Morning Call For November 25, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 +0.25%) are up +0.24% and European stocks are up +1.13% as markets shrug off the geopolitical risks from the Middle East and focus on signs that the U.S. economy is strong enough to handle the first Fed interest rate increase since 2006. NATO and U.S. President Obama called on Russia and Turkey to deescalate tensions and focus instead on destroying jihadist groups. Commodities moved lower as the dollar index strengthened to an 8-1/4 month high, while the yield on the German 10-year bund fell to a 3-1/2 week low of 0.463% on the prospects of additional stimulus from the ECB. Asian stocks settled mostly lower: Japan -0.39%, Hong Kong -0.40%, China +0.88%, Taiwan -0.17%, Australia-0.63%, Singapore -1.09%, South Korea -0.38%, India closed for holiday. Weakness in commodity prices undercut most Asian miners and raw-material producers, while Japanese exporters fell as geopolitical risks from the Middle East fueled increased safe-haven demand for the yen and reduced the profit outlook for Japanese exporters.

The dollar index (DXY00 +0.48%) is up +0.50% at an 8-1/4 month high on the outlook for a Fed rate hike next month. EUR/USD (^EURUSD) is down-0.44% at a 7-1/4 month low as speculation mounts that the ECB will boost monetary easing when it meets next Thursday. USD/JPY (^USDJPY) is up +0.11%.

Dec T-note prices (ZNZ15 +0.05%) are up +3.5 ticks on carryover support from as a rally in 10-year German bunds to a 3-1/2 week high.

In its bi-annual Financial Stability Review, the ECB warned that "highly indebted foreign-currency borrowers may be vulnerable to a prospective normalization of financial conditions in the U.S. and other advanced economies" and that "a faster than expected withdrawal of monetary policy accommodation in other major advanced economies could trigger a reversal of global term premia, which may also spill over to the Eurozone."

U.S. STOCK PREVIEW

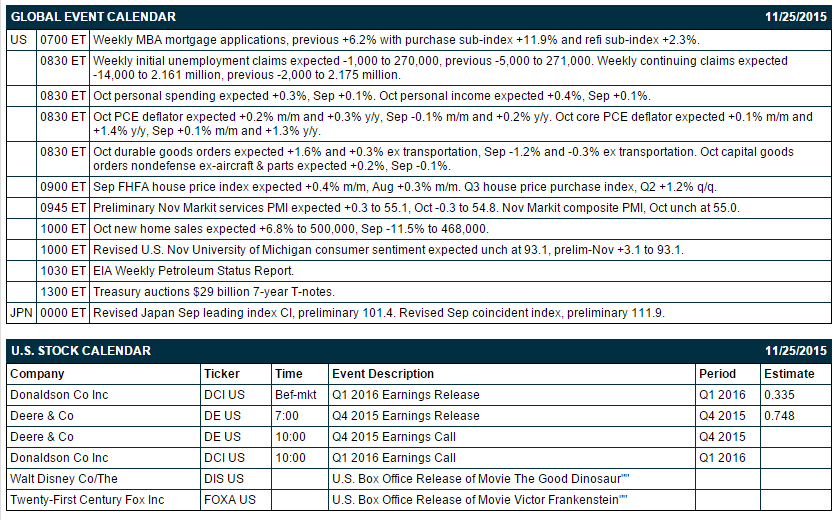

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +6.2% with purchase sub-index +11.9% and refi sub-index +2.3%), (2) weekly initial unemployment claims (expected -1,000 to 270,000, previous -5,000 to 271,000) and continuing claims (expected -14,000 to 2.161 million, previous -2,000 to 2.175 million), (3) Oct personal spending (expected +0.3%, Sep +0.1%) and Oct personal income (expected +0.4%, Sep +0.1%), (4) Oct PCE deflator (expected +0.2% m/m and +0.3% y/y, Sep -0.1% m/m and +0.2% y/y) and Oct core PCE deflator (expected +0.1% m/m and +1.4% y/y, Sep +0.1% m/m and +1.3% y/y), (5) Oct durable goods orders (expected +1.6% and +0.3% ex transportation, Sep -1.2% and -0.3% ex transportation), (6) Sep FHFA house price index (expected +0.4% m/m, Aug +0.3% m/m), (7) preliminary-Nov Markit U.S. services PMI (expected +0.3 to 55.1, Oct -0.3 to 54.8), (8) Oct new home sales (expected +6.8% to 500,000, Sep -11.5% to 468,000), (9) the final-Nov U.S. consumer sentiment index from the University of Michigan (expected -0.1 to 93.0, prelim-Nov +3.1 to 93.1), (10) the Treasury's auction of $29 billion 7-year T-notes, and (11) EIA Weekly Petroleum Status Report.

There are 2 of the S&P 500 companies that report earnings today: Donaldson Co (consensus $0.34), Deere (0.75).

U.S. IPO's scheduled to price today: none.

Equity conferences this week include: INTERGAS VII Oil, Gas & Petrochemicals Conference & Exhibition on Wed.

OVERNIGHT U.S. STOCK MOVERS

Deere & Co. (DE +2.32%) jumped nearly 5% in pre-market trading after it reported Q4 EPS of $1.08, higher than consensus of 75 cents.

Hormel Foods (HRL +2.97%) was raised to 'Overweight' from 'Equal weight' at Stephens.

SunEdison (SUNE +37.33%) dropped over 7% in pre-market trading after it was downgraded to 'Sell' from 'Neutral' at UBS.

Terraform Power (TERP +5.50%) was cut to 'Sell' from 'Neutral' at UBS.

Valspar (VAL +2.25%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Caleres (CAL -0.48%) reported Q3 adjusted EPS of 80 cents, higher than consensus of 78 cents.

TiVo (TIVO +1.20%) fell almost 1% in after-hours trading after it reported Q3 EPS of 6 cents, below consensus of 8 cent, although Q3 net revenue of $132.3 million was higher than consensus of $123.3 million.

Hewlett Packard (HPQ +2.88%) slid nearly 8% in after-hours trading after it said it sees Q1 adjusted EPS of 33 cents-38 cents, below consensus of 42 cents, and then lowered guidance on fiscal 2016 adjusted EPS to $1.59-$1.69 from an earlier estimate of $1.67-$1.77.

Hewlett Packard Enterprise (HPE -1.16%) rose nearly 2% in after-hours trading after it reported Q4 pro forma revenue of $14.1 billion, higher than consensus of $13.5 billion.

Guess (GES +2.14%) climbed over 7% in after-hours trading after it reported Q3 adjusted EPS of 15 cents, higher than consensus of 11 cents, and then raised he lower end of its fiscal 2016 EPS estimate to 93 cents-$1.02 from a previous estimate of 89 cents-$1.02.

Pinnacle Foods (PF -1.46%) agreed to buy Boulder Brands (BDBD +8.44%) for about $710 million.

Veeva Systems (VEEV +0.51%) rose nearly 5% in after-hours trading after it reported Q3 adjusted EPS o 12 cents, better than consensus of 11 cents, and said it sees Q4 adjusted EPS of 11 cents, higher than consensus of 10 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 +0.25%) this morning are up +5.00 points (+0.24%). Tuesday's closes: S&P 500 +0.12%, Dow Jones +0.11%, Nasdaq -0.12%. The S&P 500 on Tuesday closed higher on strength in energy producers as crude oil rallied to a 1-week high and on the upward revision in U.S. Q3 GDP to +2.1% from +1.5%. Stock prices were undercut by heightened Middle East tensions after Turkey shot down a Russian warplane that violated its airspace and by the unexpected -8.7 point drop in the U.S. Nov consumer confidence (Conference Board) to 90.4, weaker than expectations of +1.9 to 99.5 and the lowest in 14 months.

Dec 10-year T-notes (ZNZ15 +0.05%) this morning are up +3.5 ticks. Tuesday's closes: TYZ5 +3.00, FVZ5 +2.50. Dec T-notes on Tuesday jumped to a 2-1/2 week high and closed higher on a rally in global government bond markets on increased safe-haven demand after Tukey shot down a Russian warplane on its Syrian border. T-notes also found support on the unexpected decline in U.S. Nov consumer confidence to a 14-month low. T-note prices were undercut by supply pressures during this week's $103 billion T-note auction package.

The dollar index (DXY00 +0.48%) this morning is up +0.493 (+0.50%) at an 8-1/4 month high. EUR/USD (^EURUSD) is down -0.0047 (-0.44%) at a 7-1/4 month low. USD/JPY (^USDJPY) is up +0.13 (+0.11%). Tuesday's closes: Dollar Index -0.276 (-0.28%), EUR/USD +0.0007 (+0.07%), USD/JPY-0.31 (-0.25%). The dollar index on Tuesday closed lower on the fall in USD/JPY to a 1-week low on increased safe-haven demand for the yen as geopolitical risks rose after Turkey shot down a Russian warplane. The dollar was also undercut by the unexpected decline in U.S. Nov consumer confidence to a 14-month low.

Jan crude oil (CLF16 -1.84%) this morning is down -59 cents (-1.38%) and Jan gasoline (RBF16 -2.61%) is down -0.0280 (-2.06%). Tuesday's closes: CLF6 +0.90 (+2.16%), RBF6 +0.0619 (+4.81%). Jan crude oil and gasoline on Tuesday closed higher with Jan crude at a 1-week high and Jan gasoline at a 1-1/2 week high. Crude oil prices received a boost from the weaker dollar and from Turkey's action in shooting down a Russian warplane near its border with Syria, which bolsters concern the conflict may spread and threaten crude shipments from the Middle East.

Disclosure:None.