Morning Call For June 3, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.49%) this morning are up +0.27% and European stocks are up +0.68% ahead of the ECB meeting. European stocks received a boost on stronger-than-expected economic data on Eurozone Apr retail sales that rose +0.7% m/m, the most in 15 months, and after Eurozone Apr unemployment fell -0.1 to 11.1%, the lowest in 3 years. Bank stocks also gave the overall market a boost as Credit Suisse climbed nearly 3% after RBC upgraded the lender to 'Outperform' from 'Sector Perform.' Another positive for European stocks is the decline in the Greek 10-year bond yield to a 2-week low of 10.92% on optimism that a solution to the Greek debt crisis can soon be found. Stock prices climbed even after the OECD cut its 2015 global GDP forecast to 3.1% from a 3.7% estimate in Oct. Asian stocks closed mostly lower: Japan -0.34%, Hong Kong +0.69%, China -0.01%, Taiwan -0.60%, Australia -0.93%, Singapore +0.27%, South Korea -0.85%, India -1.29%.

Commodity prices are mostly lower as the dollar strengthened. Jul crude oil (CLN15 -2.07%) is down -2.20% and Jul gasoline (RBN15 -2.11%) is down -2.16%. Metals prices are weaker. Aug gold (GCQ15 -0.35%) is down -0.50% and Jul copper (HGN15 -0.35%) is down -0.51%. Agricultural prices are lower.

The dollar index (DXY00 +0.34%) is up +0.42%. EUR/USD (^EURUSD) is down -0.26%. USD/JPY (^USDJPY) is up +0.28%.

Sep T-note prices (ZNU15 -0.14%) are down -4 ticks at a 2-week low.

The Organization for Economic Cooperation and Development (OECD) lowered its 2015 global growth forecast to 3.1% from a 3.7% estimate in Oct, saying investment is lagging and risks including a possible Greek default are hurting confidence. The OECD cut its 2015 U.S. GDP forecast to 2.0% from a Mar estimate of 3.1%.

Eurozone Apr retail sales rose +0.7% m/m, stronger than expectations of +0.6% m/m and the most in 15 months. On an annual basis, Apr retail sales rose +2.2% y/y, stronger than expectations of +2.0% y/y.

The Eurozone Apr unemployment rate fell -0.1 to 11.1% from a downward revised 11.2% in Mar, better than expectations of -0.1 to 11.2% and the lowest in 3 years.

U.S. STOCK PREVIEW

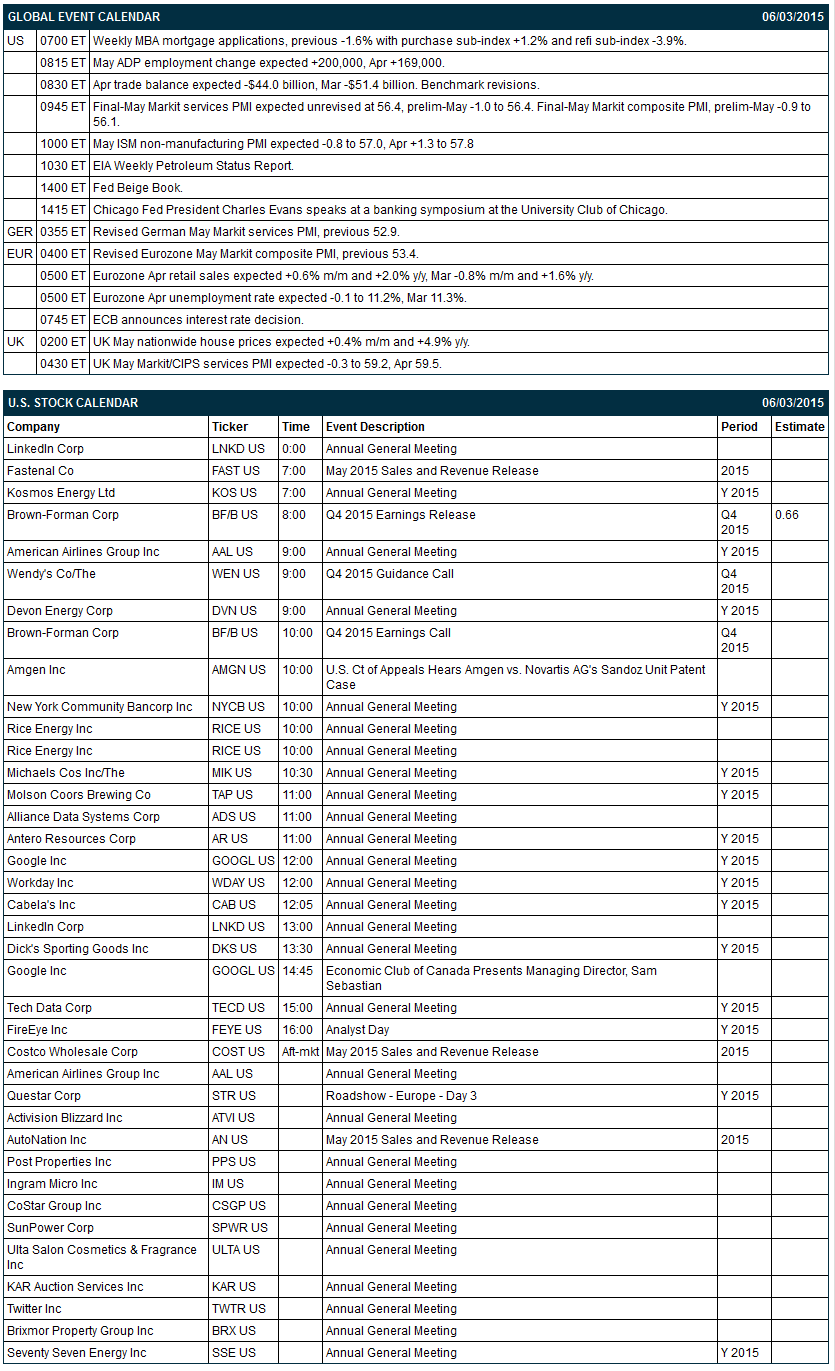

Key U.S. news today includes: (1) weekly MBA mortgage applications (last week -1.6% with purchase sub-index +1.2% and refi sub-index -3.9%), (2) May ADP employment change (expected +200,000 after April's +169,000), (3) Apr trade deficit (expected -$44.0 billion after March's -$51.4 billion), (4) final-May Markit services PMI (expected unrevised at 56.4 after prelim-May -1.0 to 56.4), (5) May ISM non-manufacturing PMI (expected -0.8 to 57.0), (6) Fed Beige Book, and (7) a speech by Chicago Fed President Charles Evans at a banking symposium at the University Club of Chicago.

There is 1 of the Russell 1000 companies that reports earnings today: Brown-Forman (consensus $0.66).

U.S. IPO's scheduled to price today include: PennTex Midstream Partners (PTXP), VWR Corp (VWR), Molina Healthcare (MOH), AerCap Holdings (AER), STORE Capital (STOR).

Equity conferences during the remainder of this week include: Jefferies Global Healthcare Conference on Mon-Wed, Bank of America Merrill Lynch Global Technology Conference on Tue-Wed, Deutsche Bank Global Financial Services Investor Conference on Tue-Wed, KBW Asset Management and Capital Markets Conference on Wed, Sandler O'Neill & Partners Global Exchange and Brokerage Conference on Wed, Deutsche Bank Global Industrials and Basic Materials Conference on Wed-Thu, FBN Securities: Field Trip - 8th Semi-Annual Silicon Valley Tour on Wed-Thu, Credit Suisse Engineering & Construction Conference on Thu, Morgan Stanley Leveraged Finance Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Actavis (ACT -1.12%) was initiated with an 'Outperform' at Raymond James with a price target of $344.

Dean Foods (DF -0.43%) was downgraded to 'Equal Weight' from 'Overweight' at Morgan Stanley.

Humana (HUM -0.08%) was upgraded to 'Neutral' from 'Underperform' at Sterne Agee CRT.

Piper Jaffray reiterates an 'Overweight' rating on Amazon.com (AMZN +0.02%) and rasies the price target on the stock to $520 from $475.

Caterpillar (CAT +0.75%) was initiated with a 'Buy' at Societe Generale with a price target of $110.

Expedia (EXPE +0.17%) was initiated with an 'Overweight' at Barclays with a price target of $125.

Genesco (GCO +1.88%) was downgraded to 'Sell' from 'Neutral' at Goldman Sachs.

Charles Schwab (SCHW +0.60%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $39.

Legg Mason (LM +0.06%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $65.

CNBC reports that Hewlett-Packard's (HPQ +0.36%) separation into HP Inc. and Hewlett-Packard Enterprise will be effective Nov 1.

Ciena (CIEN +0.62%) was initiated with a 'Buy' at Nomura with a price target of $29.

ABM Industries (ABM -0.34%) reports Q2 adjusted EPS of 37 cents, higher than consensus of 35 cents.

Guess (GES +6.21%) reported an unexpected Q1 EPS profit of 4 cents, better than consensus of a -5 cent loss, although Q1 revenue of $478.8 million was below consensus of $483.8 million.

Ascena Retail (ASNA -0.61%) reported Q3 EPS of 18 cents, weaker than consensus of 20 cents.

G-III Apparel (GIII +3.30%) climbed over 4% in after-hours trading after it reported Q1 EPS of 15 cents, more than double consensus of 7 cents, and then raised guidance on fiscal 2016 EPS view to $2.66-$2.76 from $2.53-$2.63, above consensus of $2.62.

MARKET COMMENTS

June E-mini S&Ps (ESM15 +0.49%) this morning are up +5.75 points (+0.27%). Tuesday's closes: S&P 500 -0.10%, Dow Jones -0.16%, Nasdaq -0.29%. The S&P 500 on Tuesday slid to a 2-1/2 week low and closed lower on the -0.4% decline in U.S. Apr factory orders, weaker than expectations of -0.1%, and on a slide in utility companies caused by a rise in the 10-year T-note yield to a 1-1/2 week high. Stocks received support from Fed Governor Brainard's comment that she may favor waiting to raise interest rates.

Sep 10-year T-notes (ZNU15 -0.14%) this morning are down -4 ticks at a 2-week low. Tuesday's closes: TYU5 -19.00, FVU5 -8.00. Sep T-notes on Tuesday sold-off to a 1-1/2 week low and closed lower on carry-over weakness from a slide in German bund prices to a 2-week low on reduced deflation concerns after Eurozone May CPI rose more than expected. In addition, there was reduced safe-haven demand for T-notes on optimism a Greek bailout deal may be closer after EU Economic Commissioner Moscovici said there was "real progress" in negotiations.

The dollar index (DXY00 +0.34%) this morning is up +0.402 (+0.42%). EUR/USD (^EURUSD) is down -0.0029 (-0.26%). USD/JPY (^USDJPY) is up +0.35 (+0.28%). Tuesday's closes: Dollar Index -1.557 (-1.60%), EUR/USD +0.02242 (+2.05%), USD/JPY -0.673 (-0.54%). The dollar index on Tuesday dropped to a 1-week low and closed sharply lower on Fed Governor Brainard's indication that she may favor delaying an interest rate hike when she said "the string of soft data in Q1 raises some questions about the contours of the economic outlook." In addition, EUR/USD rallied sharply on reduced deflation concerns after the Eurozone May CPI estimate rose +0.3% y/y, more than expectations of +0.2% y/y and the first increase in 6 months.

July WTI crude oil (CLN15 -2.07%) this morning is down -$1.35 a barrel (-2.20%). July gasoline (RBN15 -2.11%) is down -0.0445 (-2.16%). Tuesday's closes: CLN5 +1.06 (+1.76%), RBN5 +0.0167 (+0.82%). July crude oil and gasoline closed higher Tuesday with Jul crude at a 3-week high on the sharp sell-off in the dollar index and on expectations for Wednesday' weekly EIA crude inventories to fall -2.5 million bbl, the fifth straight weekly decline.

Click on picture to enlarge

Disclosure: None.