Morning Call For November 9, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 -0.32%) are down -0.33% and European stocks are down -0.42 % on global growth concerns after the OECD cut its global GDP forecasts for this year and next, and after China Oct exports and imports declined more than expected. Asian stocks settled mixed: Japan +1.96%, Hong Kong -0.61%, China +1.58%, Taiwan -0.59%, Australia -1.83%, Singapore -0.42, South Korea -0.42%, India -0.55%. China's Shanghai Composite climbed to a 2-1/2 month high as a government plan to resume initial public offerings by the end of the year boosted brokerages, and Japan's Nikkei Stock Index also rose to a 2-1/2 month high as exporters rallied on improved earnings prospects after the yen fell to a 2-1/2 month low against the dollar.

The dollar index (DXY00 -0.29%) is down -0.28%. EUR/USD (^EURUSD) is up +0.41% after a gauge of Eurozone investor confidence rose more than expected. USD/JPY (^USDJPY) is up +0.26% at a 2-1/2 month high.

Dec T-note prices (ZNZ15 -0.09%) are down -4 ticks.

The OECD cut its global economic forecast for the second time in three months as it cut its global 2015 GDP estimate to 2.9% from a Sep forecast of 3.0%, and cut its 2016 global GDP forecast to 3.3% from a Sep estimate of 3.6%.

The Eurozone Nov Sentix investor confidence rose +3.4 to 15.1, stronger than expectations of +1.4 to 13.1.

The China Oct trade balance widened to a record surplus of +$61.64 billion, less than expectations of +$62.00 billion. Oct exports fell -6.9% y/y, more than expectations of -3.2% y/y and the fourth straight month of declines. Oct imports fell -18.8% y/y, more than expectations of -15.2% y/y and the twelfth consecutive month of declines.

U.S. STOCK PREVIEW

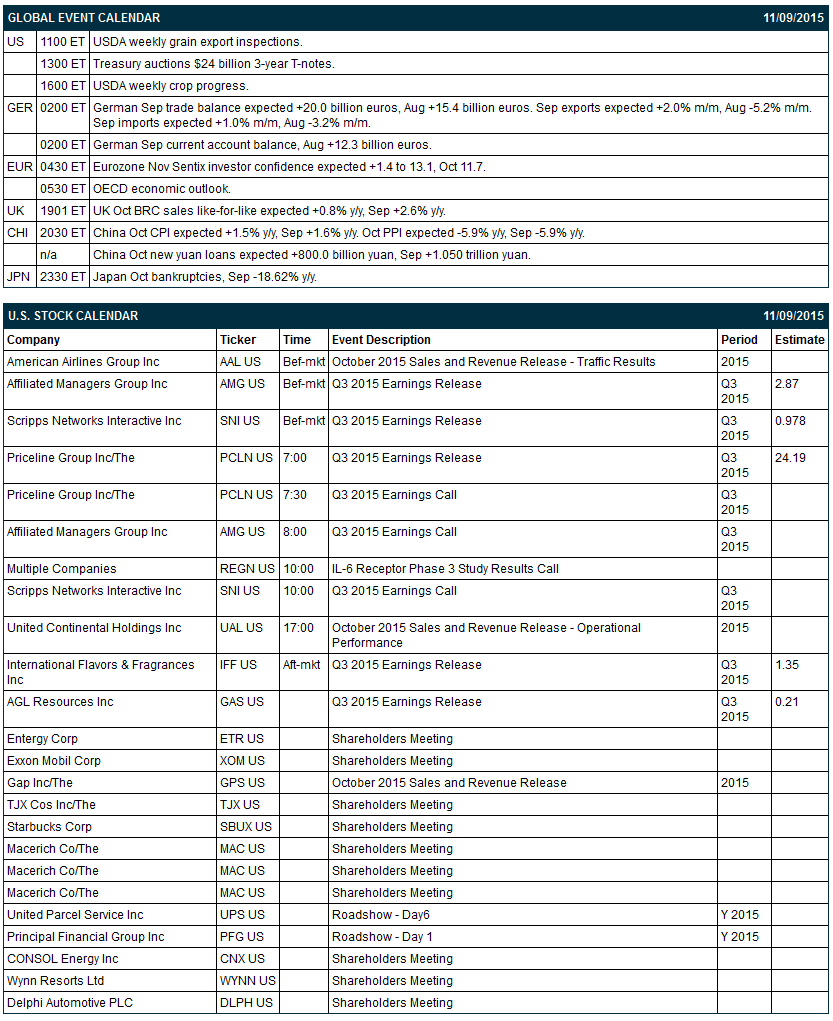

Key U.S. news today includes: (1) the Treasury's auction of $24 billion 3-year T-notes.

There are 5 of the S&P 500 companies that report earnings today: Priceline (consensus $24.19), Affiliated Managers Group (2.87), Scripps Networks Interactive (0.98), International Flavors and Fragrances (1.35), AGL Resources (0.21).

U.S. IPO's scheduled to price today: Xtera Communications (XCOM), GenSight Biologics (GNST).

Equity conferences today include: Mitsubishi UFJ Energy Tour-Houston on Mon, Morgan Stanley Global Chemicals & Agriculture Conference on Mon-Tue, Baird Healthcare Conference on Mon-Wed, Edison Electric Institute Financial Conference on Mon-Wed, Robert W. Baird & Co. Industrial Conference on Mon-Wed, Citi Financial Technology Conference on Tue, J.P. Morgan Ultimate Services Investor Conference on Tue, Mizuho Securities Technology Corporate Access Day on Tue, Mitsubishi UFJ Securities: Healthcare Conference - Seattle on Tue, Bank of America Merrill Lynch Global Energy Conference on Tue-Wed, Credit Suisse Boston Financials Conference on Tue-Wed, Credit Suisse Health Care Conference on Tue-Wed, Wells Fargo Securities Technology, Media and Telecom Conference on Tue-Wed, RBC Capital Markets Technology, Internet, Media and Telecommunications Conference on Tue-Wed, Stephens Inc Fall Investment Conference on Tue-Wed, Jefferies Energy Conference on Wed, UBS Building & Building Products CEO Conference on Wed.

OVERNIGHT U.S. STOCK MOVERS

Alcoa (AA -1.20%) was downgraded to 'Neutral' from 'Buy' at Nomura.

Priceline Group (PCLN -0.87%) reported Q3 adjusted EPS of $25.35, better than consensus of $24.19.

Scripps Networks Interactive (SNI +1.34%) reported Q3 EPS of $1.06, higher than consensus of 98 cents.

Affiliated Managers Group (AMG +0.89%) reported Q3 EPS of $2.93, better than consensus of $2.87.

Sanofi (SNY -7.58%) was downgraded to 'Neutral' from 'Buy' at UBS.

Marathon Oil (MRO -3.74%) said it will sell some its Gulf of Mexico assets for $205 million.

Apache Corp. (APA -3.25%) jumped 11% in pre-market trading after it said it rejected an unsolicited $18 billion offer for the company.

Hertz GLobal (HTZ +4.27%) reported Q3 adjusted EPS of 49 cents, weaker than consensus of 52 cents.

Kronos Worldwide (KRO -0.37%) reported an unexpected Q3 EPS loss of -10 cents, weaker than consensus of a profit of 6 cents.

Weight Watchers (WTW +35.20%) rose 4% in after-hours trading after Point 72 Asset reported a 6.0% stake in the company.

BioCryst Pharmaceuticals (BCRX -4.28%) climbed nearly 4% in after-hours trading after Baker Bros. said they raised their stake in the company to 19.5% from 15.8%.

WhiteWave Foods (WWAV -0.96%) rose over 1% in after-hours trading on optimism over the company's Q3 earnings results that are expected before the opening of trading on Monday, Nov 9.

Acadia Pharmaceuticals (ACAD -11.53%) fell nearly 2% in after-hours trading after its Chief Medical Officer, Roger Mills, resigned.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 -0.32%) this morning are down -7.00 points (-0.33%). Friday's closes: S&P 500 -0.03%, Dow Jones +0.26%, Nasdaq +0.09%. The S&P 500 on Friday closed slightly lower on the increased odds for a Fed rate hike in December after the +271,000 increase in Oct non-farm payrolls, stronger than expectations of +185,000 and the largest increase in 10 months. In addition, energy producers sold off on a rally in the dollar index to a 6-3/4 month high, which pushed crude prices to a 1-week low. The main bullish factor was the record +$28.918 billion increase in Sep consumer credit, stronger than expectations of +$18.000 billion and a sign that consumers are confident enough in the economy to increase their debt load. Bank stocks rallied on speculation that an increase in interest rates will boost bank profits.

Dec 10-year T-notes (ZNZ15 -0.09%) this morning are down -4 ticks. Friday's closes: TYZ5 -25.00, FVZ5 -14.25. Dec T-notes on Friday slumped to a 3-1/2 month nearest-futures low and closed lower on the larger-than-expected increase in U.S. Oct non-farm payrolls and on the larger-than-expected increase in U.S. Oct average hourly earnings which bolsters the likelihood that the Fed will raise interest rates at December's FOMC meeting.

The dollar index (DXY00 -0.29%) this morning is down -0.279 (-0.28%). EUR/USD (^EURUSD) is up +0.0044 (+0.41%). USD/JPY (^USDJPY) is up +0.32 (+0.26%) at a fresh 2-1/2 month high. Friday's closes: Dollar Index +1.232 (+1.26%), EUR/USD +0.0143 (-1.31%), USD/JPY +1.38 (+1.13%). The dollar index on Friday surged to a 6-3/4 month high and closed higher on increased expectations for a December FOMC rate hike after the stronger-than-expected U.S. Oct payroll report. In addition, EUR/USD tumbled to a 6-1/2 month low on speculation the ECB may expand QE after German Sep industrial production unexpectedly fell by the most in 13 months.

Dec crude oil (CLZ15 +1.29%) this morning is up +61 cents (+1.38%) and Dec gasoline (RBZ15 +1.93%) is up +0.0284 (+2.07%). Friday's closes: CLZ5 -0.68 (-1.50%), RBZ5 +0.0139 (+1.02%). Dec crude oil and gasoline prices on Friday settled mixed with Dec crude at a 1-week low. Crude oil prices were undercut by the surge in the dollar index to a 6-3/4 month high and by the ongoing U.S. crude supply glut with U.S. crude inventories more than 100 million bbls above the 5-year seasonal average. Gasoline moved higher on speculation fuel demand will increase with the strength in the economy.

(Click on image to enlarge)

Disclosure:None.