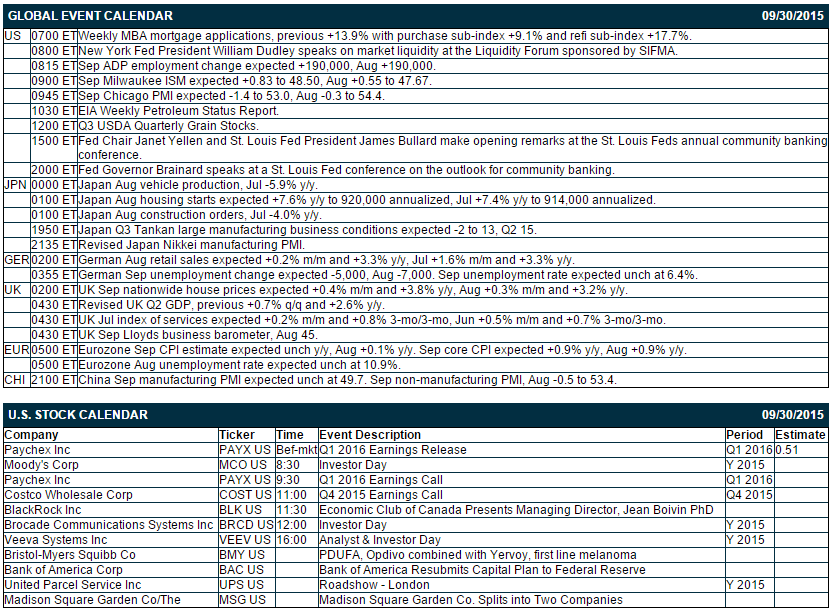

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +13.9% with purchase sub-index +9.1% and refi sub-index +17.7%), (2) Sep ADP employment (expected +190,000, Aug +190,000), (3) Sep Milwaukee ISM (expected +0.83 to 48.50, Aug +0.55 to 47.67), (4) Sep Chicago PMI (expected -1.4 to 53.0, Aug -0.3 to 54.4), (5) New York Fed President William Dudley's speech on market liquidity at the Liquidity Forum sponsored by SIFMA, (6) opening remarks by Fed Chair Janet Yellen and St. Louis Fed President James Bullard at the St. Louis Fed’s annual community banking conference, and (7) Fed Governor Brainard's speech at a St. Louis Fed conference on the outlook for community banking.

There is 1 of the Russell 2000 companies that report earnings today: Paychex (consensus $0.51).

U.S. IPO's scheduled to price today include: Performance Food Group (PFGC), Ardelyx (ARDX), Innovation Economy Group (MYIE), Accelerize (ACLZ), NovaBay Pharmaceuticals (NBY).

Equity conferences this week include: Johnson Rice & Co Energy Conference on Mon-Wed, Wolfe Research Power and Gas Leaders Conference on Tue-Wed, D. A. Davidson & Co Engineering & Construction Conference on Wed, Leerink Partners Rare Disease Roundtable Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Verifone Systems (PAY +1.47%) was raised to 'Buy' from 'Hold' at Argus with a price target of $35.

Bank of America reinstated Valeant Pharmaceuticals (VRX -5.06%) with a 'Buy' and a price target of $290.

HSBC (HSBC -0.30%) was upgraded to 'Buy' from 'Neutral' at UBS.

Novavax (NVAX -21.35%) climbed over 3% in after-hours trading after the company said a Phase 1 study of its RSV F vaccine shows it was safe in healthy children.

Ralph Lauren (RL -0.79%) gained almost 4% in after-hours trading after CEO Ralph Lauren said he will step down and hand the job over to Old Navy President Stefan Larsson.

The Gap (GPS +0.30%) fell 4% in pre-market trading after UBS downgraded the stock to 'Sell' from 'Neutral' on the pending departure of Old Navy President Stefan Larsson.

Dealertrack Technologies (TRAK +0.10%) rose nearly 2% in after-hours trading after the U.S. Attorney General said that Cox Automotive can buy the company on the condition it divests an inventory management unit to preserve competition.

Donaldson (DCI +0.26%) dropped over 6% in after-hours trading after the company said it will delay its 10-K filing after two ex-employees reported that a European gas turbine project improperly recognized revenue.

Barracuda Networks (CUDA -4.38%) slumped over 15% in after-hours trading after it reported Q2 adjusted EPS of 10 cents, higher than consensus of 9 cents, but reported Q2 revenue of $78.4 million, below consensus of $78.7 million, and said that it sees "some evidence that growth in the overall storage market has slowed."

Clovis (CLVS -1.67%) climbed nearly 3% in after-hours trading after it said the FDA and EMA will expedite reviews of its rociletinib drug for the treatment of non-small cell lung cancer.

Diamond Foods (DMND -1.97%) fell over 4% in after-hours trading after it reported Q4 adjusted EPS of 23 cents, better than consensus of 21 cents, but Q4 sales of $201.8 million were below expectations of $209.8 million.

Clarcor (CLC -0.21%) boosted its quarterly dividend to 22 cents a share from 20 cents a share, below consensus for an increase to 23 cents a share.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 +1.33%) this morning are up +23.00 points (+1.23%). Tuesday's closes: S&P 500 +0.12%, Dow Jones +0.30%, Nasdaq-0.49%. The S&P 500 on Tuesday recovered from a 1-month low and closed slightly higher on the unexpected +1.7 point increase in U.S. Sep consumer confidence to an 8-month high of 103.0, stronger than expectations of -4.7 to 96.8, and on strength in energy and commodity producers as crude oil and copper moved higher. Stocks were undercut by negative carryover from a 2% slide in China's Shanghai Composite and a -0.70% fall in European stocks on global growth concerns, and by the unexpected -0.2% m/m decline in the Jul S&P CaseShiller composite-20 home price index.

Dec 10-year T-notes (ZNZ15 -0.32%) this morning are down -13 ticks. Tuesday's closes: TYZ5 +12.00, FVZ5 +6.75. Dec T-notes on Tuesday rose to a 1-month high and settled higher on carryover support from a rally in German bunds to a 1-month high on speculation the ECB may boost QE to fight deflation risks after German Sep CPI fell -0.2% y/y, the fastest pace of decline in 8 months. T-notes also received a boost from the weaker-than-expected Jul S&P CaseShiller home price index.

The dollar index (DXY00 +0.31%) this morning is up +0.240 (+0.25%). EUR/USD (^EURUSD) is down -0.0026 (-0.23%). USD/JPY (^USDJPY) is up +0.48 (+0.40%). Tuesday's closes: Dollar Index -0.179 (-0.19%), EUR/USD +0.0005 (+0.04%), USD/JPY -0.18 (-0.15%). The dollar index on Tuesday closed lower on the weaker-than-expected U.S. Jul S&P CaseShiller composite-20 home price index, and on the -2.0% plunge in China's Shanghai Composite after the China Aug leading index fell to a 6-1/2 year low, which bolsters speculation that the recent meltdown in China will undercut global growth and further delay a Fed interest rate hike. The dollar recovered from its worst levels after U.S. Sep consumer confidence unexpectedly rose to an 8-month high.

Nov crude oil (CLX15 -0.31%) this morning is down -16 cents (-0.35%) and Nov gasoline (RBX15 -0.51%) is down -0.0092 (-0.68%). Tuesday's closes: CLX5 +0.80 (+1.80%), RBX5 -0.0094 (+0.71%). Nov crude oil and gasoline prices on Tuesday closed higher on improvement in global economic outlook after an unexpected increase in U.S. Sep consumer confidence to an 8-month high and an increase in Eurozone Sep economic confidence to a 4-year high. Crude oil prices also received a boost from the weaker dollar and expectations that Wednesday's weekly EIA data will show U.S. crude inventories fell -500,000 bbl.

Disclosure: I have no positions in ...

more