Morning Call For July 28, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.10%) this morning are trading slightly higher by +0.12% on support from a +5% overnight rally in Facebook on better-than-expected revenue and user figures. The Euro Stoxx 50 index this morning is down by -0.67%, undercut by the banking sector after Lloyds Banking Group fell -4% on a disappointing earnings outlook tied in part to Brexit. The European banking sector is also lower ahead of bank stress-test results that will be released on Friday.

On the more positive side, European stocks are getting some underlying support this morning from news that the July Eurozone economic confidence index from the European Commission rose by +0.2 points to 104.6 from 104.4 in June, which was substantially stronger than market expectations for a -0.9 point decline to 103.5. The confidence report suggested that Europe largely shook off concerns about the July 23 Brexit vote. The July German unemployment rate was unchanged at a record low of 6.1%. The Spanish Q2 unemployment rate fell to a 6-year low of 20%.

The Nikkei index today closed -1.12% on yen strength with USD/JPY down -0.67 yen (-0.64%) this morning. The Japanese markets are worried about whether the BOJ on Friday will announce a sufficiently large expansion of new monetary stimulus measures to meet high market expectations. Prime Minister Abe on Wednesday announced a $265 billion fiscal stimulus plan to put pressure on the BOJ for the maximum amount of new monetary stimulus.

The rest of the Asian markets today closed mixed with support from Wednesday's FOMC results that reduced concerns for a rate hike as early as the next FOMC meeting in September: Hong Kong -0.20%, China Shanghai +0.08%, Taiwan +0.15%, Australia +0.30%, Singapore -0.78%, South Korea -0.34%, India +0.66%, Turkey +0.66%.

Sep 10-year T-notes (ZNU16 +0.01%) are up +1.5 ticks this morning as the market looks ahead to today's 7-year T-note auction. There are questions about Treasury demand at current yields after the weak demand seen at Tuesday's 5-year T-note auction.

The dollar index (DXY00 -0.46%) is down -0.52 points (-0.53%) this morning as the dollar continues to slide on the market's dovish interpretation of Wednesday's FOMC post-meeting statement. The dollar is also lower on yen strength as USD/JPY (^USDJPY) fell -0.67 (-0.64%) on fears that the BOJ will disappoint on Friday. EUR/USD (^EURUSD) this morning is up +0.30 (+0.27%).

Commodity prices are up +0.42% this morning with support in part from today's -0.53% sell-off in the dollar index. Sep crude oil (CLU16 +0.24%) this morning is slightly lower by -0.05 (-0.12%) on continued overhang from yesterday's weekly EIA that showed an unexpected +1.7 million bbl increase in U.S. crude oil inventories and the third straight week of U.S. oil production gains. Sep gasoline (RBU16 +0.61%) this morning is up +0.0016 (+0.12%). Metals prices are trading sharply higher on the weak dollar with Aug gold (GCQ16 +1.07%) up +13.1 (+0.99%), Sep silver (SIU16 +2.13%) up +0.415 (+2.08%), and Sep copper (HGU16 +1.01%) up +0.016 (+0.73%). Grains are trading higher with Dec corn up +1.00 (+0.29%), Nov soybeans up +2.00 (+0.20%), and Sep wheat up +3.50 (+0.84%). Softs are mixed with Oct sugar down -0.04 (-0.21%), Sep coffee up +0.25 (+0.18%), Sep cocoa up +23 (+0.81%), and Dec cotton down -1.29 (-1.75%).

U.S. STOCK PREVIEW

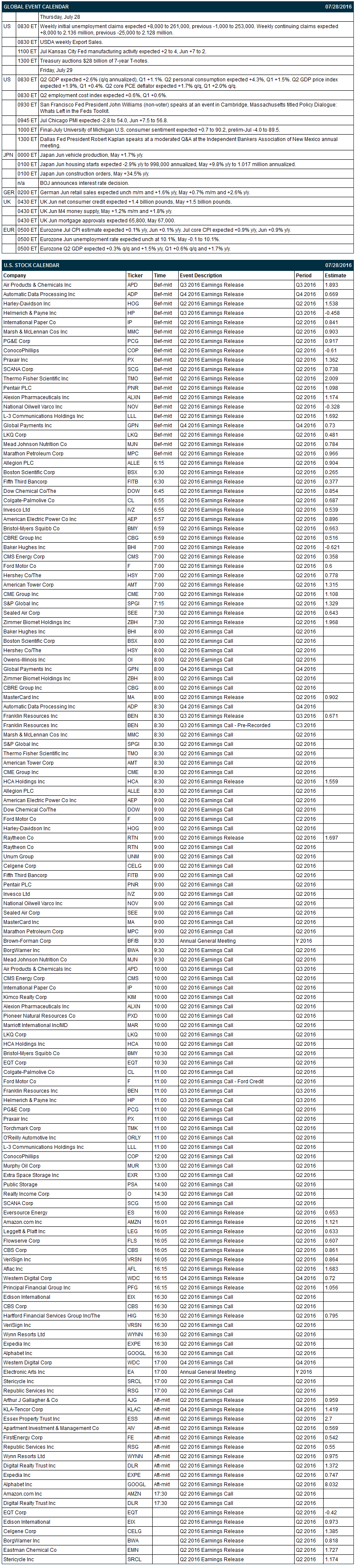

Key U.S. news today includes: (1) weekly initial unemployment claims (expected +8,000 to 261,000, previous -1,000 to 253,000) and continuing claims (expected +8,000 to 2.136 million, previous -25,000 to 2.128 million), (2) Jul Kansas City Fed manufacturing activity (expected +2 to 4, Jun +7 to 2), (3) Treasury auction of $28 billion of 7-year T-notes, and (4) USDA weekly Export Sales.

There are 67 of the S&P 500 companies that report earnings today with notable reports including: Amazon.com (consensus $1.12), Alphabet (8.03), MasterCard (0.90), Ford (0.60), Harley-Davidson (1.54), PG&E (0.92), Marathon Petroleum (0.97), Dow Chemical (0.85), Baker Hughes (-0.62), CME Group (1.11).

U.S. IPO's scheduled to price today: Bioventus Inc (BIOV), Talend SA (TLND).

Equity conferences this week include: none.

Sep E-mini S&Ps this morning are trading slightly higher by +0.12% on support from a +5% overnight rally in Facebook on better-than-expected revenue and user figures. Wednesday's closes: S&P 500 -0.12%, Dow Jones -0.01%, Nasdaq +0.58%. The S&P 500 on Wednesday closed slightly lower. Stocks were undercut by the weaker-than-expected June durable goods orders report of -4.0% and -0.5% ex-transportation (vs market expectations of -1.4% and +0.3%) and by the weaker-than-expected U.S. June pending home sales report of +0.2% m/m (vs expectations of +1.2%). There was also weakness in petroleum companies as Sep crude oil fell by another -2.3% to a new 3-month low. However, stocks saw underlying support from the FOMC's post-meeting statement that did not suggest that the FOMC is on the verge of a rate hike at its next meeting in September. U.S. stocks also got a boost from the early announcement of Japan's new $265 billion fiscal stimulus package.

OVERNIGHT U.S. STOCK MOVERS

- Facebook (FB +1.75%) rallied 5% overnight after revenue and user figures topped estimates on a surge in mobile ads.

- Groupon (GRPN -3.32%) rallied 24% in after-hours trading on higher sales guidance for the remainder of the year.

- Cirrus Logic (CRUS +2.50%) rallied 14% in after-hours trading after strong revenue guidance and EPS and sales figures that beat the consensus (Q1 EPS of 44 cents vs 27 cent consensus).

- Whole Foods (WFM -1.38%) fell 4% in after-hours trading after missing sales estimates on tougher competition.

- Vertex Pharmaceuticals (VRTX +1.08%) fell -2.5% in after-hours trading after reporting disappointing sales for its Orkambi therapy.

- Barrick Gold (ABX +4.40%) fell -2.6% in after-hours trading after releasing its quarterly earnings report.

- Earnings reports this morning have been nearly all positive with results including: Fifth Third (FITB -0.05%)(0.41 vs 0.38 consensus), Marathon Petroleum (MPC -2.02%)(1.62 vs 0.97), Dow Chemical (DOW +0.17%)(0.95 vs 0.85), Colgate-Palmolive (CL -0.95%)(0.70 vs 0.60), Raytheon (RTN -0.04%)(2.38 vs 2.02), Bristol-Myers (BMY +1.88%)(0.69 vs 0.66), CME Group (CME +1.20%) (1.14 vs 1.11),

MARKET COMMENTS

Sep 10-year T-notes are up +1.5 ticks this morning as the market looks ahead to today's 7-year T-note auction. Wednesday's closes: TYU6 +13.5, FVU6 +8.5. Sep 10-year T-notes on Wednesday rallied moderately on the weaker-than-expected U.S. durable goods and pending home sales reports and on relief that the FOMC did not adopt more hawkish language suggesting a rate hike in September. T-notes were also boosted by the -2.3% sell-off in Sep crude oil that further dampened inflation expectations.

The dollar index is down -0.52 points (-0.53%) this morning as the dollar continues to slide on the market's dovish interpretation of Wednesday's FOMC post-meeting statement. The dollar is also lower on yen strength as USD/JPY fell -0.67 (-0.64%) on fears that the BOJ will disappoint on Friday. EUR/USD this morning is up +0.30 (+0.27%). Wednesday's closes: Dollar index -0.10 (-0.11%), EUR/USD +0.0072 (+0.66%), USD/JPY +0.74 (+0.71%). The dollar index on Wednesday closed mildly lower on the market's dovish interpretation of the FOMC's post-meeting statement. USD/JPY rallied on Japanese Prime Minister Abe's earlier-than-expected announcement of a $265 billion fiscal stimulus package, which will put pressure on the BOJ for new stimulus measures at its Thu-Friday meeting.

Sep crude oil this morning is slightly lower by -0.05 (-0.12%) on continued overhang from yesterday's weekly EIA that showed an unexpected +1.7 million bbl increase in U.S. crude oil inventories and the third straight week of U.S. oil production gains. Sep gasoline this morning is up +0.0016 (+0.12%). Wednesday's closes: CLU6 -1.00 (-2.33%), RBU6 -0.0264 (-1.96%). Sep crude oil and gasoline on Wednesday closed lower with Sep crude oil posting a new 3-month low on the EIA report showing a +1.67 million bbl rise in U.S. crude oil inventories (vs expectations of -2.5 million bbls). Crude oil prices were also undercut by the +0.2% increase in U.S. oil production to 8.515 million bpd, the third straight weekly gain that now totals +1.0%.

(Click on image to enlarge)

Disclosure: None.