Morning Call For November 11, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 +0.32%) are up +0.32% and European stocks are up +0.86% after China Oct retail sales rose by the most this year. Increased M&A activity is also supportive for stocks with SABMiller Plc up +1.7% after Anheuser-Busch InBev NV made a formal offer to buy it for about $107 billion. On the negative side is weakness in miners and raw-material producers after China Oct industrial production rose at the slowest pace in nearly 7 years, which sent Dec copper (HGZ15 -0.34%) down -0.32% to a 6-1/3 year low. Also, energy producers are weaker with Dec crude oil (CLZ15-1.31%) down -1.18% to a 2-week low. Asian stocks settled mixed: Japan +0.10%, Hong Kong -0.22%, China +0.27%, Taiwan -1.43%, Australia +0.46%, Singapore -0.54%, South Korea unch, India closed for holiday. Japan's Nikkei Stock Index climbed to a 2-1/2 month high on expectations for divergent central bank policies that weaken the yen to continue as the BOJ is expected to expand stimulus while the Fed is expected to raise interest rates. This will weaken the yen, which boosts the earnings prospects of Japanese exporters.

The dollar index (DXY00 -0.11%) is down -0.10%. EUR/USD (^EURUSD) is down -0.09%. USD/JPY (^USDJPY) is unch.

Dec T-note prices (ZNZ15 -0.10%) are down -4.5 ticks.

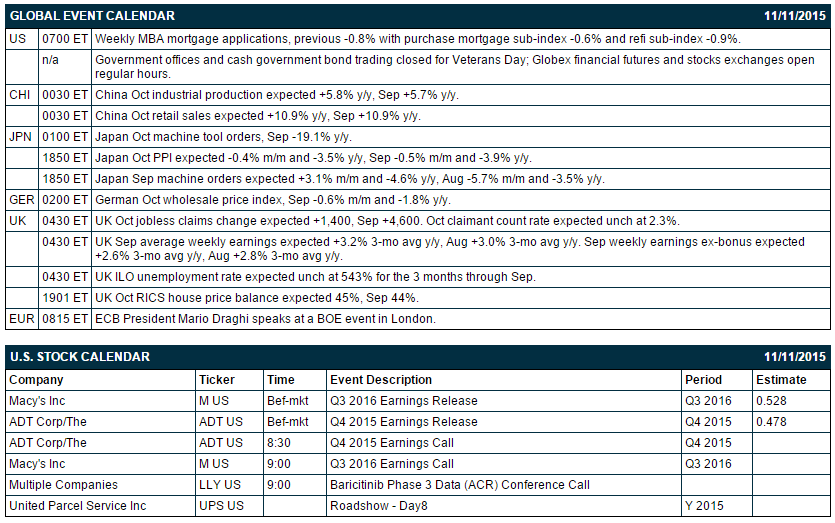

China Oct industrial production rose +5.6% y/y, weaker than expectations of +5.8% y/y and matched the Mar 2015 gain as the slowest pace of increase in nearly 7 years.

China Oct retail sales rose +11.0% y/y, stronger than expectations of +10.9% y/y and the fastest pace of increase since Dec of 2014.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -0.8% with purchase mortgage sub-index -0.6% and refi sub-index-0.9%). Government offices and cash government bond trading are closed today for Veterans Day but Globex financial futures and stocks exchanges are open during regular hours.

There are 2 of the S&P 500 companies that report earnings today: Macy's (consensus $0.53), ADT Corp (0.48).

U.S. IPO's scheduled to price today: Loxo Oncology (LOXO).

Equity conferences today include: Baird Healthcare Conference on Mon-Wed, Edison Electric Institute Financial Conference on Mon-Wed, Robert W. Baird & Co. Industrial Conference on Mon-Wed, Bank of America Merrill Lynch Global Energy Conference on Tue-Wed, Credit Suisse Boston Financials Conference on Tue-Wed, Credit Suisse Health Care Conference on Tue-Wed, Wells Fargo Securities Technology, Media and Telecom Conference on Tue-Wed, RBC Capital Markets Technology, Internet, Media and Telecommunications Conference on Tue-Wed, Stephens Inc Fall Investment Conference on Tue-Wed, Jefferies Energy Conference on Wed, UBS Building & Building Products CEO Conference on Wed.

OVERNIGHT U.S. STOCK MOVERS

Tyco International Plc (TYC -0.14%) was upgraded to 'Overweight' from 'Neutral' at JPMorgan Chase with a price target of $42.

Alarm.com Holdings (ALRM +4.07%) jumped 10% in after-hours trading after it reported Q3 adjusted EPS of 14 cents, well above consensus of 2 cents, and then raised guidance on fiscal 2015 adjusted EPS to 20 cents-21 cents from an August estimate of 13 cents-14 cents, above consensus of 14 cents.

MetLife (MET -0.06%) was downgraded to 'Equal Weight' from 'Overweight' at Morgan Stanley.

Horizon Pharma Plc (HZNP +0.40%) plunged 25% in pre-market trading after Express Scripts Holding said it was suing the company for $140 million for unfilled contractual obligations.

SanDisk (SNDK -1.57%) was downgraded to 'Market Perform' from 'Outperform' at Bernstein.

Sanofi (SAN -0.72%) and Regeneron Pharmaceuticals (REGN +1.14%) announced that 74% of patients in a Phase 3 clinical trial reached their pre-specified LDL cholesterol targets within 8 weeks of adding the new Praluent (alirocumab) injection to their standard-of-care.

WuXi PharmaTech (WX +0.20%) and Eli Lilly (LLY +0.88%) announced that have entered into a strategic collaboration to develop, manufacture and promote a cholesterol drug in China.

Boston Scientific (BSX +1.13%) fell nearly 4% in after-hours trading after CMS said evidence shows that percutaneous left atrial appendage closure (LAAC) therapy using an implanted device is not necessary.

ChannelAdvisor reported that Amazon (AMZN +0.64%) Oct same-store-sales rose +16.4% y/y.

Lockheed Martin (LMT -0.29%) was awarded a 5-year U.S. Air Force contract worth as much as $968.7 million to build 17 C-130J aircrafts.

Public Storage (PSA +1.00%) was rated a new 'Underweight' at BB&T Capital Markets with a 12-month price target of $217.50.

Veritex Holdings (VBTX +1.45%) filed to sell $150 million of mixed securities.

Boot Barn (BOOT +2.49%) dropped over 9% in after-hours trading after it lowered guidance on fiscal 2016 adjusted EPS to 76 cents-80 cents from an August estimate of 85 cents-90 cents, below consensus of 86 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 +0.32%) this morning are up +6.75 points (+0.32%). Tuesday's closes: S&P 500 +0.15%, Dow Jones +0.16%, Nasdaq -0.30%. The S&P on Tuesday recovered from early losses and closed higher on the subdued inflation picture indicated by the -10.5% y/y decline in Oct import prices and on the +0.5% increase in U.S. Sep wholesale trade sales, stronger than expectations of +0.1%. Stocks were hurt early by deflation risks in China after the China Oct CPI report of +1.3% y/y versus expectations of +1.5% y/y.

Dec 10-year T-notes (ZNZ15 -0.10%) this morning are down -4.5 ticks. Tuesday's closes: TYZ5 +8.50, FVZ5 +6.50. Dec T-notes on Tuesday closed higher on the larger-than-expected decline in U.S. Oct import prices and on strong foreign demand for the Treasury's $24 billion 10-year T-note auction after indirect bidders, a proxy for foreign central bank demand, purchased 60.5% of the auction, higher than the 12-auction average of 56.8%.

The dollar index (DXY00 -0.11%) this morning is down -0.097 (-0.10%). EUR/USD (^EURUSD) is down -0.0010 (-0.09%). USD/JPY (^USDJPY) is unch. Tuesday's closes: Dollar Index +0.314 (+0.32%), EUR/USD -0.0028 (-0.26%), USD/JPY -0.03 (-0.02%). The dollar index on Tuesday climbed to a 6-3/4 month high and closed higher on favorable dollar interest rate differentials after the recent rise in T-note yields and on weakness in EUR/USD which tumbled to a 6-1/2 month low on speculation the ECB will expand QE after ECB Board member and Bank of Finland Governor Liikanen said that "decelerating growth in the emerging economies threatens to dampen global activity."

Dec crude oil (CLZ15 -1.31%) this morning is down -52 cents (-1.18%) at a 2-week low and Dec gasoline (RBZ15 +0.10%) is up +0.0055 (+0.40%). Tuesday's closes: CLZ5 -0.24 (-0.55%), RBZ5 -0.0136 (-0.99%). Dec crude oil and gasoline prices on Tuesday closed lower with Dec crude at a 1-1/2 week low and Dec gasoline at a 1-week low. Crude oil prices were undercut by the rally in the dollar index to a 6-3/4 month high and by concern that China's economic slowdown is deepening after China Oct PPI fell by the most in 6 years.

Disclosure:None.