Morning Call For June 2, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 -0.25%) this morning are down -0.20% and European stocks are down -0.13%, both at 2-week lows, although prices recovered from their worst levels on optimism over an end to the Greek credit impasse after EU Economic Commissioner Moscovici said there was "real progress" in talks. IMF chief Lagarde met with German Chancellor Merkel, ECB President Draghi and European Commission President Juncker at the German Chancellery in Berlin on Monday night in an attempt to forge a plan to unlock bailout funds for Greece. Although Greece says it can make a debt repayment due to the IMF on Friday, it is the smallest of four payments due this month that total almost 1.6 billion euros. Asian stocks closed mixed: Japan -0.13%, Hong Kong -0.47%, China +1.69%, Taiwan -0.12%, Australia -1.73%, Singapore -1.61%, South Korea -0.95%, India -2.37%. India's BSE Sensex 30 Stock Index fell over 2% even after the RBI lowered interest rates for the third time this year as the central bank cut its growth estimates for India.

Commodity prices are mostly higher. Jul crude oil (CLN15 +1.31%) is up +0.95% at a 2-week high and Jul gasoline (RBN15 +0.33%) is up +0.11%. Metals prices are higher. Aug gold (GCQ15 +0.14%) is up +0.13% and Jul copper (HGN15 +0.17%) is up +0.15%. Agricultural prices are stronger.

The dollar index (DXY00 -0.59%) is down -0.53%. EUR/USD (^EURUSD) is up +0.95% on reduced deflation concerns after Eurozone consumer prices rose or the first time in 6 months. USD/JPY (^USDJPY) is up +0.02% at a fresh 12-1/2 year high.

Sep T-note prices (ZNU15 -0.25%) are down -6.5 ticks at a 1-week low.

The Reserve Bank of India (RBI) cut its benchmark repurchase rate by 25 bp to 7.25%, right on expectations and the third interest rate cut this year. The RBI also lowered its gross value added (GVA), a component of GDP watched closely by the RBI, to 7.6% in the year though Mar 2016 from a previous estimate of 7.8%.

The Eurozone May CPI estimate rose +0.3% y/y, stronger than expectations of +0.2% y/y and the largest increase in 6 months. The May core CPI climbed +0.9% y/y, stronger than expectations of +0.7% y/y and the fastest pace of increase in 9 months.

U.S. STOCK PREVIEW

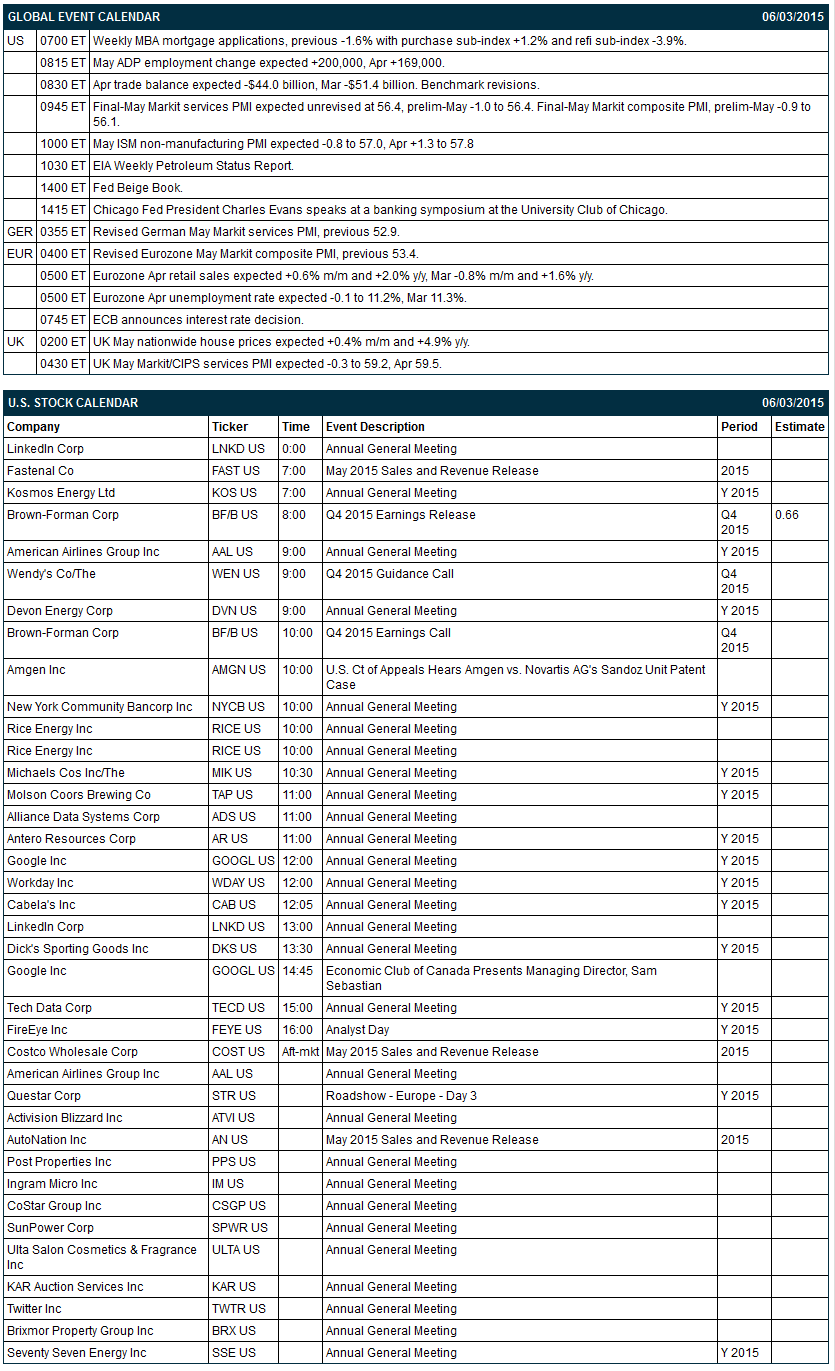

Key U.S. news today includes: (1) May New York ISM (April was +8.1 to 58.1), (2) Apr factory orders (expected -0.1% after March's +2.1% and -0.1% ex-transportation), (3) a speech by Fed Governor Lael Brainard on the U.S. economic outlook and monetary policy at the Center for Strategic and International Studies, and (4) May total vehicle sales (expected 17.10 million units vs April's 16.46 million).

There are 3 of the Russell 1000 companies that report earnings today: Dollar General (consensus $0.81), Medtronic (1.12), Ascena Retail Group (0.20).

U.S. IPO's scheduled to price today include: Nevro Corp (NVRO), Catalent (CTLT), Ferrellgas Partners (FGP), Intersect ENT (XENT).

Equity conferences during the remainder of this week include: American Society of Clinical Oncology Meeting on Mon-Tue, Andean Institutional Real Estate Forum on Mon-Tue, RBC - Conference: Global Energy & Power Executive Conference - New York on Mon-Tue, Jefferies Global Healthcare Conference on Mon-Wed, Bank of America Merrill Lynch Global Telecom & Media Conference on Tue, Goldman Sachs Lodging, Gaming, Restaurant and Leisure Conference on Tue, Keefe, Bruyette, & Woods Mortgage Finance Conference on Tue, RBC Global Energy Conference on Tue, Bank of America Merrill Lynch Global Technology Conference on Tue-Wed, Deutsche Bank Global Financial Services Investor Conference on Tue-Wed, KBW Asset Management and Capital Markets Conference on Wed, Sandler O'Neill & Partners Global Exchange and Brokerage Conference on Wed, Deutsche Bank Global Industrials and Basic Materials Conference on Wed-Thu, FBN Securities: Field Trip - 8th Semi-Annual Silicon Valley Tour on Wed-Thu, Credit Suisse Engineering & Construction Conference on Thu, Morgan Stanley Leveraged Finance Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Intel (INTC -1.63%) was downgraded to 'Market Perform' from 'Outperform' at BMO Capital.

Big Lots (BIG +2.26%) was upgraded to 'Overweight' from 'Equal Weight' at Barclays.

Iron Mountain (IRM +0.99%) was downgraded to 'Underperform' from 'Hold' at Jefferies.

Medtronic PLC (MDT +0.50%) reported Q4 EPS of $1.16, higher than consensus of $1.12.

Dollar General (DG +0.30%) reported Q1 EPS of 84 cents, better than consensus of 81 cents.

Glenview Capital reported a 7.06% stake in Manitowoc (MTW +2.33%) .

Whiting Petroleum (WLL -1.55%) was initiated with a Buy at Evercore ISI with a price target of $45.

Prudential (PRU -0.34%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $106.

AIG (AIG +0.12%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $73.

Anadarko (APC +0.28%) was initiated with a 'Buy' at Evercore ISI with a price target of $100.

Palo Alto (PANW +0.60%) was initiated with a 'Buy' at Guggenheim with a price target of $200.

Point72 Asset reported a 5.1% passive stake in Renewable Energy (REGI +16.46%) .

PVH Corp. (PVH +0.04%) reported Q1 adjusted EPS of $1.50, better than consensus of $1.38, and then raised guidance on fiscal 2015 adjusted EPS view to $6.85-$6.95 from $6.75-$6.90, above consensus of $6.86.

MARKET COMMENTS

June E-mini S&Ps (ESM15 -0.25%) this morning are down -4.25 points (-0.20%) at a 2-week low. Monday's closes: S&P 500 +0.21%, Dow Jones +0.16%, Nasdaq +0.30%. The S&P 500 on Monday settled higher on the +1.3 point increase in the May ISM manufacturing index to 52.8 (stronger than expectations of +0.5 to 52.0) and the +2.2% jump in U.S. Apr construction spending, which was the biggest increase in 2-3/4 years.

Sep 10-year T-notes (ZNU15 -0.25%) this morning are down -6.5 ticks at a 1-week low. Monday's closes: TYU5 -25.00, FVU5 -14.50. Sep T-notes Monday closed lower on the stronger-than-expected May ISM manufacturing report and the +2.2% increase in U.S. Apr construction spending, which may prompt the Fed to raise interest rates sooner rather than later.

The dollar index (DXY00 -0.59%) this morning is down -0.518 (-0.53%). EUR/USD (^EURUSD) is up +0.0104 (+0.95%). USD/JPY (^USDJPY) is up +0.02 (+0.02%) at a fresh 12-1/2 year high. Monday's closes: Dollar Index +0.485 (+0.50%), EUR/USD -0.00662 (-0.60%), USD/JPY +0.644 (+0.52%). The dollar index on Monday closed higher on the stronger-than-expected U.S. May ISM manufacturing and April construction spending reports, which bolster the case for Fed rate hikes sooner rather than later. The yen showed weakness on poor Japanese interest rate differentials as USD/JPY surged to a 12-1/2 year high.

July WTI crude oil (CLN15 +1.31%) this morning is up +57 cents (+0.95%). July gasoline (RBN15 +0.33%) is up +0.0022 (+0.11%). Monday's closes: CLN5 -0.10 (-0.17%), RBN5 -0.0172 (-0.83%). Jul crude and gasoline on Monday closed lower on the stronger dollar and on record Saudi crude output as Saudi Arabian May oil production was 10.25 million bpd, unch from Apr and the highest since data began in 1962. Other bearish monthly OPEC data included (1) record Iraq oil exports with Iraq May crude exports up +2.2% to a record 3.145 million bpd, and (2) the rise in May OPEC crude production by +67,000 bpd to a 2-1/2 year high of 31.579 million bpd.

Click on picture to enlarge

Disclosure: None.