Morning Call For June 23, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 +0.99%) are up sharply by +0.99% at a 1-1/2 week high and European stocks are up +2.34% at a 3-week high as the UK referendum on membership in the European Union is under way. Optimism is high that Britain will vote to remain in the EU as GBP/USD soared +1.13% to a 5-3/4 month high. Global government bonds and the price of gold tumbled to 2-week lows with the surge in equity markets. Copper prices (HGN16 +0.61%) jumped to a 1-1/2 month high and European stocks also found support on an unexpected increase in the Eurozone Jun Markit manufacturing PMI to its fastest pace of expansion in 6 months. Asian stocks settled mixed: Japan +1.07%, Hong Kong +0.35%, China -0.47%, Taiwan -0.45%, Australia +0.18%, Singapore +0.28%, South Korea -0.18%, India +0.88%.

The dollar index (DXY00 -0.54%) is down -0.60% at a 1-1/2 month low. EUR/USD (^EURUSD) is up +0.91% at a 2-week high. USD/JPY (^USDJPY) is up +1.34% at a 1-week high.

Sep T-note prices (ZNU16 -0.31%) are down -13.5 ticks at a 2-week low.

The Eurozone Jun Markit manufacturing PMI unexpectedly rose +1.1 to 52.6, stronger than expectations of -0.1 to 51.4 and the fastest pace of expansion in 6 months.

U.S. STOCK PREVIEW

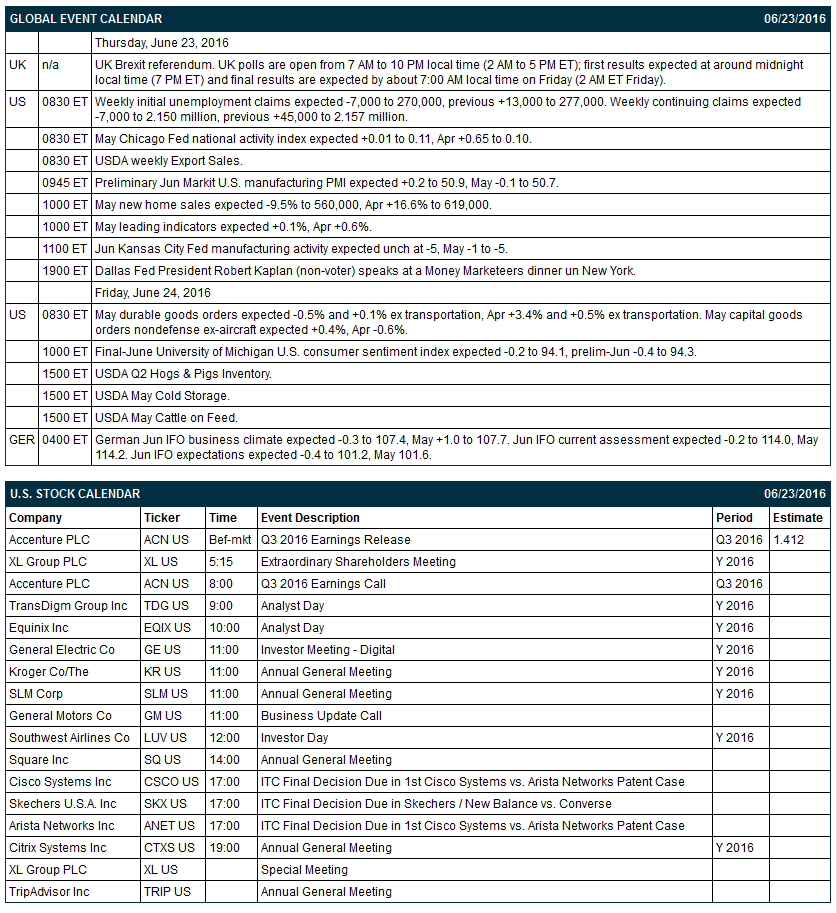

Key U.S. news today includes: (1) today's Brexit vote in the UK, (2) weekly initial unemployment claims (expected -7,000 to 270,000, previous +13,000 to 277,000) and continuing claims (expected -13,000 to 2.144 million, previous +45,000 to 2.157 million), (3) May Chicago Fed national activity index (expected +0.01 to 0.11, Apr +0.65 to 0.10), (4) preliminary Jun Markit U.S. manufacturing PMI (expected +0.2 to 50.9, May -0.1 to 50.7), (5) May new home sales (expected -9.5% to 560,000, Apr +16.6% to 619,000), (6) May leading indicators (expected +0.1%, Apr +0.6%), (7) Jun Kansas City Fed manufacturing activity (expected unch at -5, May -1 to -5), (8) Dallas Fed President Robert Kaplan (non-voter) speaks at a Money Marketeers dinner un New York, and (9) USDA weekly Export Sales.

There is 1 of the Russell 1000 companies that reports earnings today: Accenture (consensus $1.41).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week include: Citigroup Insurance Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Herman Miller (MLHR -0.86%) climbed over 5% in after-hours trading after it reported Q4 adjusted EPS of 56 cents, higher than consensus of 52 cents, and said it sees Q1 adjusted EPS of 60 cents-64 cents, above consensus of 60 cents.

Amazon.com (AMZN -0.73%) was rated a new 'Buy' at Maxim Group with a 12-month price target of $825.

Home Depot (HD -0.11%) was upgraded to 'Buy' from 'Neutral' at Nomura with a price target of $155.

Intuit (INTU -1.34%) was added to America's 'COnviction Buy List' at Goldman Sachs.

CACI International (CACI -0.57%) said it sees fiscal 2017 EPS of $6.02-$6.43, below consensus of $6.50.

Steelcase (SCS -0.87%) slid 4% in after-hours trading after it said it sees Q2 adjusted EPS of 29 cents-33 cents, below consensus of 37 cents.

Apogee Enterprises (APOG -4.22%) jumped over 9% in after-hours trading after it reported Q1 EPS of 61 cents, well above consensus of 49 cents, and then raised guidance on fiscal 2017 EPS to $2.70-$2.85 from an April 6 view of $2.65-$2.80.

Bed Bath & Beyond (BBBY -0.35%) fell nearly 6% in after-hours trading after it reported Q1 EPS of 80 cents, below consensus of 86 cents.

Red Hat (RHT -0.80%) dropped over 5% in after-hours trading after it lowered guidance on fiscal 2017 adjusted EPS to $2.19-$2.23 from a March 22 view of $2.22-$2.26.

H.B. Fuller (FUL -0.45%) reported Q2 adjusted EPS of 67 cents, weaker than consensus of 68 cents.

CubeSmart (CUBE +0.57%) was rated a new 'Outperform' at FBR Capital Markets with a 12-month price target of $35.

The U.S. Department of Defense said Harris Corp. (HRS -0.13%) won a $1.7 billion army contract for radios, ancillaries, spare parts and services for Afghanistan.

Weyerhaeuser (WY +0.14%) said it will close 2 of its 3 lumber and plywood mills in Columbia Falls, Montana this summer and approximately 100 positions will be eliminated.

SolarCity (SCTY +3.26%) fell over 2% in after-hours trading after Citron Research founder Andrew Left said that SolarCity "is not even technology. It's a subprime lender" and that he sees the stock price going to zero.

MARKET COMMENTS

September E-mini S&Ps (ESU16 +0.99%) this morning are up sharply by +20.50 points (+0.99%) at a 1-1/2 week high. Wednesday's closes: S&P 500 -0.17%, Dow Jones -0.27%, Nasdaq -0.20%. The S&P 500 on Wednesday closed lower on the IMF's cut in its U.S. 2016 GDP estimate to 2.2% from 2.4% and on long liquidation pressure ahead of Thursday's UK Brexit vote. Stocks found support on the +1.8% increase in U.S. May existing home sales to a 9-1/4 year high of 5.53 million.

Sep 10-year T-note prices (ZNU16 -0.31%) this morning are down -13.5 ticks at a 2-week low. Wednesday's closes: TYU6 +3.00, FVU6 +2.25. Sep T-notes on Wednesday closed higher on economic concerns after the IMF cut its U.S. 2016 GDP forecast and on decent demand for the Treasury's $28 billion 7-year T-note auction that had a 2.56 bid-to-cover ratio, above the 12-auction average of 2.49.

The dollar index (DXY00 -0.54%) this morning is down -0.565 (-0.60%) at a 1-1/2 month low. EUR/USD (^EURUSD) is up +0.0103 (+0.91%) at a 2-week high. USD/JPY (^USDJPY) is up +1.40 (+1.34%) at a 1-week high. Wednesday's closes: Dollar Index -0.301 (-0.32%), EUR/USD +0.0054 (+0.48%), USD/JPY -0.34 (-0.32%). The dollar index on Wednesday closed lower on strength in GBP/USD as Brexit concerns eased on optimism the UK will vote Thursday to remain in the European Union. The dollar was also undercut by cautious comments from Fed Chair Yellen that signal the Fed may be slow to raise interest rates when she said the "headwinds" of weak productivity growth and tepid business investment may only slowly fade over time.

Aug WTI crude oil (CLQ16 +1.47%) this morning is up +64 cents (+1.30%). Aug gasoline (RBQ16 +0.88%) is up +0.0087 (+0.55%). Wednesday's closes: CLQ6 -0.72 (-1.44%), RBQ6 -0.0086 (-0.54%). Aug crude and gasoline on Wednesday both fell back from 1-week highs and closed lower. Crude oil prices were undercut by the -917,000 bbl decline in EIA crude inventories (less than expectations of -1.5 million bbl) and the unexpected +627,000 bbl increase in EIA gasoline inventories, more than expectations of -1.0 million bbl. Crude oil found support on a weaker dollar and the -0.4% decline in U.S. crude production in the week ended Jun 17 to a 1-3/4 year low of 8.677 million bpd.

(Click on image to enlarge)

Disclosure: None.