Morning Call For June 30, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 +0.17%) are up +0.25% and European stocks are up +0.80%. A rally in U.S. bank stocks is leading the overall market higher with Goldman Sachs, Bank of America and Citigroup all up over 1% in pre-market trading after they passed the Fed's annual stress tests and said they will increase their stock buyback programs. A +0.16% gain in copper prices (HGU16 -0.05%) to a 1-3/4 month high is giving European mining stocks a lift, as is data that showed German May retail sales rose +0.9% m/m, the biggest increase in 10 months. Asian stocks settled mostly higher: Japan +0.06%, Hong Kong +1,75%, China -0.07%, Taiwan +0.93%, Australia +1,77%, Singapore +1.73%, South Korea +0.75%, India +0.97%.

The dollar index (DXY00 -0.33%) is down -0.31%. EUR/USD (^EURUSD) is up +0.16% after Eurozone Jun CPI rose more than expected, which reduces the chances of additional ECB stimulus. USD/JPY (^USDJPY) is down -0.04%.

Sep T-note prices (ZNU16 -0.26%) are down -13.5 ticks.

German May retail sales rose +0.9% m/m, stronger than expectations of +0.6% m/m and the largest increase in 10 months.

The Eurozone Jun CPI estimate rose +0.1% y/y, stronger than expectations of unch y/y. The Jun core CPI rose +0.9% y/y, stronger than expectations of +0.8% y/y.

U.S. STOCK PREVIEW

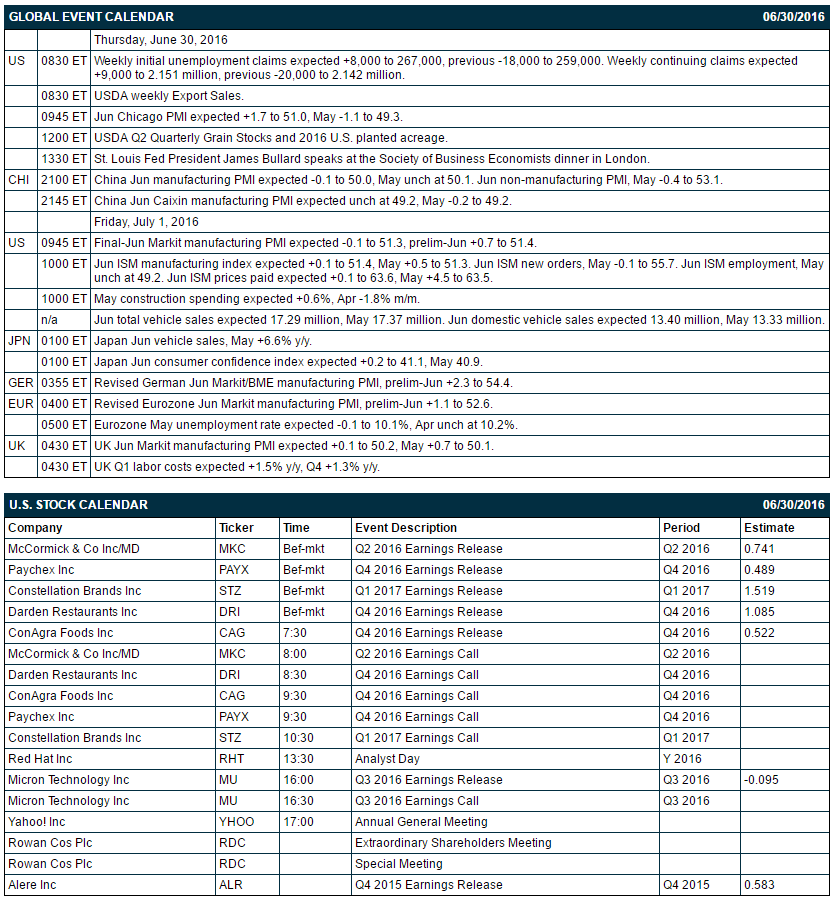

Key U.S. news today includes: (1) weekly initial unemployment claims (expected +8,000 to 267,000, previous -18,000 to 259,000) and continuing claims (expected +9,000 to 2.151 million, previous -20,000 to 2.142 million), (2) Jun Chicago PMI (expected +1.7 to 51.0, May -1.1 to 49.3), (3) St. Louis Fed President James Bullard speaks at the Society of Business Economists’ dinner in London, (4) USDA weekly Export Sales, and (5) USDA Q2 Quarterly Grain Stocks and 2016 U.S. planted acreage.

There are 7 of the Russell 1000 companies report earnings today: McCormick (consensus $0.74), Paychex (0.49), Constellation Brands (1.52), Darden Restaurants (1.09), ConAgra Foods (0.52), Micron Technology (-0.10), Alere (0.58).

U.S. IPO's scheduled to price today: Tactile Systems Technology (TCMD)

Equity conferences during the remainder of this week include: none.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM +2.82%) , Bank of America (BAC +3.86%) ,and Goldman Sachs (GS +2.17%) all rose over 1% in pre-market trading after they passed the Fed's CCAR stress tests without conditions.

Marriott International (MAR +3.69%) was upgraded to 'Buy' from 'Hold' at Evercore ISI with a price target of $75.

American International Group (AIG +3.29%) was upgraded to 'Overweight' from 'Neutral' at Atlantic Equities with a 12-month price target of $60.

Progress Software (PRGS +1.74%) rallied 5% in after-hours trading after it reported Q2 adjusted EPS of 33 cents, higher than consensus of 29 cents.

CIT Group (CIT +4.28%) climbed 6% in after-hours trading after it sold its Canadian Equipment Finance and Corporate Finance businesses to Laurentian Bank of Canada.

Pier 1 Imports (PIR +4.02%) slid 3% in after-hours trading after it lowered guidance on full-year adjusted EPS to 32 cents-40 cents from an April 13 view of 42 cents-50 cents.

Shutterstock (SSTK +4.47%) rose over 1% in after-hours trading after it was announced that it will replace Southwest Gas in the S&P Smallcap 600.

Alliant Energy (LNT +0.03%) gained 0.5% in after-hours trading after it was announced that it will replace AGL Resources in the S&P 500 after the close of trading on Thursday, June 30.

Tractor Supply (TSCO +1.06%) dropped over 7% in after-hours trading after it reported Q2 revenue of $1.85 billion, below consensus of $1.93 billion, and then lowered guidance on full-year EPS to $3.35-$3.40 from a prior view of $3.40-$3.48.

Citigroup (C +4.15%) rose over 2% in after-hours trading after it announced a $8.6 billion stock buyback and said it will lift its quarterly dividend to 16 cents from 5 cents.

Stone Energy (SGY +4.03%) jumped over 7% in after-hours trading after it said it ended its pact with ESV and ended its contract with Midstream and entered into a new gas gathering, processing pact with Williams at Mary Field in Appalachia.

Care.com (CRCM +2.79%) surged 18% in after-hours trading after it received a $46.35 million investment from Google Capital, who will add a representative to CRCM's board and is now the company's largest shareholder.

MARKET COMMENTS

September E-mini S&Ps (ESU16 +0.17%) this morning are up +5.25 points (+0.25%). Wednesday's closes: S&P 500 +1.70%, Dow Jones +1.64%, Nasdaq +1.73%. The S&P 500 on Wednesday closed sharply higher on reduced Brexit concerns on speculation global central banks will take the necessary measures to mitigate the damage done by the UK's decision to leave the European Union. Stocks were also boosted by the as-expected +0.4% increase in U.S. May personal spending and by strength in energy producers after crude oil prices climbed +4.24%. Stocks were undercut by the-3.7% m/m decline in U.S. May pending home sales, the largest monthly decline in 6 years.

Sep 10-year T-note prices (ZNU16 -0.26%) this morning are down -13.5 ticks. Wednesday's closes: TYU6 -6.00. FVU6 -4.00. Sep T-notes on Wednesday closed lower on reduced safe-haven demand with the 2-day recovery rally in stocks and the Atlanta Fed's hike in its U.S. Q2 GDP estimate to 2.7% from a previous estimate of 2.6%.

The dollar index (DXY00 -0.33%) this morning is down -0.296 (-0.31%). EUR/USD (^EURUSD) is up +0.0018 (+0.16%). USD/JPY (^USDJPY) is down-0.04 (-0.04%). Wednesday's closes: Dollar Index -0.476 (-0.49%), EUR/USD +0.0060 (+0.54%), USD/JPY +0.08 (+0.08%). The dollar index on Wednesday closed lower on the weaker-than-expected U.S. May pending home sales report of -3.7% and the as-expected increase in German Jun CPI, which may keep the ECB from expanding stimulus and boosted EUR/USD.

Aug WTI crude oil (CLQ16 -1.06%) this morning is down -43 cents (-0.86%). Aug gasoline (RBQ16 -0.13%) is up +0.0002 (+0.01%). Wednesday's closes: CLQ6 +2.03 (+4.24%), RBQ6 +0.0184 (+1.21%). Aug crude oil and gasoline on Wednesday settled higher on the weaker dollar and the -4.05million bbl decline in EIA crude inventories (vs expectations of -2.5 million bbl). Crude oil was also boosted by the -0.6% drop in U.S. crude production in the week ended Jun 24 to a 1-3/4 year low of 8.622 million bpd. Gasoline prices were undercut on news that EIA gasoline stockpiles unexpectedly rose +1.37 million bbl, more than expectations for a -300,000 bbl decline.

Disclosure: None.