Morning Call For March 31, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 -0.53%) this morning are down -0.52% and European stocks are down -0.37% on giveback from Monday's sharp gains. Energy producers are lower as crude oil slides on speculation a nuclear deal may be reached with Iran, while European deflation concerns remain after Eurozone Mar core CPI rose at the slowest pace on record. On the positive side, the Eurozone Feb unemployment rate fell to a 2-3/4 year low and German Mar retail sales were stronger than expected. Asian stocks settled mixed: Japan -1.05%, Hong Kong +0.18%, China -0.90%, Taiwan +0.68%, Australia +0.78%, Singapore -0.21%, South Korea +0.46%, India -0.07%. Commodity prices are weaker. May crude oil (CLK15 -2.18%) is down -2.26% on speculation that Western nations are nearing a nuclear deal with Iran that could allow sanctions to be lifted and allow Iran to increase crude exports that would exacerbate a global supply glut. May gasoline (RBK15 -1.82%) is down -1.63% at a 1-week low. Apr gold (GCJ15 -0.10%) is down -0.10% at a 1-week low. May copper (HGK15 -1.28%) is down -1.49% at a 1-week low. Agriculture prices are mostly lower ahead of the USDA Quarterly Grain stocks and U.S. 2015 acreage estimates. The dollar index (DXY00 +0.44%) is up +0.51% at a 1-week high. EUR/USD (^EURUSD) is down -0.81% at a 1-week low. USD/JPY (^USDJPY) is down -0.17%. Jun T-note prices (ZNM15 +0.12%) are up +5 ticks.

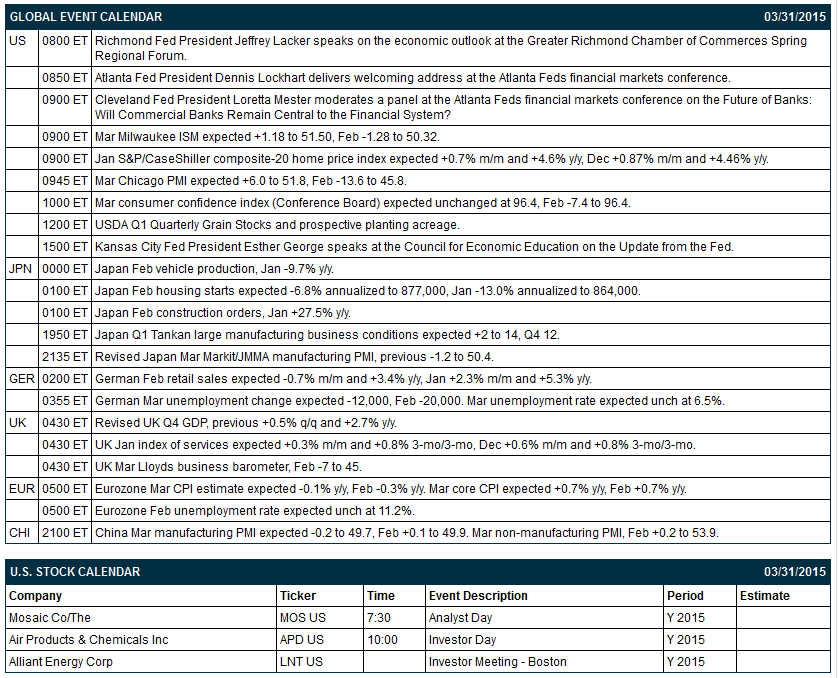

The Eurozone Mar CPI estimate fell -0.1% y/y, right on expectations. The Mar core CPI rose +0.6% y/y, less than expectations of +0.7% y/y and matched January's gain as the slowest pace of increase since the data series began in 1997.

The Eurozone Feb unemployment rate fell -0.1 to 11.3% from an upward revised 11.4% in Jan, the lowest in 2-3/4 years.

The German Mar unemployment change fell -15,000 to 2.8 million, better than expectations of -12,000. The Mar unemployment rate unexpectedly fell -0.1 to 6.4%, better than expectations of no change at 6.5% and the lowest since data for a unified Germany began in 1991.

German Feb retail sales fell -0.5% m/m and rose +3.6% y/y, stronger than expectations of -0.7% m/m and +3.4% y/y.

UK Mar GfK consumer confidence rose +3 to 4, stronger than expectations of +1 to 2 and the highest in 12-3/4 years.

UK Mar Lloyds business barometer rose +8 to 53, the highest in 6 months.

UK Q4 GDP was revised upward to +0.6% q/q and +3.0% y/y from the originally reported +0.5% q/q and +2.7% y/y.

Japan Feb housing starts fell -3.1% annualized to 905,000, a smaller decline than expectations of -6.8% annualized to 877,000.

Japan Feb vehicle production fell -5.3% y/y, a smaller decline than the -9.7% y/y drop in Jan but still the eighth consecutive month production has declined.

U.S. STOCK PREVIEW

Key news today includes (1) today's deadline for a political agreement on the Iran nuclear talks, (2) today's Mar Milwaukee ISM index (expected +1.18 to 51.50 after Feb's -1.28 to 50.32), (3) today's Jan S&P/CaseShiller Composite-20 home price index (expected +0.7% m/m and +4.6% y/y after Dec's +0.87% m/m and +4.46% y/y), (4) today's Mar Chicago PMI (expected +6.0 to 51.8 after Feb's -13.6 to 45.8), (5) today's Mar U.S. consumer confidence index from the Conference Board (expected unchanged at 96.4 after Feb's -7.4 to 96.4), and (6) comments by four different Fed officials.

None of the Russell 1000 companies report earnings today.

U.S. IPO's that price today include: GoDaddy (GDDY), Infraredx (REDX), Wowo (WOWO), AutoGenomics (AGMX), Mylan (MYL), Media General (MEG), CyrusOne (CONE), Insmed (INSM). There are U.S. IPO's that start trading today.

Equity conferences during the remainder of this week include: Bank of America Merrill Lynch New York Auto Summit on Wed, DUG Bakken and Niobrara Unconventional Oil Conference on Wed, Mitsubishi UFJ Financial Utilities Conference on Wed, New York Interational Auto Show-Press Days on Wed, and Goldman Sachs Biosimilars Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Schlumberger (SLB +1.40%) was downgraded to 'Market Perform' from 'Outperform' at Wells Fargo.

Credit Suisse reiterates its 'Outperform' rating on UnitedHealth (UNH +2.53%) and raised its price target on the stock to $135 from $120.

Reliance Steel (RS +2.83%) was upgraded to 'Outperform' from 'Neutral' at Credit Suisse.

D.R. Horton (DHI +2.11%) was upgraded to 'Positive' from 'Neutral' at Susquehanna.

SAIC (SAIC +2.47%) reported Q4 EPS of 75 cents, better than consensus of 71 cents.

Priceline (PCLN +1.29%) was upgraded to 'Buy' from 'Hold' at Stifel.

Horizon Pharma (HZNP +18.20%) was upgraded to 'Overweight' from 'Neutral' at Piper Jaffray.

Sensient (SXT +1.37%) was initiated with a 'Buy' at BB&T with a price target of $81.

Tesla (TSLA +3.01%) rose over 1% in after-hours trading after Bloomberg reported that March China sales were up 130%-150% month-over-month.

Gabelli reported a 5.56% stake in Jason Industries (JASN +0.29%) .

Teck Resources (TCK +10.17%) slid nearly 5% in after-hours trading after it said it is not in talks with Antofagasta regarding a possible merger.

HCP (HCP +3.94%) was upgraded to 'Buy' from 'Neutral' at UBS.

MARKET COMMENTS

Jun E-mini S&Ps (ESM15 -0.53%) this morning are down -10.75 points (-0.52%). Monday's closes: S&P 500 +1.22%, Dow Jones +1.49%, Nasdaq +1.15%. The S&P 500 index on Monday rallied sharply on support from a rally in Chinese stocks and hopes for another Chinese interest rate cut or other stimulus measures after China's central bank chief call for more measures to spur growth. Stocks also received a boost from the stronger-than-expected U.S. Feb pending home sales report (+3.1% m/m and +12.0% y/y) and M&A activity with acquisitions announced by UnitedHealth and Teva Pharma.

Jun 10-year T-notes (ZNM15 +0.12%) this morning are up +5 ticks. Monday's closes: TYM5 -3.00, FVM5 -0.75. T-note prices on Monday closed mildly lower due to the stronger-than-expected Feb core PCE deflator report of +1.4% y/y and the U.S. pending home sales report of +3.1% m/m. T-notes were also undercut by reduced safe-haven demand caused by the rally in stocks.

The dollar index (DXY00 +0.44%) this morning is up +0.496 (+0.51%) at a 1-wwek high. EUR/USD (^EURUSD) is down -0.0088 (-0.81%) at a 1-week low. USD/JPY (^USDJPY) is down -0.20 (-0.17%). Monday's closes: Dollar index +0.684 (+0.70%), EUR/USD -0.00547 (-0.50%), USD/JPY +0.966 (+0.81%). The dollar index rallied fairly sharply on Monday due to the stronger-than-expected U.S. pending home sales report, which indicates some signs of life in the housing market that could accelerate a Fed interest rate cut.

May WTI crude oil (CLK15 -2.18%) this morning is down -$1.10 a barrel (-2.26%) and May gasoline (RBK15 -1.82%) is down -0.0293 (-1.63%) at a 1-week low. Monday's closes: CLK5 -0.19 (-0.39), RBK5 -0.0025 (-0.14%). Crude oil and gasoline prices on Monday closed mildly lower due to the rally in the dollar and the remote chance that a last-minute agreement might be reached on Iran's nuclear program. Crude oil received some underlying support from the rally in global stocks and on hopes for additional Chinese stimulus.

Click on picture to enlarge

Disclosure: None.