Morning Call For October 27, 2016

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 +0.21%) are up +0.16% and European stocks are down -0.06%. Global government bond markets sold-off on speculation central banks will become less accommodative as the economy strengthens. The 10-year UK Gilt yield surged to a 4-month high of 1.242% after UK Q3 GDP grew more than expected. That fueled a sell-off in German bund prices to a 4-1/2 month low and helped push U.S. Dec 10-year T-notes down to a 2-week low. Equity losses were limited as mining stocks and raw-material producers gained as the price of copper (HGZ16 +0.77%) jumped to a 2-week high on signs of tighter supplies after LME copper inventories tumbled -4,775 MT to a 1-1/2 month low of 331,450 MT. Increased M&A activity is another positive for stocks after Qualcomm agreed to buy NXP Semiconductors for $47 billion. Asian stocks settled mostly lower: Japan -0.32%, Hong Kong -0.83%, China -0.13%, Taiwan 0.67%, Australia -1.20%, Singapore +0.01%, South Korea +0.45%, India +0.29%.

The dollar index (DXY00 -0.09%) is down -0.10%. EUR/USD (^EURUSD) is up +0.16%. USD/JPY (^USDJPY) is up +0.23%.

Dec 10-year T-note prices (ZNZ16 -0.26%) are down -10.5 ticks at a 2-week low.

UK Q3 GDP rose +0.5% q/q and +2.3% y/y, stronger than expectations of +0.3% q/q and +2.1% y/y.

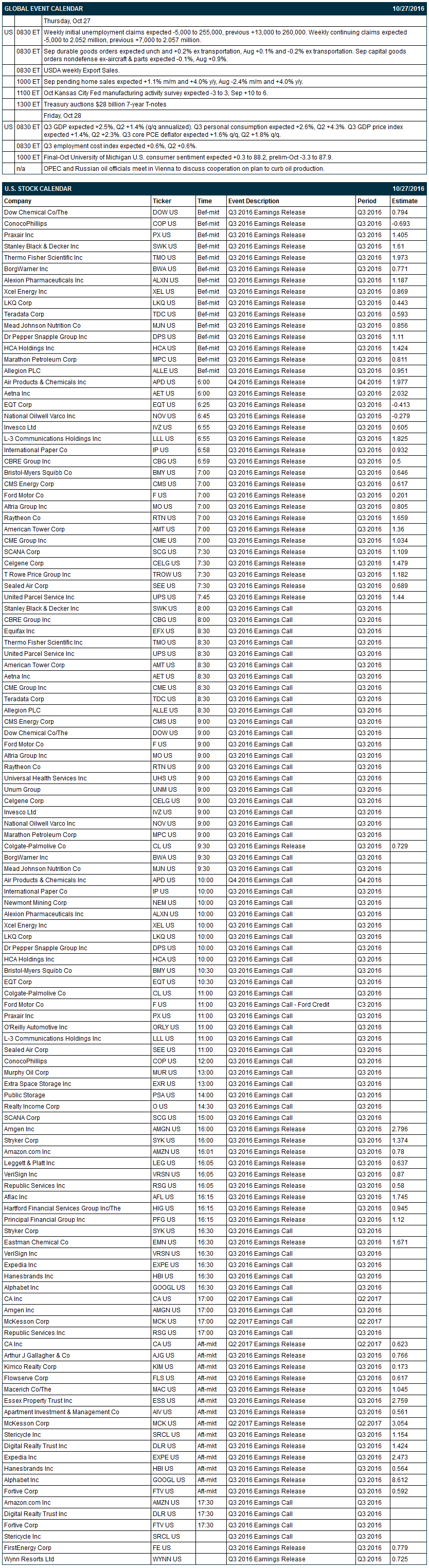

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -5,000 to 255,000, previous +13,000 to 260,000) and continuing claims (expected -5,000 to 2.052 million, previous +7,000 to 2.057 million), (2) Sep durable goods orders (expected unch and +0.2% ex transportation, Aug +0.1% and -0.2% ex transportation), (3) Sep pending home sales (expected +1.1% m/m and +4.0% y/y, Aug -2.4% m/m and +4.0% y/y), (4) Oct Kansas City Fed manufacturing activity survey (expected -3 to 3, Sep +10 to 6), (5) the Treasury's auction of $28 billion of 7-year T-notes, (6) USDA weekly Export Sales.

Notable S&P 500 earnings reports today include: Amazon.com (consensus $0.78), Alphabet (8.61), UPS ($1.44), Dow Chemical (0.79), ConocoPhillips (-0.69), Praxair (1.41), BorgWarner (0.77), Dr Pepper Snapple (1.11), Marathon Petroleum (0.81), National Oilwell Varco (-0.28), International Paper (0.93), Bristol-Myers Squibb (0.65), Ford (0.20), Raytheon (1.66), CME Group (1.03), T Rowe Price (1.18), Amgen (2.80), VeriSign (0.87), Aflac (1.75), Expedia (2.47).

U.S. IPO's scheduled to price today: Acushnet Holdings (GOLF), Quantenna Communications (QTNA), Blackline Inc (BL), Aytu Bioscience (AYTU).

Equity conferences during the remainder of this week include: American Cystic Fibrosis Conference on Thu, ARM TechCon on Thu.

OVERNIGHT U.S. STOCK MOVERS

NXP Semiconductors (NXPI -1.97%) rose over 2% in pre-market trading after Qualcomm agreed to buy the company for $110 a share or $47 billion, an 11% premium to Wednesday's closing price.

Tesla Motors (TSLA -0.05%) gained over 4% in after-hours trading after it reported an unexpected Q3 adjusted EPS profit of 71 cents, better than consensus of a -54 cent loss.

Cheesecake Factory (CAKE -0.47%) jumped 7% in after-hours trading after it reported Q3 adjusted EPS of 70 cents, above consensus of 61 cents.

F5 Networks (FFIV +1.98%) climbed 5% in after-hours trading after it reported Q4 adjusted EPS of $2.11, higher than consensus of $1.94, and said it sees Q1 adjusted EPS of $1.92-$1.95, higher than consensus of $1.87.

O'Reilly Automotive (ORLY -1.11%) slid 3% in after-hours trading after it lowered guidance on 2016 adjusted EPS to $10.58-$10.68, below consensus of $10.73.

Trinity Industries (TRN -0.62%) dropped 6% in after-hours trading after it said it sees Q4 EPS of 30-cents-40 cents, less than consensus of 43 cents, and said it sees first-half 2017 EPS 45 cents-60 cents versus $1.25 y/y.

Shutterfly (SFLY -0.90%) rallied 8% in after-hours trading after it reported a Q3 loss of -86 cents per share, a narrower loss than consensus of -95 cents.

Rent-A-Center (RCII +1.17%) dropped over 8% in after-hours trading after it cut guidance on full-year adjusted EPS to $1.05-$1.15 from a prior view of $1.65-$1.85.

Pilgrim’s Pride (PPC -1.15%) fell nearly 6% in after-hours trading after it reported Q3 adjusted EPS of 40 cents, weaker than consensus of 47 cents.

Ultra Clean Holdings (UCTT +2.17%) jumped nearly 9% in after-hours trading after it reported Q3 adjusted EPS of 17 cents, above consensus of 13 cents, and said it sees Q4 adjusted EPS of 17 cents-20 cents, higher than consensus of 11 cents.

Interface (TILE -0.32%) slid nearly 5% in after-hours trading after it reported Q3 EPS of 25 cents, below consensus of 32 cents.

Cimpress NV (CMPR +1.64%) dropped over 9% in after-hours trading after it reported Q1 gross margin of 51.8%, less than consensus of 54.4%.

Planet Fitness (PLNT +3.78%) rose 4% in after-hours trading after it reported Q3 adjusted EPS of 16 cents, higher than consensus of 14 cents, and then raised guidance on 2016 adjusted EPS to 66 cents-67 cents from an August 11 view of 63 cents-66 cents.

Essendant (ESND -0.21%) tumbled 12% in after-hours trading after it reported Q3 adjusted EPS of 57 cents, weaker than consensus of 68 cents, and then cut guidance on 2016 adjusted EPS to $1.75-$1.90 from a prior view of $2.15-$2.30.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 +0.21%) this morning are up +3.50 points (+0.16%). Wednesday's closes: S&P 500 -0.17%, Dow Jones +0.17%, Nasdaq -0.63%. The S&P 500 on Wednesday closed lower on weakness in technology stocks led by a 2% decline in Apple after it forecasted an uninspiring holiday sales outlook. There was also weakness in energy producer stocks after the price of crude oil fell to a 3-week low. Stocks found underlying support from news that the U.S. Oct Markit services PMI rose +2.5 to an 11-month high of 54.8, stronger than expectations of +0.2 to 52.5.

Dec 10-year T-notes (ZNZ16 -0.26%) this morning are down -10.5 ticks at a 2-week low. Wednesday's closes: TYZ6 -7.50, FVZ6 -3.50. Dec 10-year T-notes on Wednesday fell to a 1-week low and closed lower on the stronger-than-expected increase in the U.S. Oct Markit services PMI to an 11-month high that bolstered the case for a Fed rate hike. T-notes were also undercut by increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 5-3/4 month high.

The dollar index (DXY00 -0.09%) this morning is down -0.102 (-0.10%). EUR/USD (^EURUSD) is up +0.0017 (+0.16%). USD/JPY (^USDJPY) is up +0.24 (+0.23%). Wednesday's closes: Dollar index -0.090 (-0.09%), EUR/USD +0.0019 (+0.17%), USD/JPY +0.25 (+0.24%). The dollar index on Wednesday closed lower on the weaker-than-expected U.S. Sep new home sales report and on strength in EUR/USD after Tuesday's data showed the German Oct IFO business climate index unexpectedly rose to a 2-1/2 year high.

Dec WTI crude oil (CLZ16 +0.49%) this morning is up +22 cents (+0.45%) and Dec gasoline (RBZ16 +0.61%) is up +0.0113 (+0.77%). Wednesday's closes: Dec crude -0.78 (-1.56%), Dec gasoline -0.0089 (-0.60%). Dec crude oil and gasoline on Wednesday closed lower with Dec crude at a 3-week low and Dec gasoline at a 1-1/2 week low. Crude oil prices were undercut by doubts about whether OPEC can find support for a cut in oil production after Russia said it favors a freeze in output but not a cut in production. Crude oil prices were also undercut by the +0.5% increase in U.S. crude production in the week of Oct 21. Crude oil and gasoline prices found support on the EIA report that showed an unexpected -553,000 bbl decline in EIA crude inventories to a 9-month low (versus expectations of +1.75 million bbl) and a -1.337 million bbl decline in crude supplies at Cushing to an 11-month low.

(Click on image to enlarge)

Disclosure: None.