Morning Call For January 8, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.99%) this morning are up +0.87% on positive carryover from Wednesday afternoon's Dec 16-17 FOMC meeting minutes that signaled the Fed will remain patient in raising interest rates. European stocks are up +2.12% as signs of economic weakness in Europe spurs optimism that the ECB will expand stimulus. Eurozone producer prices in Nov fell more than expected while German Nov factory orders declined more than forecast. Greece's ASE Stock Index fell over 1% today to a 2-year low as polls show the anti-austerity party Syriza is leading ahead of Greece's Jan 25 elections. As expected, the BOE today left its benchmark interest rate unchanged at 0.50% and maintained its asset purchase target at 375 billion pounds. Asian stocks closed mostly higher: Japan +1.67%, Hong Kong +0.65%, China -2.32%, Taiwan +1.74%, Australia +0.52%, Singapore +1.42%, South Korea +1.42%, India +1.36%. Chinese stocks bucked the trend and closed lower as China's Shanghai Index tumbled over 2% after analysts from Bank of America and HSBC Holdings Plc forecast declines this year for Chinese stocks. Commodity prices are mixed. Feb crude oil (CLG15 +0.39%) is up +0.78%. Feb gasoline (RBG15 +0.16%) is up +0.20%. Feb gold (GCG15 -0.40%) is down -0.35%. Mar copper (HGH15 +0.65%) is up +0.24%. Agriculture prices are mixed. The dollar index (DXY00 +0.64%) is up +0.58% at a 9-year high. EUR/USD (^EURUSD) is down -0.60% at a 9-year low on expectations for the ECB to begin large-scale government bond purchases when it meets on Jan 22. USD/JPY (^USDJPY) is up +0.47%. Mar T-note prices (ZNH15 -0.30%) are down -10.5 ticks.

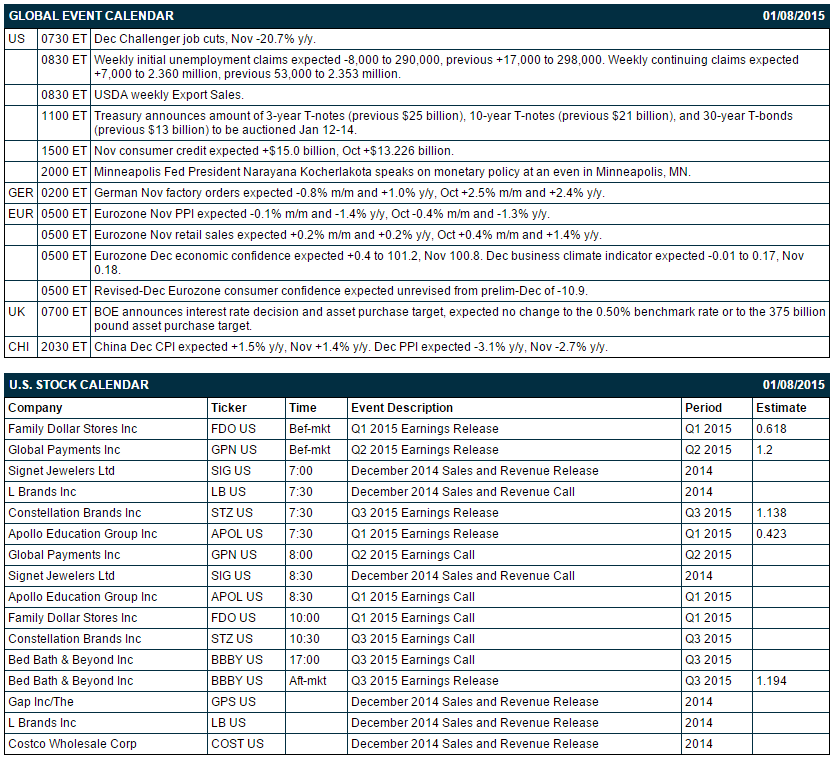

Eurozone Nov retail sales rose +0.6% m/m and +1.5% y/y, much better than expectations of +0.2% m/m and +0.2% y/y.

Eurozone Nov PPI fell -0.3% m/m and -1.6% y/y, more than expectations of -0.1% m/m and -1.4% y/y with the -1.6% y/y drop the fastest pace of decline in 8 months.

The Eurozone Dec business climate indicator fell -0.13 to 0.04, a bigger decline than expectations of -0.01 to 0.17. Dec economic confidence was unchanged at 100.07, weaker than expectations of +0.04 to 101.2.

German Nov factory orders fell -2.4% m/m, three times more than expectations of -0.8% m/m. On an annual basis Nov factory orders unexpectedly fell-0.4% y/y, weaker than expectations of +1.0% y/y.

UK Dec Halifax house prices rose +0.9% m/m and +7.8% 3-mo/year-over-year, better than expectations of +0.3% m/m and +7.6% 3-mo/year=over-year.

Speaking Wednesday night at an event in Chicago, Chicago Fed President Evans said "I don't think we should be in a hurry to raise interest rates" as inflation may stay under the Fed's 2.0% target for 3 to 4 years and a move to tighten too soon would be a "catastrophe."

U.S. STOCK PREVIEW

Today’s weekly initial unemployment claims report is expected to show a -8,000 decline to 290,000, reversing about one-half of last week’s rise of +17,000 to 298,000. Today’s Nov consumer credit report is expected to show another strong increase of +$15.0 billion, up from October’s +$13.226 billion but mildly below the year-to-date monthly average of +$18.1 billion. There are 5 the Russell 1000 companies that report earnings today: Family Dollar Stores (consensus $0.62), Global Payments (1.20), Constellation Brands (1.14), Apollo Education (0.42), Bed Bath & Beyond (1.19). Equity equity conferences during the remainder of this week include: Goldman Sachs Global Energy Conference on Wed-Thu, and Evercore ISI Utility Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Advance Auto Parts (AAP +2.15%) and Tractor Supply (TSCO +3.24%) were both upgraded to 'Buy' from 'Hold' at Deutsche Bank.

Global Payments (GPN +1.17%) reported Q2 cash EPS of $1.27, better than consensus of $1.20, and then raised guidance on fiscal 2015 cash EPS view to $4.75-$4.83 from $4.65-$4.75, higher than consensus of $4.73.

Ralph Lauren (RL +2.51%) was downgraded to 'Hold' from 'Buy' at Maxim.

Staples (SPLS +2.02%) was added to the short-term buy list at Deutsche Bank.

Eli Lilly (LLY -0.70%) wsa downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Priceline (PCLN -0.96%) was downgraded to 'Hold' from 'Buy' at Stifel.

Constellation Brands (STZ +2.58%) reported Q3 EPS of $1.10, less than consensus of $1.14.

Family Dollar Stores (FDO +0.24%) reported Q1 EPS of 44 cents, well below consensus of 62 cents.

Bank of America (BAC +0.47%) was initiated with an 'Outperform' at Credit Suisse with a price target of $21.

Marathon Oil (MRO +1.23%) and Oasis Petroleum (OAS unch) were both downgraded to 'Sell' from 'Neutral' at Citigroup.

Anadarko (APC +1.59%) , Chesapeake (CHK -0.33%) , Whiting Petroleum (WLL -0.10%) , Pioneer Natural (PXD -1.10%) , Noble Energy (NBL -0.38%) and Cabot Oil & Gas (COG +0.86%) wwre all downgraded to 'Neutral' from 'Buy' at Citigroup.

Goldman Sachs (GS +1.49%) was initiated with an 'Outperform' at Credit Suisse with a price target of $225.

JPMorgan Chase (JPM +0.15%) was initiated with an 'Outperform' at Credit Suisse with a price target of $75.

Zumiez (ZUMZ +4.73%) rose 3% in after-hours trading after it reported December same-store-sales were up 8% y/y and then raised guidance on Q4 EPS to 75 cents-77 cents from 69 cents-72 cents, higher than consensus of 73 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +0.99%) this morning are up +17.50 points (+0.87%). The S&P 500 index on Wednesday closed higher: S&P 500 +1.16%, Dow Jones +1.23%, Nasdaq +1.20%. Bullish factors included (1) signs of strength in the U.S. labor market after the Dec ADP employment change rose +241,000, better than expectations of +225,000, and (2) the Dec 16-17 FOMC meeting minutes that stated the economy was expanding at a moderate pace with broad-based improvement in the job market.

Mar 10-year T-notes (ZNH15 -0.30%) this morning are down -10.5 ticks. Mar 10-year T-note futures prices on Wed closed slightly higher. Closes: TYH5 +3.50, FVH5 +3.25. T-notes traded weaker until early-afternoon when they erased their losses and closed higher after the Dec 16-17 FOMC meeting minutes stated that policy members saw an interest rate hike “unlikely” before the Apr FOMC meeting. Prices had traded lower on negative factors included (1) the larger-than-expected increase in the Dec ADP employment report, and (2) a rally in stocks that curbed the safe-haven demand for Treasuries.

The dollar index (DXY00 +0.64%) this morning is up +0.532 (+0.58%) at a new 9-year high. EUR/USD (^EURUSD) is down -0.0071 (-0.60%) at a fresh 9-year low. USD/JPY (^USDJPY) is up +0.56 (+0.47%). The dollar index on Wednesday rose to a 9-year high and closed higher: Dollar index +0.391 (+0.43%), EUR/USD -0.00506 (-0.43%), USD/JPY +0.867 (+0.73%). Bullish factors included (1) the plunge in EUR/USD to a 9-year low after Eurozone CPI fell to a 5-1/4 year low of -0.2%, y/y, which bolstered expectations for the ECB to begin QE when it meets on Jan 22, and (2) the larger-than expected increase in the Dec ADP employment report, which signals labor market strength and puts the Fed closer to raising interest rates.

Feb WTI crude oil (CLG15 +0.39%) this morning is up +38 cents (+0.78%) and Feb gasoline (RBG15 +0.16%) is up +0.0027 (+0.20%). Feb crude oil and Feb gasoline on Wednesday posted 5-3/4 year lows but settled mixed: CLG5 +0.72 (+1.50%), RBG5 -0.0155 (-1.14%). Bearish factors included (1) the rally in the dollar, (2) the +8.1 million bbl surge in weekly EIA gasoline inventories to a 3-3/4 year high of 237.2 million bbl, and (3) the +1.3 million bbl build in crude supplies at Cushing, OK, delivery point of WTI futures, to a 10-month high of 32.1 million bbl. Crude prices closed higher after weekly EIA crude stockpiles unexpectedly fell -3.06 million bbl.

Disclosure: None.