Morning Call For March 3, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.14%) this morning are down -0.09% and European stocks are down -0.19% led by a decline in bank stocks after Barclays fell over 3% when it said it set aside 750 million pounds ($1.2 billion) for the settlement of a currency-manipulation probe. Also, data from the Basel Committee on Banking Supervision said global banks are 305 billion euros ($341 billion) short of their liquidity coverage ratio (LCR). The Basel rule began to phase in Jan 1, when banks were required to have at least 60% of their liquidity buffers. The LCR takes full effect in 2019 when the LCR rises to 100%. The LCR was designed to require global banks have sufficient high-quality liquid assets to withstand a stressed 30-day funding scenario. Losses in European stocks are limited after German Jan retail sales posted the largest monthly increase in 7 years. Asian stocks closed mixed: Japan-0.06%, Hong Kong -0.74%, China -2.59%, Taiwan +0.05%, Australia -0.42%, Singapore +0.54%, South Korea +0.34%, India +0.46%. Chinese growth concerns undercut Asian stocks after the government-controlled Xinhua News Agency reported that Chinese Premier Li Keqiang will announce Thursday at the annual National People's Congress a Chinese growth target of 7% for 2015, down from 7.5% in 2014. Commodity prices are mixed. Apr crude oil (CLJ15 +1.57%) is up +1.45% and Apr gasoline (RBJ15 +2.64%) is up +1.96%. Apr gold (GCJ15 +0.14%) is down -0.02%. May copper (HGK15 -1.48%) is down -1.58%. Agriculture prices are higher. The dollar index (DXY00 +0.08%) is up +0.05% at a new 11-1/3 year high. EUR/USD (^EURUSD) is down -0.21%. USD/JPY (^USDJPY) is down -0.22%. Jun T-note prices (ZNM15 -0.09%) are down -6 ticks at a 1-week low.

Eurozone Jan PPI fell -0.9% m/m and -3.4% y/y, weaker than expectations of -0.7% m/m and -3.0% y/y, with the -3.4% y/y drop the biggest year-over-year decline in 5 years.

German Jan retail sales rose +2.9% m/m, stronger than expectations of +0.4% m/m and the largest monthly increase in 7 years. On an annual basis, Jan retail sales rose +5.3% y/y, stronger than expectations of +3.0% y/y.

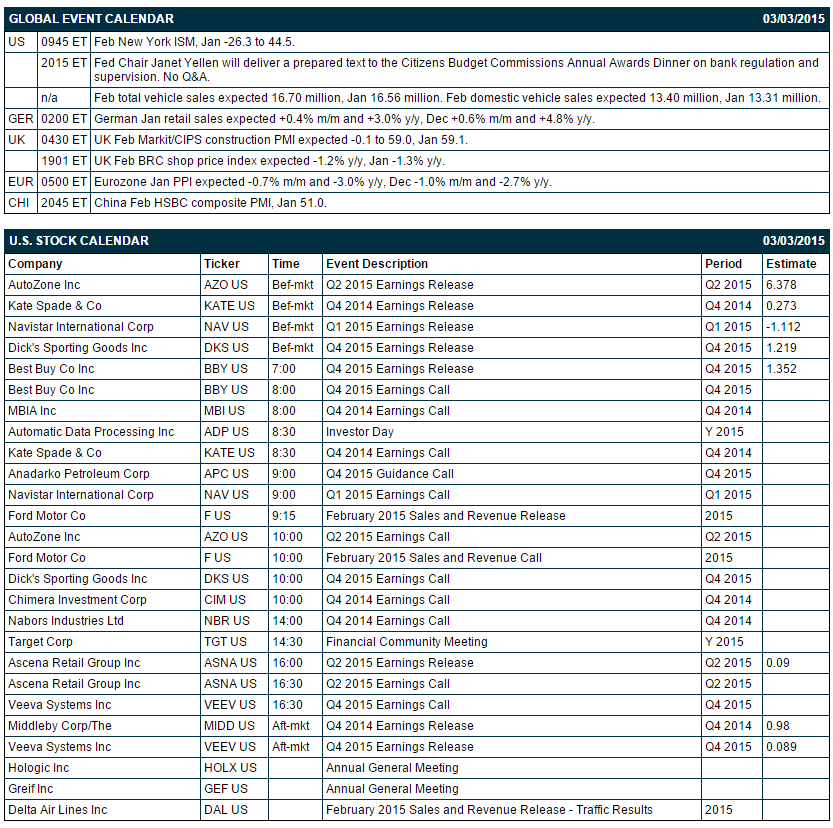

UK Jan Markit/CIPS construction PMI unexpectedly rose +1.0 point to 60.1, stronger than expectations of -0.1 to 59.0 and the fastest pace of expansion in 4 months.

Japan Jan labor cash earnings rose +1.3% y/y, stronger than expectations of +0.5% y/y. Jan real cash earnings fell -1.5% y/y, the nineteenth consecutive month real cash earnings have declined.

U.S. STOCK PREVIEW

Today’s Feb total vehicle sales report is expected to edge higher to 16.70 million units from 16.56 million units in January. There are 2 of the S&P 500 companies that report earnings today: Best Buy (consensus $1.35), AutoZone (6.38).

Equity conferences during the remainder of this week include: Cowen & Co. Health Care Conference on Mon-Wed, 10th LNG Supplies for Asian Markets on Mon-Tue, Association of Insurance and Financial Analysts Conference on Mon-Tue, Citigroup Global Property CEO Conference on Mon-Wed, Raymond James & Associates Institutional Investors Conference on Mon-Wed, Morgan Stanley Technology Media & Telecom Conference on Mon-Thu, JMP Securities Technology Conference on Tue, SpeedNews 5th Annual Aerospace Raw Materials & Manufacturers Supply Chain Conference on Tue, ISI Industrial Conference on Tue, Bank of America Merrill Lynch Consumer & Retail Conference on Tue-Wed, J.P. Morgan Aviation, Transportation and Industrials Conference on Tue-Thu, Mitsubishi UFJ Securities 3rd Annual Seattle Consumer Conference on Wed, Morgan Stanley European MedTech & Services Conference on Wed, Simmons Energy Conference on Wed, UBS Natural Gas, Electric Power and MLP Conference on Wed, UBS Utilities and Natural Gas Conference on Wed, UBS Global Consumer Conference on Wed-Thu, Bank of America Merrill Lynch Refining Conference on Thu, Barclays Investment Grade Energy & Pipeline Conference on Thu, Pacific Crest Emerging Technology Summit on Thu, Morgan Stanley MLP/Diversified Natural Gas, Utilities Clean Tech Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Nomura downgraded Micron (MU +1.86%) to 'Neutral' from 'Buy.'

Navistar (NAV -0.58%) reported a Q1 EPS loss of -52 cents, a smaller loss than consensus of -$1.09.

Lumber Liquidators (LL -25.13%) was upgraded to 'Buy' from 'Neutral' at Janney Capital.

Dick's Sporting (DKS +2.46%) reported Q4 EPS of $1.30, above consensus of $1.22.

Best Buy (BBY +1.39%) reported Q4 EPS of $1.48, higher than consensus of $1.35.

AutoZone ({=AZO reported Q2 EPS of $6.51, better than consensus of $6.38.

Nortek (NTK +2.27%) reported Q4 EPS of 29 cents, well above consensus of 19 cents.

CBOE Holdings (CBOE -0.92%) reported that total options and futures volume at CBOE Holdings during February was 88.5 million contracts, down-17% m/m and -22% y/y.

Nabors Industries (NBR -2.11%) reported Q4 adjusted EPS of 33 cents, below consensus of 39 cents.

McDermott (MDR +4.40%) surged 20% in after-hours trading after it reported Q4 EPS of 3 cents, much better than consensus of a -6 cent loss, and then raised guidance on fiscal 2015 revenue to $3.3 billion-$3.6 billion, stronger than consensus of $2.79 billion.

Mylan (MYL +0.98%) reported Q4 adjusted EPS of $1.05, right on consensus, although Q4 revenue of $2.08 billion was better than consensus of $2.07 billion.

Herman Miller (MLHR +0.74%) lowered guidance on 2015 revenue to $2.118 billion-$2.153 billion, below consensus of $2.170 billion.

Caesar's (CZR +3.96%) slid over 4% in after-hours trading after it reported a Q4 EPS loss of -$7.00, more than four times consensus of a -$1.65 loss.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.14%) this morning are down -2.00 points (-0.09%). The S&P 500 index on Monday closed higher: S&P 500 +0.61%, Dow Jones +0.86%, Nasdaq +0.95%. Bullish factors included (1) China’s second interest rate cut in 3 months, and (2) increased M&A activity after NXP Semiconductors NV agreed to buy Freescale Semiconductor Ltd. for about $11.8 billion and after Cardinal Health agreed to buy Johnson & Johnson’s Cordis business for $1.94 billion. Stocks ignored bearish factors that included (1) weaker-than-expected U.S. Jan personal spending and personal income, and (2) the -0.6 point decline in the U.S. Feb ISM manufacturing index to 52.9, weaker than expectations of -0.5 to 53.0 and the slowest pace of expansion in 13 months.

Jun 10-year T-notes (ZNM15 -0.09%) this morning are down -6 ticks at a 1-week low. Jun 10-year T-note futures prices on Monday closed lower. Closes: TYM5 -21.50, FVM5 -11.75. Bearish factors included (1) U.S. economic data on Feb ISM manufacturing and Jan personal spending that was close to expectations and fueled speculation that Fed will start to raise interest rates this year, and (2) reduced safe-haven demand after stocks rallied.

The dollar index (DXY00 +0.08%) this morning is up +0.049 (+0.05%) at a new 11-1/3 year high. EUR/USD (^EURUSD) is down -0.0024 (-0.21%). USD/JPY (^USDJPY) is down -0.26 (-0.22%). The dollar index on Monday climbed to a 5-week high and closed higher: Dollar index +0.169 (+0.18%), EUR/USD -0.00088 (-0.08%), USD/JPY +0.52 (+0.43%). Bullish factors included (1) The U.S. ISM manufacturing report that was close to expectations, which boosted speculation the Fed is closer to raising interest rates, and (2) weakness in the Chinese yuan which fell to a 2-year low against the dollar after China cut interest rates for the second time in 3 months.

Apr WTI crude oil (CLJ15 +1.57%) this morning is up +72 cents (+1.45%) and Apr gasoline (RBJ15 +2.64%) is up +0.0371 (+1.96%). Apr crude and Apr gasoline prices on Monday closed lower: CLJ5 -0.17 (-0.34%), RBJ5 -0.0629 (-3.18%). Bearish factors included (1) a rally in the dollar index to a 5-week high, and (2) increased crude output in Saudi Arabia, the largest OPEC producer, as Saudi Arabian Feb crude production rose +130,000 bpd to 9.85 million bpd, the highest in 17 months. Losses in crude were limited after an oil industry survey from Genscape Inc. said Wednesday’s EIA data will show a negligible increase of crude inventories at Cushing, OK, the delivery point for WTI futures, for the week ended Feb 27.

Disclosure: None.