Morning Call For March 24, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.23%) this morning are up +0.19% and European stocks are up +0.31% after Eurozone manufacturing activity this month expanded at the fastest pace in 10 months. Upbeat comments from St. Louis Fed President Bullard also gave stocks a lift when he said he expects the U.S. economy to grow at a 3.0% rate this year and that falling unemployment will herald a "boom time." Asian stocks closed mixed: Japan -0.21%, Hong Kong -0.39%, China +0.02%, Taiwan -0.27%, Australia +0.22%, Singapore +0.09%, South Korea +0.08%, India -0.11%. China's Shanghai Stock Index eked out a gain for the tenth consecutive session and climbed to the highest in 6-3/4 years after weaker-than-expected manufacturing data bolstered speculation that the government will expand stimulus. The China Mar HSBC flash manufacturing PMI fell -1.5 to 49.2 and contracted at the fastest pace in 11 months. Commodity prices are mostly higher. May crude oil (CLK15 +0.63%) is up +0.82% and May gasoline (RBK15 +0.54%) is up +0.93%, both at 1-week highs. Apr gold (GCJ15 +0.46%) is up +0.52%. May copper (HGK15 +0.14%) is up +0.29%. Agriculture prices are mixed. The dollar index (DXY00 -0.25%) is down -0.36%. EUR/USD (^EURUSD) is up +0.36%. USD/JPY (^USDJPY) is down -0.29%. Jun T-note prices (ZNM15 +0.07%) are up +3.5 ticks.

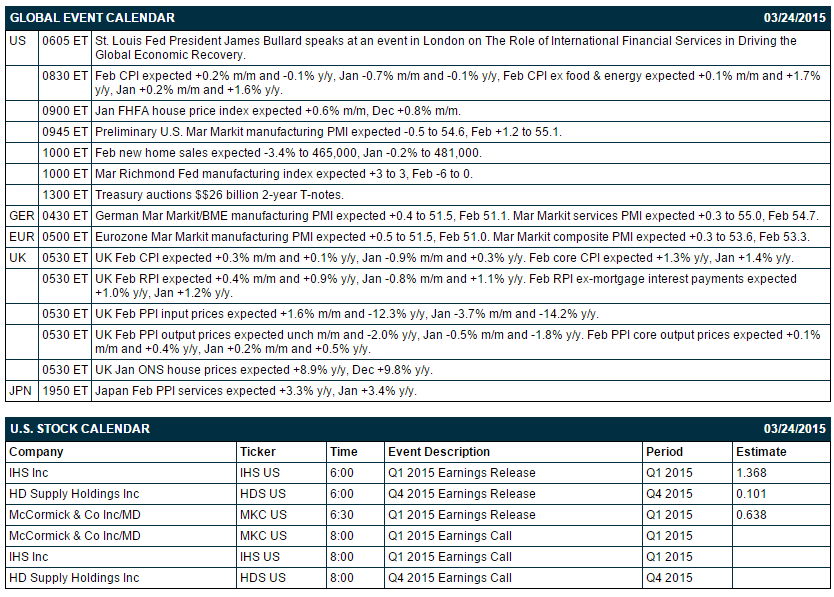

The Eurozone Mar Markit manufacturing PMI rose +0.9 to 51.9, stronger than expectations of +0.5 to 51.5 and the fastest pace of expansion in 10 months. The Mar Markit composite PMI rose +0.8 to 54.1, stronger than expectations of +0.3 to 53.6 and the highest since the data series began in 2012.

The German Mar Markit/BME manufacturing PMI rose +1.3 to 52.4, stronger than expectations of +0.4 to 51.5 and the fastest pace of expansion in 8 months. The Mar Markit services PMI rose +0.6 to 55.3, stronger than expectations of +0.3 to 55.0 and the fastest pace of expansion in 6 months.

UK Feb CPI rose +0.3% m/m, right on expectations, nut was unch, y/y, weaker than expectations of +0.1% y/y and the slowest pace since the data series began in 1989. Feb core CPI rose +1.2% y/y, weaker than expectations of +1.3% y/y and matched November as the slowest pace of increase in 6 years.

St. Louis Fed President Bullard said the U.S. economy will grow at a 3.0% rate through 2015 and falling employment will herald a "boom time" for the U.S. He said developing economic conditions will set up the Fed to start normalizing policy in 2015 and that Fed policy will still be very accommodative after a "small rise."

The China Mar HSBC flash manufacturing PMI fell -1.5 to 49.2, weaker than expectations of -0.2 to 50.5 and the fastest pace of contraction in 11 months.

The Japan Mar Markit/JMMA manufacturing PMI unexpectedly fell -1.2 to 50.4, weaker than expectations of +0.4 to 52.0 and the slowest pace of expansion in 10 months.

U.S. STOCK PREVIEW

Today’s Feb headline CPI report is expected to be unchanged from Jan on a year-on-year basis at -0.1% y/y. Meanwhile, today’s Feb core CPI is expected to rise slightly to +1.7% y/y from +1.6% in Jan. Today’s Feb new home sales report is expected to show a -3.4% decline to 465,000, adding to January’s small decline of -0.2% to 481,000. Today’s Jan FHFA house price index is expected to show a solid increase of +0.6% m/m, adding to December’s sharp increase of +0.8% m/m. The Treasury today will sell $26 billion of 2-year T-notes. There are three of the Russell 1000 companies that reports earnings today: IHS (consensus $1.37), McCormick (0.64), HD Supply (0.10).

Equity conferences during the remainder of this week include: Barclays Emerging Payments Forum on Mon-Tue, Goldman Sachs Houston Chemical Intensity Days on Mon-Tue, Howard Weil Energy Conference on Mon-Tue, BioPharma Asia Convention 2015 on Mon-Wed, Canaccord Genuity Musculoskeletal Conference on Tue, Barclays Select Series Metals & Materials Cross Asset Forum on Tue, Excellence in Data Analytics for Shared Services and Outsourcing 2015 on Tue-Wed, Telsey Advisory Group (TAG) Spring Consumer Conference on Tue-Wed, Leerink Booth Tours At American Academy of Orthopaedic Surgeons on Wed-Thu, CIBC Real Estate Conference on Thu, Nomura - Conference: Global Chemicals Industry Leaders Conference - London on Thu, Jefferies Animal Health Summit on Thu, Gabelli Specialty Chemicals Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

RW Baird upgraded Cummins (CMI -0.01%) to 'Outperform' from 'Neutral' and raised its price target to $166 from $155.

L Brands (LB +0.02%) was initiated with a 'Buy' at Topeka with a price target of $106.

Estee Lauder (EL -0.78%) was upgraded to 'Outperform' from 'Market Perform' at Wells Fargo.

Hartford Financial (HIG -0.26%) coverage resumed with a 'Buy' at Goldman Sachs with a price target of $49.

McCormick & Co. (MKC +0.44%) reported Q1 EPS of 70 cents, higher than consensus of 64 cents.

IHS Inc. (IHS -0.16%) reported Q1 adjusted EPS of $1.36, right on consensus, but then lowered guidance on fiscal 2015 adjusted EPS to $5.77-$5.97 from $6.10-$6.30, below consensus of $6.18.

HD Supply (HDS -0.98%) reported Q4 EPS of 11 cents, better than consensus of 10 cents.

Fluor (FLR +1.03%) was awarded an engineering contract for a new Chinese polysilicon plant in Yulin, Shaanxi Province, China, that will have an anticipated total investment of more than $1 billion.

Starboard reported a 13.1% stake in Insperity (NSP -3.55%) .

Carl Icahn reported a 10.98% stake in Chesapeake (CHK +3.67%) .

The U.S. FDA approved Abiomed's (ABMD +2.38%) Impella 2.5 System, a miniature blood pump system intended to help certain patients maintain stable heart function and circulation during certain high-risk percutaneous coronary intervention procedures.

American Water (AWK -0.76%) coverage was resumed with a 'Buy' at Janney Capital with a price target of $62.

MARKET COMMENTS

Jun E-mini S&Ps (ESM15 +0.23%) this morning are up +4.00 points (+0.19%). Monday's Closes: S&P 500 -0.17%, Dow Jones -0.06%, Nasdaq-0.292%. The stock market moved lower on Monday on the weaker than expected U.S. Feb existing home sales report (+1.2% to 4.88 million) and Feb Chicago Fed national activity index (-0.01 to a 6-month low of -0.01). In addition, Fed Vice Chairman Fisher said that raising interest rates “likely will be warranted before the end of the year.”

Jun 10-year T-notes (ZNM15 +0.07%) this morning are up +3.5 ticks. Monday's Closes: TYM5 +5.00, FVM5 +3.50. T-note prices move higher on Monday due to the weaker-than-expected U.S. economic data and safe-haven demand with the sell-off in stocks.

The dollar index (DXY00 -0.25%) this morning is down -0.347 (-0.36%). EUR/USD (^EURUSD) is up +0.0039 (+0.36%). USD/JPY (^USDJPY) is down-0.35 (-0.29%). Monday's closes: Dollar index -0.876 (-0.89%), EUR/USD +0.01276 (+1.18%), USD/JPY -0.302 (-0.25%). The dollar was undercut on Monday by the weaker-than-expected U.S. Feb existing home sales report and Feb Chicago Fed national activity index. Meanwhile, EUR/USD received a boost as the Eurozone Mar consumer confidence rose to a 7-1/2 year high.

May WTI crude oil (CLK15 +0.63%) this morning is up +39 cents (+0.82%) at a 1-week high and May gasoline (RBK15 +0.54%)is up +0.0168 (+0.93%), also at a 1-week high. Monday's closes: CLK5 +0.88 (+1.89), RBK5 +0.0063 (+0.35%). Energy prices received a boost on Monday from the weaker dollar and the early rally in the S&P 500 index to a 2-1/2 week high. Oil prices overcame early losses tied to Saudi Arabian Oil Minister Ali al-Naimi’s comment that Saudi Arabia will not repeat the mistakes of the 1980s when it cut production as oil prices fell.

Disclosure: None.