Morning Call For March 30, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.51%) this morning are up +0.46% and European stocks are up +1.20% on the prospects for China to expand its stimulus measures after China's central bank said the government can do more to support growth. Another positive for European stocks was the larger-than-expected increase in Eurozone Mar economic confidence to the highest in 3-1/2 years. Asian stocks closed mostly higher: Japan +0.65%, Hong Kong +1.51%, China +2.93%, Taiwan +0.19%, Australia -1.25%, Singapore +0.12%, South Korea +0.22%, India +1.88%. China's Shanghai Index surged nearly 3% to a 7-year high after the head of the PBOC, Zhou Xiaochuan, said that China's growth rate has tumbled "a bit" too much, and that policy makers have room to act with both interest rates and "quantitative" measures, which bolstered speculation that China will boost stimulus measures. Commodity prices are mostly lower. May crude oil (CLK15 -1.35%) is down -2.07% on speculation a potential nuclear deal between Iran and Western nations may end sanctions against Iran and lead to increased Iranian crude exports that may exacerbate a global supply glut. May gasoline (RBK15 -0.84%) is down -1.24%. Apr gold (GCJ15 -1.38%) is down -1.20%. May copper (HGK15 +0.31%) is up +0.33%. Agriculture prices are mixed. The dollar index (DXY00 +0.56%) is up +0.53%. EUR/USD (^EURUSD) is down -0.47%. USD/JPY (^USDJPY) is up +0.51%. Jun T-note prices (ZNM15 -0.07%) are down -2.5 ticks.

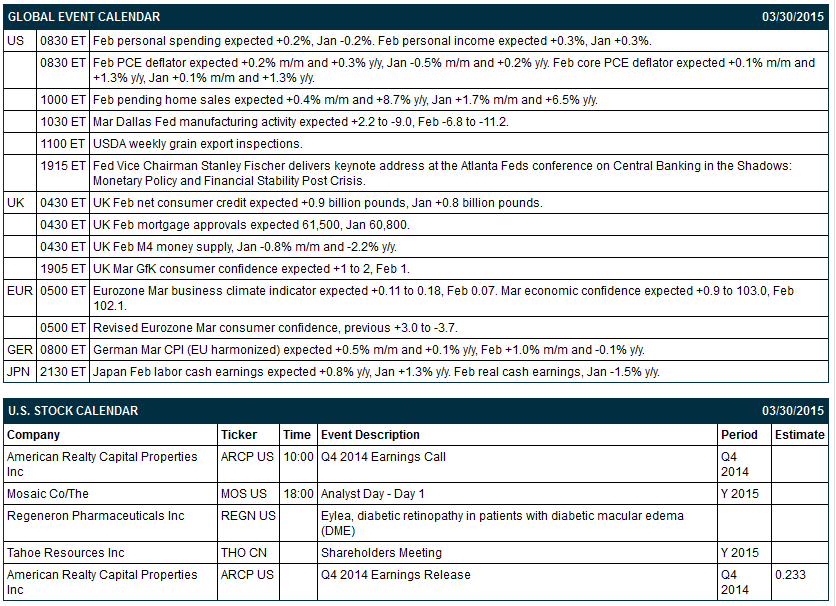

The Eurozone Mar business climate indicator rose +0.14 to 0.23, stronger than expectations of +0.11 to 0.18 and matched the November 2014 reading as the highest in 9 months. Mar economic confidence rose +1.6 to 103.9, stronger than expectations of +0.9 to 103.0 and the highest in 3-1/2 years.

UK Feb mortgage approvals rose 61,800, stronger than expectations of 61,500 and the most in 6 months.

UK Feb net consumer credit rose +0.7 billion pounds, less than expectations of +0.9 billion pounds.

Japan Feb industrial production fell -3.4% m/m and -2.6% y/y, weaker than expectations of -1.9% m/m and -0.6% y/y.

U.S. STOCK PREVIEW

Key news today includes (1) today's deadline for Greece to submit a list of sufficent reforms to Eurozone finance ministers to qualify for frozen bailout money and avoid a new default, (2) oil prices ahead of tomorrow's deadline for a political agreement on the Iran nuclear talks, (3) today's Feb personal income report (expected +0.3%) and spending report (expected +0.2%), (4) today's Feb PCE deflator report (expected +0.3% y/y vs +0.2% in Jan) and Feb core PCE deflator report (expected unchanged from Jan at +1.3%), (4) today's Feb pending home sales report (expected +0.4% m/m), (5) today's Mar Dallas Fed manufacturing activity index (expected +2.2 to -9.0), and (6) Fed Vice Chairman Stanley Fischer's keynote address at the Atlanta Fed’s conference on “Central Banking in the Shadows: Monetary Policy and Financial Stability Post Crisis.”

There is one of the Russell 1000 companies that reports earnings today: American Realty Capital Properties (consensus $0.23).

There are no U.S. IPOs that are scheduled to price or begin trading today.

Equity conferences this week include: Bank of America Merrill Lynch New York Auto Summit on Wed, DUG Bakken and Niobrara Unconventional Oil Conference on Wed, Mitsubishi UFJ Financial Utilities Conference on Wed, New York Interational Auto Show-Press Days on Wed, and Goldman Sachs Biosimilars Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Nike (NKE +0.55%) was upgraded to 'Outperform' from 'Neutral' at RW Baird.

Genesco (GCO +0.49%) was downgraded to 'Neutral' from 'Outperform' at RW Baird

BHP Billiton (BHP -1.98%) was upgraded to 'Outperformer' from 'Sector Performer' at CIBC.

Western Union (WU +1.60%) was upgraded to 'Buy' from 'Hold' at Evercore ISI.

Xilinx (XLNX +5.85%) was downgraded to 'Equal Weight' from 'Overweight' at Morgan Stanley.

Madison Square Garden (MSG +1.55%) was upgraded to 'Buy' from 'Hold' at Topeka.

Horizon Pharma (HZNP +3.27%) will acquire Hyperion Therapeutics (HPTX -1.88%) for $46.00 per share, or $1.1 billion on a fully diluted basis.

Restoration Hardware (RH +4.06%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs.

Barclays upgraded Analog Devices (ADI +2.47%) to 'Overweight' from 'Equal Weight' saying it believes the chip maker has secured multiple socket wins in Apple's iPhone and iPad.

Altera (ALTR +28.37%) is up over 3% in pre-market trading on carry-over support from Friday's 28% surge in the stock amid reports that Intel is in negotiations to acquire the company.

Realty Income (O -0.37%) will replace Windstream (WIN -5.10%) in the S&P 500 as the close of trading on April 6.

Fitch Ratings downgraded Greece's Long-term foreign and local currency Issuer Default Ratings to 'CCC' from 'B.'

Enterprise Partners reported a 8.3% passive stake in Celladon (CLDN +2.88%) .

MARKET COMMENTS

Jun E-mini S&Ps (ESM15 +0.51%) this morning are up +9.50 points (+0.46%). Friday's closes: S&P 500 +0.24%, Dow Jones +0.19%, Nasdaq +0.41%. The U.S. stock market closed higher on Friday on the stronger-than-expected +1.8 point increase to 93.0 in the final-March U.S. consumer confidence index from the University of Michigan and the rally in tech stocks sparked by the news that Intel is in talks to acquire Altera. Stock market gains were limited by disappointment that U.S. Q4 GDP was left unrevised at +2.2% versus expectations for an upward revision to +2.4%.

Jun 10-year T-notes (ZNM15 -0.07%) this morning are down -2.5 ticks. Friday's closes: TYM5 +14.50, FVM5 +9.00. T-note prices rallied on Friday due to reduced inflation expectations sparked by the plunge in crude oil prices and the unrevised Q4 GDP report of +2.2% that suggests the Fed will to slow to raise interest rates.

The dollar index (DXY00 +0.56%) this morning is up +0.520 (+0.53%). EUR/USD (^EURUSD) is down -0.0051 (-0.47%). USD/JPY (^USDJPY) is up +0.61 (+0.51%). Friday's closes: Dollar index -0.145 (-0.15%), EUR/USD +0.005 (+0.05%), USD/JPY -0.06 (-0.05%). The dollar index on Friday closed mildly lower after the unrevised U.S. Q4 GDP report of +2.2% sparked ideas that the Fed may delay an interest rate hike. The dollar received some underlying support from the stronger-than-expected U.S. Mar University of Michigan consumer sentiment report.

May WTI crude oil (CLK15 -1.35%) this morning is down -$1.01 a barrel (-2.07%) and May gasoline (RBK15 -0.84%) is down -0.0222 (-1.24%). Friday's closes: CLK5 -2.56 (-4.98), RBK5 -0.0877 (-4.66%). May crude oil and gasoline prices on Friday fell sharply on the possibility for an Iranian nuclear agreement and on ideas that Saudi Arabia's military involvement in Yemen may actually reduce the chances of oil disruptions in the Middle East.

Click on picture to enlarge

Disclosure: None.