Morning Call For June 16, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 -0.31%) are down -0.46% and European stocks are down -0.95% at a 3-3/4 month low as Greece and its creditors failed to break an impasse in debt negotiations. A slide in Greek bank stocks pushed Greece' ASE Stock Index down -3.36% and the yield on the Greek 10-year bond climbed to a 1-3/4 month high of 13.07% as Greek default concerns increased after Greek Finance Minister Varoufakis told the Bild newspaper that Greece has no plans to unveil new proposals to end the stalemate in its debt negotiations. European stocks were also pressured by a decline in automakers after data showed Eurozone May new car sales rose at the slowest pace in 6 months. Also, German investor confidence fell for a third month as the German Jun ZEW survey expectations of economic growth fell to a 7-month low. Asian stocks closed mostly lower: Japan -0.64%, Hong Kong -1.10%, China -3.47%, Taiwan -0.50%, Australia -0.05%, Singapore -0.75%, South Korea -0.90%, India +0.38%. China's Shanghai Composite Index tumbled to a 1-1/2 week low amid concern that valuations are outstripping earnings growth.

Commodity prices are mixed. Jul crude oil (CLN15 +0.34%) is up +0.62%, Jul gasoline (RBN15 +0.37%) is up +0.53%. Metals prices are lower. Aug gold (GCQ15 -0.22%) is down -0.21%. Jul copper (HGN15 -0.72%) is down -0.83% at a 2-3/4 month low after LME copper inventories jumped +4,200 MT to a 1-week high of 318,600 MT. Agricultural prices are higher on concern that heavy rains in the Midwest flooded newly planted fields.

The dollar index (DXY00 +0.17%) is up +0.17%. EUR/USD (^EURUSD) is down -0.20%. USD/JPY (^USDJPY) is up +0.11%.

Sep T-note prices (ZNU15 +0.24%) are up +8.5 ticks at a 1-week high as the fall in global equity markets boosted the safe-haven demand for T-notes.

Speaking before the European Parliament in Brussels, ECB President Draghi said that Europe needs a "strong and comprehensive agreement with Greece, and we need this very soon." He added that "the ball lies squarely in the camp of the Greek government to take the necessary steps."

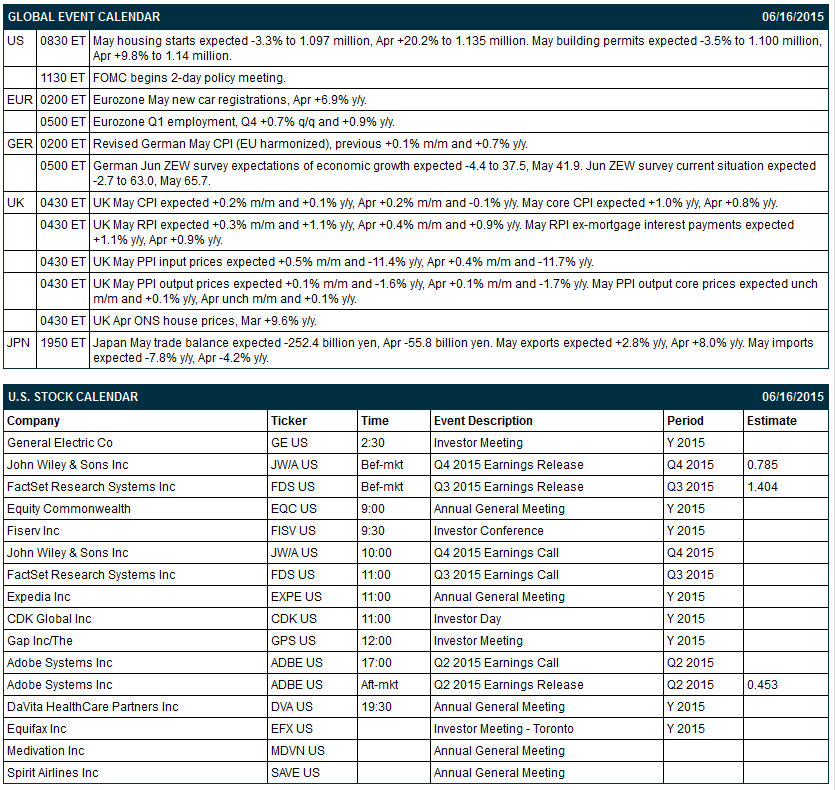

The German Jun ZEW survey expectations of economic growth fell -10.4 to 31.5, weaker than expectations of -4.6 to 37.3 and the lowest in 7 months.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) May housing starts (expected -3.3% to 1.097 million after April's +20.2% to 1.135 million), and (2) the first day of the FOMC's 2-day meeting.

There are 3 of the Russell 1000 companies that report earnings today: John Wiley (consensus $0.79), FactSet (1.40), Adobe (0.45).

U.S. IPO's scheduled to price today include: OM Asset Management (OMAM), Nivalis Therapeutics (NVLS),

Equity conferences during the remainder of this week include: 2015 EIA Energy Conference on Tue, Bloomberg Technology Conference 2015 on Tue, Stifel Industrials Conference on Tue, BIO International Convention on Tue-Wed, Real Estate Investment World Asia 2015 on Wed, Goldman Sachs dotCommerce Day on Thu, JP Morgan Oil & Gas Forum on Thu, Leerink Health Care Services Conference on Thu, Telsey Advisory Group Advertising Trends Symposium on Thu.

OVERNIGHT U.S. STOCK MOVERS

Oshkosh (OSK -2.95%) cut its fiscal 2015 adjusted EPS view to $3.75-$4.00 from $4.00-$4.25, below consensus of $4.04.

AIG (AIG +1.10%) was downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Barrick Gold (ABX +1.77%) was initiated with an 'Outperform' at BMO Capital with a price target of $16.

FreightCar America (RAIL -0.09%) was upgraded to 'Buy' from 'Hold' at Stifel.

Ryland Group (RYL +5.21%) was upgraded to 'Neutral' from 'Underperform' at Credit Suisse.

Twitter (TWTR -3.43%) was downgraded to 'Neutral' from 'Buy' at MKM Partners.

Greenbrier (GBX -0.58%) was downgraded to 'Hold' from 'Buy' at Stifel.

The WSJ reported that Aetna (AET +4.44%) was approached by UnitedHealth (UNH +1.13%) about a merger.

MSD Partners reported a 5.5% passive stake in NorthStar Asset Management (NSAM -1.43%) .

Glenhill Advisors reported a 6.2% passive stake in Pep Boys (PBY -1.76%) .

Goldman Sachs reported a 11.6% passive stake in Enviva (EVA +0.68%) .

Kevin Plank reported a 16.6% stake in Under Armour (UA -0.12%) Class A shares.

AK Steel (AKS -3.75%) announced that it will increase current spot market base prices for all carbon flat-rolled steel products by a minimum of $20 per ton, effective immediately with new orders.

Gap (GPS -0.21%) climbed over 1% in after-hours trading after it announced it will close 175 stores in North America in an attempt to position it for improved business performance.

MARKET COMMENTS

September E-mini S&Ps (ESU15 -0.31%) this morning are down -9.50 ponts (-0.46%). Monday's closes: S&P 500 -0.46%, Dow Jones -0.60%, Nasdaq -0.47%. The S&P 500 on Monday closed lower on (1) Greek concerns after the weekend negotiations broke down, and (2) weaker-than-expected U.S. economic reports. The Jun Empire manufacturing index fell by -5.11 points to a 2-1/3 year low of -1.98 and May industrial production fell by -0.2%. On the positive side, the Jun NAHB housing market index rose +5 points to a 9-month high of 59, stronger than expectations of +2 to 56.

Sep 10-year T-notes (ZNU15 +0.24%) this morning are up +8.5 ticks at a 1-week high. Monday's closes: TYU5 +9.00, FVU5 +5.50. Sep T-notes on Monday climbed to a 1-week high and closed higher on (1) increased safe-haven demand with the sell-off in U.S. and European stocks on Greek default concerns, and (2) the weaker-than-expected Empire and U.S. industrial production reports, which could delay a Fed rate hike.

The dollar index (DXY00 +0.17%) this morning is up +0.165 (+0.17%). EUR/USD (^EURUSD) is down -0.0023 (-0.20%). USD/JPY (^USDJPY) is up +0.13 (+0.11%). Monday's closes: Dollar Index -0.162 (-0.17%), EUR/USD +0.00215 (+0.19%), USD/JPY unch. The dollar index on Monday closed lower on the weaker-than-expected Jun Empire manufacturing index and U.S. May industrial production report. EUR/USD closed mildly higher despite increased concerns about a Greek exit from the Eurozone.

July WTI crude oil (CLN15 +0.34%) this morning is up +37 cents (+0.62%). July gasoline (RBN15 +0.37%) is up +0.0112 (+0.53%). Monday's closes: CLN5 -0.44 (-0.73%), RBN5 -0.0271 (-1.28%). Jul crude and gasoline closed lower for a third day on weaker-than-expected U.S. economic data that signals reduced energy demand after the Jun Empire manufacturing survey unexpectedly contracted and after May industrial production unexpectedly declined.

Click on picture to enlarge

Disclosure: None.