Morning Call For June 10, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.32%) this morning are up +0.36% on M&A activity as HCC Insurance Holdings jumped 33% in pre-market trading after Tokio Marine Holdings agreed to buy the company for about $7.5 billion. European stocks are up +0.85% as Greek Prime Minister Tsipras prepares to meet German Chancellor Merkel and French President Hollande in an attempt to strike a debt deal. The Greek 10-year bond yield fell 60 bp from a 6-week high of 12.21% down to 11.61% on optimism that Greece can reach a deal with its creditors. Asian stocks closed mixed: Japan -0.25%, Hong Kong -1.12%, China -0.15%, Taiwan +1.16%, Australia +0.13%, Singapore +0.93%, South Korea -0.55%, India +1.36%. Japan's Nikkei Stock Index dropped to a 3-week low as a rally in the yen to a 2-week high against the dollar undercut earnings prospects of Japanese exporters. Chinese stocks closed lower after MSCI held off from adding mainland Chinese equities to its benchmark indexes, saying it expects to include the stocks after it settles investor concerns about accessibility and stock ownership with the China Securities and Regulatory Commission.

Commodity prices are mostly higher with a weak dollar. Jul crude oil (CLN15 +2.28%) is up +2.16% at a 3-week high on expectations for U.S. crude supplies to drop after data late Tuesday from API showed crude stockpiles fell by -6.7 million bbl in the week of Jun 5. Jul gasoline (RBN15 +1.77%) is up +1.90% at a 7-month high. Metals prices are stronger. Aug gold (GCQ15 +0.71%) is up +0.63%. Jul copper (HGN15 +1.40%) is up +1.60% at a 1-week high on signs of tighter supplies after LME copper inventories fell -2,800 MT to 308,025 MT, a 3-month low. Agricultural prices are mixed ahead of today's USDA Jun WASDE crop production report.

The dollar index (DXY00 -0.29%) is down -0.27% at a 3-week low. EUR/USD (^EURUSD) is down -0.10%. USD/JPY (^USDJPY) is down -0.92% at a 2-week low after BOJ Governor Kuroda said "the yen is unlikely to weaken further."

Sep T-note prices (ZNU15 -0.40%) are down -18.5 ticks at an 8-month low on carryover weakness from a plunge in German bund prices to an 8-1/2 month low.

USD/JPY fell to a 2-week low on comments from BOJ Governor Kuroda who told the Japanese Parliament that "the yen is unlikely to weaken further in real effective terms if you think with common sense, given how far it has come." He added that "excessive yen gains have been corrected," and it can't' be assumed that the yen will drop when the Federal Reserve raises interest rates.

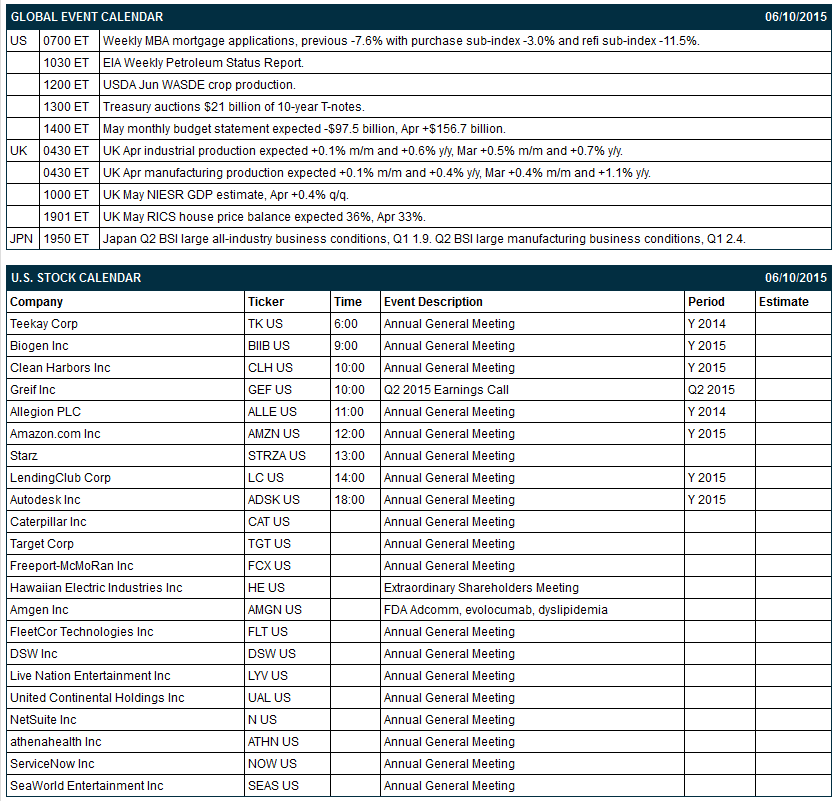

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (last -7.6% with purchase sub-index -3.0% and refi sub-index -11.5%), (2) May monthly budget statement (expected -$97.5 billion after April's +$156.7 billion), and (3) the Treasury's auction of $21 billion of 10-year T-notes.

None of the Russell 1000 companies report earnings today.

U.S. IPO's scheduled to price today include: Axovant Sciences (AXON), CyberArk Software (CYBR), Gulfport Energy (GPOR), Nord Anglia Education (NORD).

Equity conferences during the remainder of this week include: Apple's Worldwide Developer's Conference (WWDC15) on Mon-Fri, Morgan Stanley Financials Conference on Tue-Wed, NAREIT REITWeek Investor Forum on Tue-Wed, Piper Jaffray Consumer Conference on Tue-Wed, Piper Jaffray Consumer Conference on Tue-Wed, Goldman Sachs Global Healthcare Conference on Tue-Thu, Deutsche Bank db Access Global Consumer Conference on Tue-Thu, William Blair Growth Stock Conference on Tue-Thu, Goldman Sachs European Payments Conference on Wed, Macquarie Group Ltd. Global Metals, Mining & Materials Conference on Wed, Gabelli & Co., Inc. Movie & Entertainment Conference on Thu, Goldman Sachs 2020 Vision Chemicals Conference on Thu, Susquehanna Energy and Industrials Conference on Thu, Barclays High Yield Bond and Syndicated Loan Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Dollar General (DG +0.77%) and NetApp (NTAP -0.18%) were both upgraded to 'Outperform' from 'Sector Perform' at RBC Capital.

NVIDIA (NVDA +0.51%) was downgraded to 'Neutral' from 'Buy' at Nomura.

H&R Block (HRB +2.27%) was downgraded to 'Neutral' from 'Outperform' at Credit Suisse.

Legg Mason (LM -0.54%) was downgraded to 'Negative' from 'Neutral' at Susquehanna.

Eaton Vance (EV -2.27%) was upgraded to 'Neutral' from 'Negative' at Susquehanna.

Community Health (CYH +2.08%) was initiated with an 'Outperform' at Wedbush with a price target of $65.

AOL (AOL -0.14%) was downgraded to 'Hold' from 'Buy' at Jefferies.

Colgate-Palmolive (CL +1.06%) was upgraded to 'Hold' from 'Sell' at Societe Generale.

Qorvo (QRVO -0.24%) will replace Lorillard (LO +0.41%) in the S&P 500 as of the close of trading on Jun 11.

Bloomberg reported that a U.S. judge told Trinity Industries (TRN -2.70%) , the maker of a guardrail safety system linked to numerous fatalities, to pay $663 million for defrauding the U.S. government.

GameStop (GME -0.35%) reported a 21.4% stake in Geeknet (GKNT -0.15%) .

Prudential (PRU +0.45%) authorized a $1 billion stock repurchase program.

Gulfport Energy (GPOR +0.62%) filed to sell 10 million shares of common stock.

Mattress Firm (MFRM +2.37%) dropped over 4% in after-hours trading after it reported Q1 adjusted EPS of 33 cents, weaker than consensus of 39 cents.

MARKET COMMENTS

June E-mini S&Ps (ESM15 +0.32%) this morning are up +7.50 points (+0.36%). Tuesday closes: S&P 500 +0.04%, Dow Jones -0.01%, Nasdaq -0.09%. The S&P 500 on Tuesday rebounded from a 1-month low and closed slightly higher on the strong April JOLTS job openings report of +267,000 to a record high of 5.376 million that put the labor market in a stronger light, although that may also accelerate a Fed rate hike. Energy producers rallied as the price of crude jumped $2 a barrel. Tech stocks were undercut as Apple fell to a 4-week low and Micron slumped to a 13-month low.

Sep 10-year T-notes (ZNU15 -0.40%) this morning are down -18.5 ticks at an 8-month low. Tuesday closes: TYU5 -7.50, FVU5 -4.00. Sep T-notes on Tuesday closed lower on the larger-than-expected increase in Apr JOLTS job openings, which could prompt an accelerated Fed rate hike, and on supply pressure as the Treasury auctions $58 billion of T-notes and T-bonds this week.

The dollar index (DXY00 -0.29%) this morning is down -0.258 (-0.27%) at a 3-week low. EUR/USD (^EURUSD) is down -0.0011 (-0.10%). USD/JPY (^USDJPY) is down -1.14 (-0.92%) at a 2-week low. Tuesday closes: Dollar Index -1.007 (-1.05%), EUR/USD -0.0009 (-0.08%), USD/JPY -0.139 (-0.11%). The dollar index on Tuesday closed sharply lower on technical selling and shook off the stronger-than-expected JOLTS report, which could accelerate a Fed rate hike.

July WTI crude oil (CLN15 +2.28%) this morning is up +$1.30 a barrel (+2.16%) at a 3-week high. July gasoline (RBN15 +1.77%) is up +0.0394 (+1.90%) at a 7-month high. Tuesday closes: CLN5 +2.00 (+3.44%), RBN5 +0.0867 (+4.32%). July crude and gasoline on Tuesday closed sharply higher with Jul gasoline at a 2-week high on expectations that Wednesday’s EIA data will show crude inventories fell -1.5 million bbl, the sixth straight decline.

Click on picture to enlarge

Disclosure: None.