Morning Call For November 24, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 -0.53%) are down -0.47% and European stocks are down -1.15% on heightened geopolitical risks in the Middle East after Turkey shot down a Russian military jet on its Syrian border. Turkey's state-run Anadolu News Agency said the Russian Su-24 jet was warned repeatedly after violating Turkish airspace before being shot down. NATO said it was watching the situation "closely" and Russian Foreign Minister Lavrov is scheduled to meet officials in Turkey tomorrow. On the positive side, German business confidence unexpectedly rose to the highest in 17 months. Asian stocks settled mixed: Japan +0.23%, Hong Kong -0.35%, China +0.16%, Taiwan -1.01%, Australia -0.95%, Singapore +0.69%, South Korea +0.65%, India -0.17%. China's Shanghai Composite closed higher after people familiar with the matter said China has canceled a rule requiring brokerages to hold daily long positions in their proprietary trading accounts, which should improve the earnings prospects of brokerages.

The dollar index (DXY00 -0.16%) is down -0.15%. EUR/USD (^EURUSD) is up +0.09%. USD/JPY (^USDJPY) is down -0.21% at a 1-week low as the yen strengthened on increased safe-haven demand as stocks fell on the downing of the Russian warplane.

Dec T-note prices (ZNZ15 +0.11%) are up +6.5 ticks at a 2-1/2 week high as government bonds climbed worldwide on increased safe-haven demand after Turkish forces on the Syrian border shot down a Russian warplane.

The German Nov IFO business climate rose +0.8 to 109.0, stronger than expectations of unch at 108.2 and the highest in 17 months.

U.S. STOCK PREVIEW

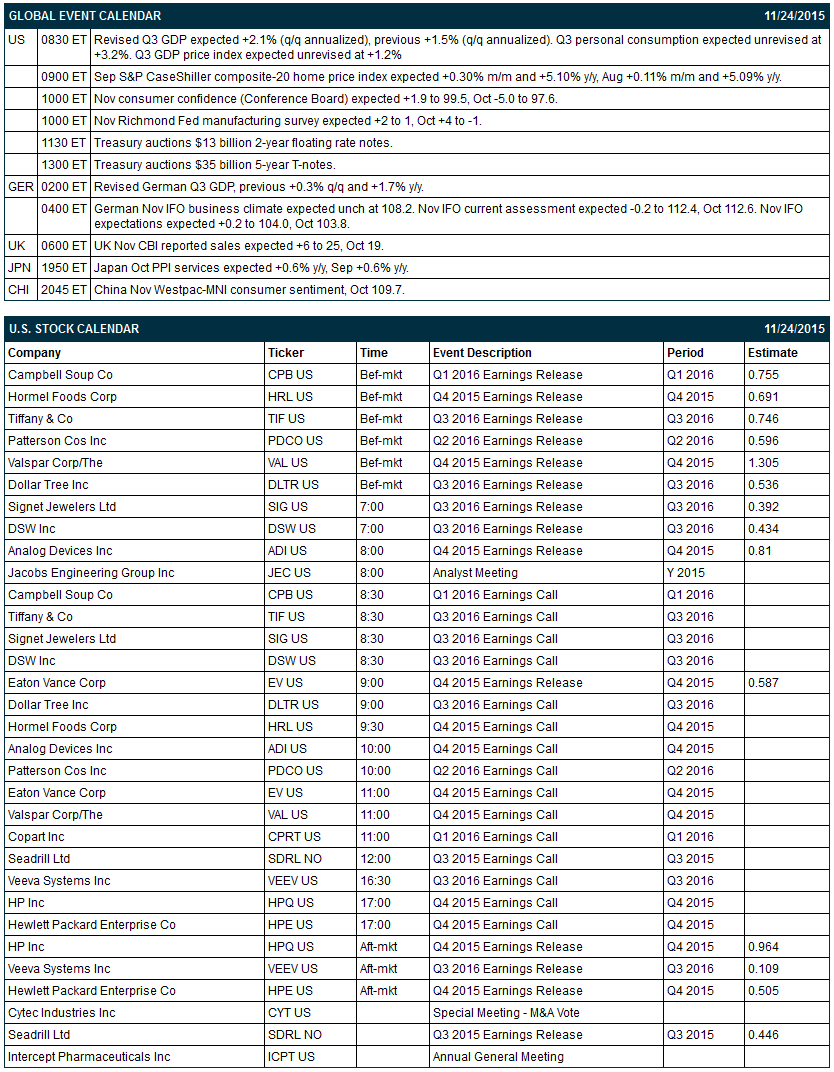

Key U.S. news today includes: (1) revised Q3 GDP (expected +2.1% q/q annualized vs previous +1.5%) and Q3 personal consumption (expected unrevised at +3.2%), (2) Sep S&P CaseShiller composite-20 home price index (expected +0.30% m/m and +5.10% y/y, Aug +0.11% m/m and +5.09% y/y), (3) Nov U.S. consumer confidence from the Conference Board (expected +1.9 to 99.5, Oct -5.0 to 97.6), (4) Nov Richmond Fed manufacturing survey (expected +2 to 1, Oct +4 to -1), and (5) the Treasury's auction of $13 billion of 2-year floating rate notes and $35 billion of 5-year T-notes.

There are 9 of the S&P 500 companies that report earnings today: HP (consensus $0.96), Campbell Soup (0.76), Hormel Foods (0.69), Tiffany (0.75), Patterson Companies (0.60), Dollar Tree (0.54), Signet Jewelers (0.39), Analog Devices (0.81).

U.S. IPO's scheduled to price today: Pampa Energia (PAM), QTS Realty Trust (QTS).

Equity conferences this week include: J.P. Morgan Asia Rising Dragons One-on-One Forum on Mon-Tue, INTERGAS VII Oil, Gas & Petrochemicals Conference & Exhibition on Wed.

OVERNIGHT U.S. STOCK MOVERS

Carnival Corp. (CCL -0.37%) and Royal Caribbean Cruises Ltd. (RCL +0.97%) both fell over 1% in pre-market trading after the U.S. State Department issued a global travel alert due to terror threats.

Tiffany & Co. (TIF +1.88%) reported Q3 EPS of 70 cents, below consensus of 75 cents.

Hormel Foods (HRL +1.60%) reported Q4 EPS of 74 cents, better than consensus of 69 cents.

CSRA Inc. will replace Computer Sciences (CSC +0.23%) in the S&P 500 after the close of trading on Friday, November 27.

Cubic (CUB +1.33%) reported Q4 adjusted EPS of 74 cents, below consensus of $1.00 and then lowered guidance on fiscal 2016 EPS to $1.30-$1.55, below consensus of $2.47.

Brocade Communication Systems (BRCD +2.44%) tumbled over 6% in after-hours trading after it reported Q4 adjusted EPS of 26 cents, better than consensus of 24 cents, but said it sees Q1 adjusted EPS of 23 cents-25 cents, weaker than consensus of 27 cents.

Xerox (XRX +2.77%) jumped more than 6% in after-hours trading after billionaire activist investor Carl Icahn said he has taken a 7.13% stake in the company.

Valeant Pharmaceuticals (VRX -3.95%) climbed nearly 3% in after-hours trading after Pershing Capital Management disclosed that it raised its stake in the company to 9.9% from 5.7%.

JM Smucker (SJM +0.12%) slid over 1% in after-hours trading after Tigress Financial Partners downgraded the stock to 'Neutral' from 'Buy.'

Dycom (DY +3.15%) reported Q1 adjusted EPS of $1.24, higher than consensus of $1.01, and said its sees Q2 revenue of $530 million-$550 million, above consensus of $527.6 million.

Post Holdings (POST -2.19%) declined over 1% in after-hours trading after it reported Q4 adjusted EPS of 6 cents, well below consensus of 26 cents.

Palo Alto (PANW +0.61%) rose over 3% in after-hours trading after it reported Q1 adjusted EPS of 35 cents, above consensus of 32 cents, and said it sees Q2 revenue of $314 million-$318 million, above consensus of $310.7 million.

Tarena International (TEDU +2.84%) gained over 5% in after-hours trading after it said it sees Q4 revenue of $54 million-$56 million, above consensus of $53.6 million.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 -0.53%) this morning are down -9.75 points (-0.47%). Monday's closes: S&P 500 +0.38%, Dow Jones +0.51%, Nasdaq +0.67%. The S&P 500 on Monday closed lower on the -3.4% decline in U.S. Oct existing home sales to 5.36 million (weaker than expectations of -2.7% to 5.40 million) and the -1.5 point drop in the preliminary U.S. Nov Markit manufacturing PMI to a 2-year low of 52.6 (weaker than expectations of -0.1 to 54.0). Stocks found support on increased M&A activity as the value of M&A deals done so far this year totals a record $3.42 trillion.

Dec 10-year T-notes (ZNZ15 +0.11%) this morning are up +6.5 ticks at a 2-1/2 week high. Monday's closes: TYZ5 +4.50, FVZ5 +1.25. Dec T-notes on Monday closed higher on the slide in stocks and the weaker-than-expected U.S Oct existing home sales and the preliminary U.S. Nov Markit manufacturing PMI reports. T-note prices were undercut, however, by hawkish comments from San Francisco Fed President Williams who said that there's a "strong case" for the Fed to raise inters rates next month.

The dollar index (DXY00 -0.16%) this morning is down -0.152 (-0.15%). EUR/USD (^EURUSD) is up +0.0010 (+0.09%). USD/JPY (^USDJPY) is down -0.26 (-0.21%) at a 1-week low. Monday's closes: Dollar Index +0.238 (+0.24%), EUR/USD -0.0010 (-0.09%), USD/JPY +0.03 (+0.02%). The dollar index on Monday climbed to a 7-1/4 month high and closed higher on the weekend comments from San Francisco Fed President Williams who said that there's a "strong case" for a Fed rate hike next month. In addition, EUR/USD slumped to a 7-1/4 month low on expectations for the ECB to boost stimulus measures at next week's ECB meeting.

Jan crude oil (CLF16 +1.49%) this morning is up +31 cents (+0.74%) and Jan gasoline (RBF16 +1.88%) is up +0.0175 (+1.36%). Monday's closes: CLF6 -0.15 (-0.36%), RBF6 +0.0294 (+2.32%). Jan crude oil and gasoline on Monday settled mixed. Crude oil prices received a boost from short covering after a story from the official Saudi Press Agency that said that Saudi Arabia says it's ready to cooperate with OPEC and non-OPEC producers to maintain stable oil prices. Crude oil prices were undercut by the rally in the dollar index to a 7-1/4 month high and by comments from Venezuelan Oil Minister Pino who said oil prices may slump to as low as the mid-$20s a barrel unless OPEC takes action to stabilize the market.

(Click on image to enlarge)

Disclosure:None.