Morning Call For March 15, 2016

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM16 -0.56%) are down -0.50% and European stocks are down -0.71% as a slide in commodity prices drags down raw material and energy producing stocks. Freeport-McMoRan is down over 5% in pre-market trading as the price of gold drops to a 1-1/2 week low and Schlumberger Ltd. SLB is down over 1% in pre-market trading as the price of crude oil dropped to a 1-week low. Also, long liquidation in stocks is pulling prices lower ahead of the 2-day FOMC meeting that begins today. Asian stocks settled mostly lower: Japan -0.68%, Hong Kong -0.72%, China +0.17%, Taiwan-1.56%, Australia -1.43%, Singapore -0.27%, South Korea -0.13%, India -1.02%. Japanese stocks retreated, led by a fall in exporters, as the yen strengthened against the dollar after the BOJ maintained a negative interest rate and kept asset-purchase plans unchanged following its policy meeting today.

The dollar index (DXY00 +0.11%) is up +0.19%. EUR/USD (^EURUSD) is down -0.13%. USD/JPY (^USDJPY) is down -0.62%.

Jun T-note prices (ZNM16 +0.16%) are up +6 ticks.

As expected, the BOJ refrained from additional stimulus following the conclusion of today's policy meeting and said it "will examine risks to economic activity and prices, and take additional easing measures in terms of three dimensions -- quantity, quality, and the interest rate - if it is judged necessary for achieving the price stability target."

U.S. STOCK PREVIEW

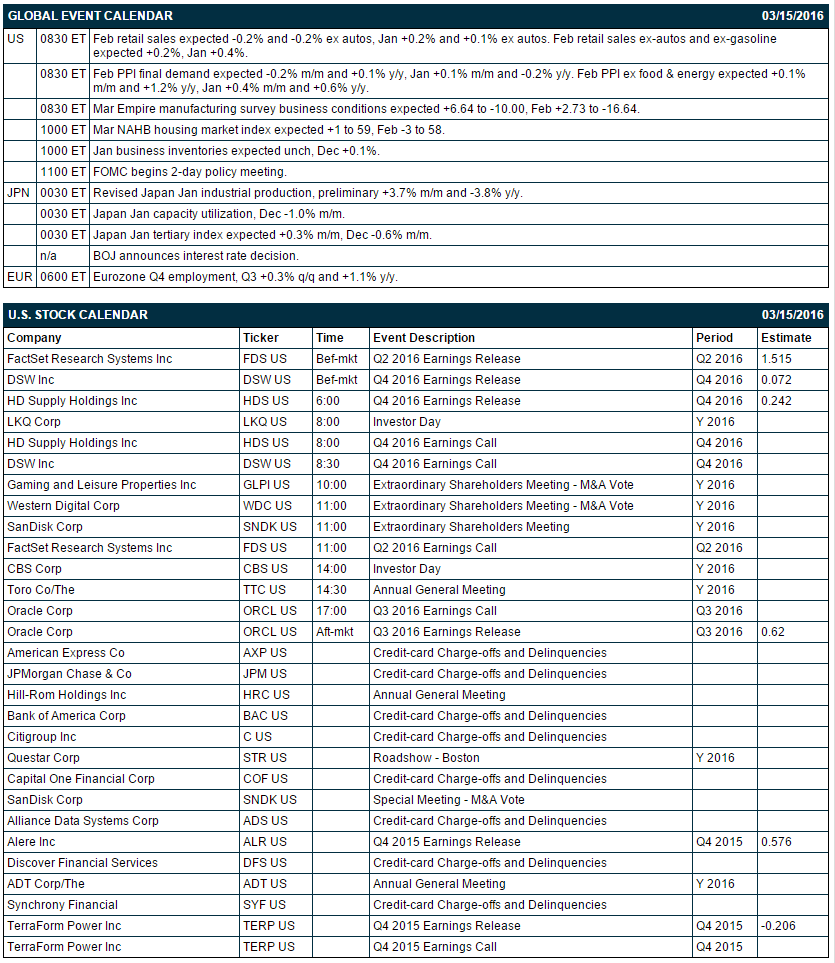

Key U.S. news today includes: Feb retail sales (expected -0.2% and -0.2% ex autos, Jan +0.2% and +0.1% ex autos), (2) Feb final-demand PPI (expected -0.2% m/m and +0.1% y/y, Jan +0.1% m/m and -0.2% y/y) and Feb PPI ex food & energy (expected +0.1% m/m and +1.2% y/y, Jan +0.4% m/m and +0.6% y/y), (3) Mar Empire manufacturing survey business conditions index (expected +6.64 to -10.00, Feb +2.73 to -16.64), (4) Mar NAHB housing market index (expected +1 to 59, Feb -3 to 58), (5) Jan business inventories (expected unch, Dec +0.1%), and (6) the first day of the FOMC's 2-day policy meeting (federal funds rate target expected unchanged at 0.25%-0.50%).

There are 6 of the Russell 1000 companies that report earnings today: Oracle (consensus $0.62), FactSet (1.52), DSW (0.07), HD Supply (0.24), Alere (0.58), TerraForm Power (-0.21).

U.S. IPO's scheduled to price today: Senseonics Holdings (SENH).

Equity conferences this week include: Citi Global Property CEO Conference on Mon-Wed, Bank of America Merrill Lynch Consumer & Retail Tech Conference on Tue-Wed, Barclays Emerging Payments Forum on Tue-Wed, Barclays Capital Global Health Care Conference on Tue-Thu,

3rd Annual Pharma Customer Experience Summit 2016 on Wed, Goldman Sachs Innovation Symposium on Wed, Bank of America Merrill Lynch Global Industrials & EU Autos Conference on Wed-Thu, Evercore ISI Retail Summit on Wed-Thu, ACI European Food & Beverage Plastic Packaging Conference on Thu, and Citigroup Retail Madness Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Schlumberger Ltd. (SLB -2.08%) is down over 1% in pre-market trading as the price of crude oil dropped to a 1-week low.

Tiffany (TIF +0.03%) was downgraded to 'Neutral' from 'Buy' at Citigroup.

Freeport-McMoRan (FCX +4.40%) is down over 5% in pre-market trading as metals declined with the price of gold at a 1-1/2 week low.

Delphi Automotive (DLPH -0.31%) was upgraded to 'Buy' from 'Neutral' at UBS with a price target of $88.

Cardinal Health (CAH -0.32%) was downgraded to 'Market Perform' from 'Outperform' at Cowen.

TeleTech Holdings (TTEC +0.07%) reported Q4 adjusted EPS of 47 cents, below consensus of 52 cents.

Outerwall (OUTR +0.73%) rose 9% in after-hours trading after it boosted its quarterly dividend by 100% to 60 cents a share and said it hired Morgan Stanley for strategic and financial alternatives.

Black Diamond (BDE -4.50%) rallied over 12% in after-hours trading after it reported Q4 adjusted EPS of 2 cents, better than consensus of a -1 cent loss.

Dover (DOV -0.70%) may be active today after the CEO said in after-hours trading that it sees Q1 results "well below our prior expectations."

MannKind (MNKD +4.51%) slumped over 10% in after-hours trading after it reported a Q4 loss of -66 cents, a much bigger loss than consensus of -5 cents.

InVivo Therapeutics Holdings (NVIV -4.74%) dropped over 8% in after-hours trading after it announced a public offering of stock and warrants, packaged as units. Prices and volumes have yet to be announced.

Biocryst Pharmaceuticals (BCRX -1.41%) rose over 5% in after-hours trading after D.E. Shaw raised his passive stake in the company to 5.1% from 3.5%.

Inigen (INGN +3.09%) jumped over 12% in after-hours trading after reported Q$ EPS of 19 cents, well above consensus of 7 cents, and raised guidance on 2016 revenue to $187 million-$191 million from a prior projection of $177 million-$181 million, above consensus of $181 million.

Amphastar Pharmaceuticals (AMPH +2.99%) climbed over 8% in after-hours trading after it reported Q4 adjusted EPS of 19 cents, well above consensus for a -5 cent loss.

Immunomedics (IMMU +3.92%) slumped over 15% in after-hours trading after it terminated a Phase 3 trial after patients with metastatic pancreatic cancer showed no improvement after receiving it its 90Y clivatuzumab tetraxetan.

Celator Pharmaceuticals (CPXX +9.80%) exploded over 300% higher in after-hours trading after it announced positive results from a Phase 3 clinical trial on usage of its Vyxeos Liposome for treatment of patients with acute myeloid leukemia,

MARKET COMMENTS

Jun E-mini S&Ps (ESM16 -0.56%) this morning are down -10.00 points (-0.50%). Monday's closes: S&P 500 -0.13%, Dow Jones +0.09%, Nasdaq +0.13%. The S&P 500 on Monday closed lower on weakness in energy producer stocks after crude oil sold off by -3.4% and on position-squaring ahead of the 2-day FOMC meeting that begins Tuesday. Stocks found supported from a +1.75% rally in China's Shanghai Composite and increased M&A activity after Apollo Global offered to buy Fresh Market for $1.4 billion.

Jun 10-year T-notes (ZNM16 +0.16%) this morning are up +6 ticks. Monday's closes: TYM6 +2.50, FVM6 +0.50. Jun T-notes on Monday closed higher on increased safe-haven demand with the sell-off in stocks and on the -3.4% slide in crude oil prices that pushed inflation expectations lower.

The dollar index (DXY00 +0.11%) this morning is up +0.185 (+0.19%). EUR/USD ^EURUSD) is down -0.0014 (-0.13%). USD/JPY (^USDJPY)is down-0.71 (-0.62%). Monday's closes: Dollar Index +0.452 (+0.47%), EUR/USD -0.0053 (-0.48%), USD/JPY -0.04 (-0.04%). The dollar index on Monday settled higher on the sell-off in crude oil, which undercut the currencies of the crude exporting countries of Russia and Canada against the dollar. The dollar was also boosted by weakness in EUR/USD on the prospects for the Fed to keep raising interest rates while the ECB maintains or even expands stimulus measures.

Apr WTI crude (CLJ16 -2.50%) this morning is down -91 cents (-2.45%) at a 1-week low and Apr gasoline (RBJ16 -2.17%) is down -0.0268 (-1.88%). Monday's closes: CLJ6 -1.32 (-3.43%), RBJ6 -0.0217 (-1.50%). Apr crude oil and gasoline on Monday closed lower on the stronger dollar and on Iranian Oil Minister Bijan Namdar Zanganreh's comment that Iran plans to boost its crude production by about a third to 4 million bpd before it will consider joining any move to rebalance the market.

Disclosure: None.