Morning Call For January 30, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.69%) this morning are down -0.63% and European stocks are down -0.10% on Eurozone deflation concerns after Jan Eurozone consumer prices fell a more-than-expected -0.6% y/y and matched the largest decline since the euro currency was introduced in 1999. Losses in European stocks were limited after the Eurozone Dec unemployment rate unexpectedly declined to the lowest in 28 months. The Russian ruble tumbled to a 1-1/2 month low against the dollar after Russia's central bank cut the 1-week auction rate to 15% from 17%. Credit-default swaps on Russia's government debt rose 3 bp to 617 bp, the highest since March 2009. Asian stocks closed mixed: Japan +0.39%, Hong Kong -0.36%, China -1.36%, Taiwan -0.69%, Australia +0.34%, Singapore -0.81%, South Korea -0.23%, India -1.68%. China's Shanghai Stock Index fell to a 1-1/2 week low as government regulators begin efforts to cool the growth of margin trading. Commodity prices are mostly higher. Mar crude oil (CLH15 +0.97%) is up +1.32%. Mar gasoline (RBH15 +0.34%) is up +0.30%. Feb gold (GCG15 +0.66%) is up +0.71%. Mar copper (HGH15 +1.16%) is up +1.04%. Agriculture prices are higher. The dollar index (DXY00 -0.26%) is down -0.35%. EUR/USD (^EURUSD) is up +0.23%. USD/JPY (^USDJPY) is down -0.52%. Mar T-note prices (ZNH15 +0.23%) are up +9.5 ticks.

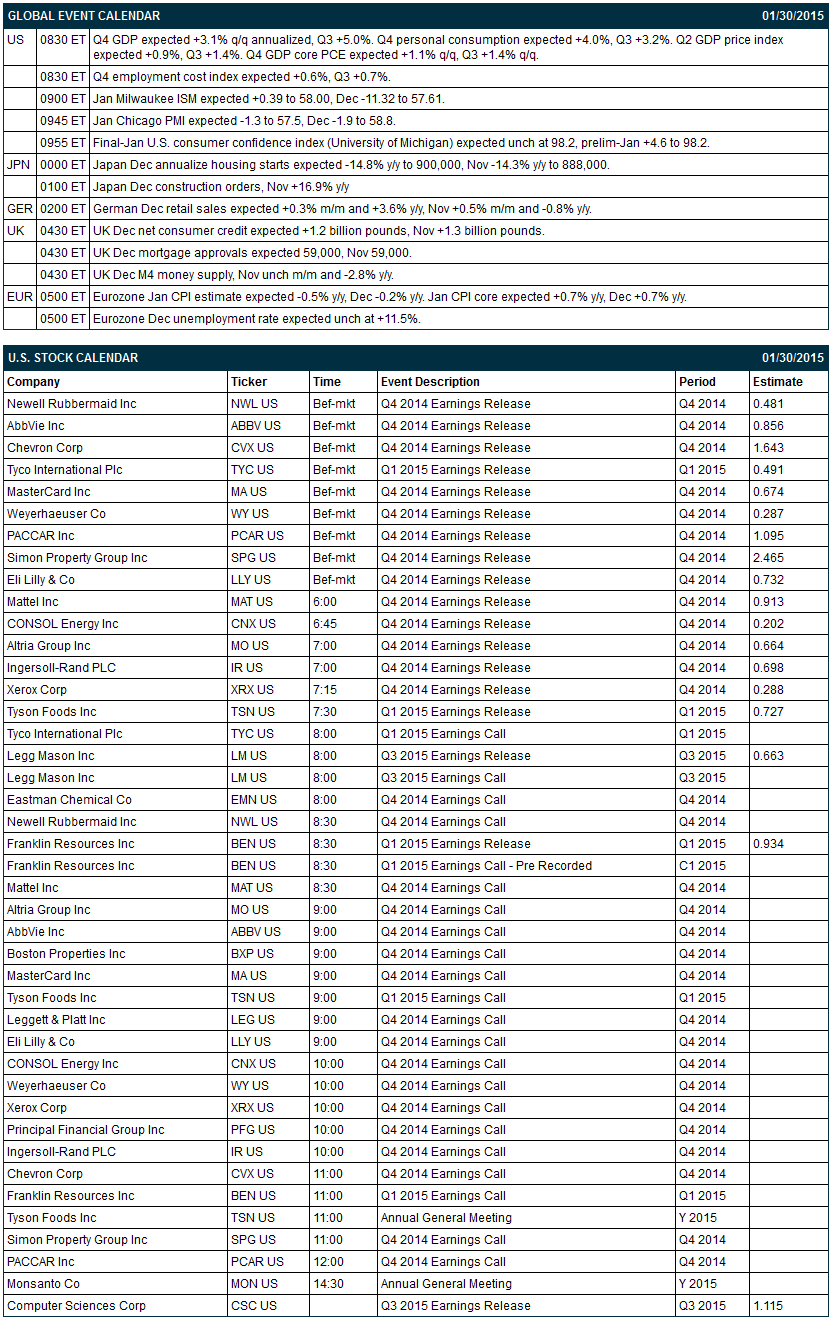

The Eurozone Jan CPI estimate fell -0.6% y/y, a bigger decline than expectations of -0.5% y/y and matched the July 2009 decrease as the biggest drop since the euro currency was introduced in 1999. The Jan core CPI rose +0.6% y/y, less than expectations of +0.7% y/y and the slowest pace of increase since the data series began in 1997.

The Eurozone Dec unemployment rate unexpectedly fell -0.1 to 11.4%, better than expectations of unch at 11.5% and the lowest in 28 months.

German Dec retail sales rose +0.2% m/m, less than expectations of +0.3% m/m, but on an annual basis rose +4.0% y/y, more than expectations of +3.6% y/y and the largest annual increase in 2-1/2 years.

UK Dec net consumer credit rose +0.6 billion pounds, less than expectations of +1.2 billion pounds and the slowest pace of increase in 13 months.

UK Dec mortgage approvals rose 60,300, more than expectations of 59,000.

The Japan Dec jobless rate unexpectedly fell -0.1 to 3.4%, better than expectations of unch at 3.5% and the lowest in 17-1/2 years. The Dec job-to-applicant ratio rose +0.03 to 1.15, better than expectations of unch at 1.12 and the highest in 22-3/4 years.

Japan Dec national CPI rose +2.4% y/y, unch from Nov and higher than expectations of -0.1 to 2.3% y/y. Dec national CPI ex-fresh food rose 2.5% y/y, down -0.2 from Nov and the slowest pace of increase in 9 months. Dec national CPI ex food & energy climbed +2.1% y/y, unch from Nov and right on expectations.

Japan Dec industrial production rose +1.0% m/m, less than expectations of +1.2% m/m, although year-over-year Dec industrial production rose +0.3% y/y, right on expectations.

U.S. STOCK PREVIEW

Today’s Q4 GDP report is expected to ease to +3.1% (q/q annualized) from +5.0% in Q3. Today’s final-Jan U.S. consumer confidence index from the University of Michigan is expected to be unrevised from the early-Jan figure of 98.2, thus leaving the final-Jan figure of 98.2 up by +4.6 points from December’s level. Today’s Q4 employment cost index is expected to show an increase of +0.6% q/q, which would be slightly below the +0.7% increase seen in Q3. Today’s Jan Chicago PMI report is expected to show a -1.3 point decline to 57.5, adding to the -1.9 point decline to 58.8 seen in Dec.

There are 18 of the S&P 500 companies that report earnings today with notable reports including: MasterCard (consensus $0.67), Chevron (1.64), Tyson Foods (0.73), AbbVie (0.86), Weyerhaeuser (0.29), Eli Lilly (0.73), Ingersoll-Rand (0.70). There are no equity conferences today.

OVERNIGHT U.S. STOCK MOVERS

Weyerhaeuser (WY -0.45%) reported Q4 EPS of 27 cents, below consensus of 29 cents.

Mattel (MAT -0.33%) reported Q4 EPS of 52 cents, well below consensus of 91 cents.

Eli Lilli (LLY +1.61%) reported Q4 EPS of 75 cents, better than consensus of 73 cents.

Eastman Chemical (EMN -0.01%) reported Q4 adjusted EPS of $1.64, higher than consensus of $1.52.

Unisys (UIS -1.21%) reported Q4 EPS of $1.60, well above consensus of $1.27.

Leggett & Platt (LEG +1.30%) reported Q4 adjusted EPS of 41 cents, less than consensus of 45 cents, and then lowered guidance on fiscal 2015 EPS to $1.90-$2.10, below consensus of $2.10.

Acuity Brands (AYI +0.16%) coverage resumed with a 'Buy' at Stifel witha price target of $185.

C.R. Bard (BCR +1.02%) reported Q4 adjusted EPS of $2.29, higher than consensus of $2.24.

JDSU (JDSU -2.43%) fell 5% in after-hours trading after it reported Q2 EPS of 15 cents, below consensus of 16 cents.

Hanesbrands (HBI +1.44%) reported Q4 adjusted EPS of $1.46, more than consensus of $1.43.

Biogen (BIIB +0.59%) reported Q4 EPS of $4.09, above consensus of $3.78, and then raised guidance on fiscal 2015 EPS to $16.60-$17.00, better than consensus of $16.37.

Broadcom (BRCM +0.83%) rose 3% in after-hours trading after it reported Q4 adjusted EPS ex-SBC of 90 cents, higher than consensus of 87 cents.

Visa (V +0.67%) climbed over 3% in after-hours trading after it reported Q1 EPS of $2.53, better than consensus of $2.49, and then announced a four-for-one stock split.

Principal Financial (PFG +0.29%) reported Q4 EPS of $1.09, higher than consensus of $1.04.

Manitowoc (MTW +0.89%) reported Q4 adjusted EPS of 27 cents, below consensus of 32 cents.

Google (GOOG +0.13%) reported Q4 EPS of $6.88, weaker than consensus of $7.11.

Amazon.com (AMZN +2.59%) jumped 11% in after-hours trading after it reported Q4 EPS of 45 cents, well above consensus of 17 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.69%) this morning are down -12.75 points (-0.63%). The S&P 500 index on Thursday rebounded from a 1-1/2 week low and closed higher: S&P 500 -1.35%, Dow Jones -1.13%, Nasdaq -0.60%. Bullish factors included (1) the -43,000 decline in U.S. weekly initial unemployment claims to 265,000, more than expectations of -7,000 to 300,000 and the lowest level in 14-3/4 years, and (2) strength in energy producers which recovered from early losses after crude oil rebounded from a 5-3/4 year low and closed higher. A bearish factor was the unexpected -3.7% m/m decline in U.S. Dec pending home sales, weaker than expectations of a +0.5% m/m increase and the biggest decline in a year.

Mar 10-year T-notes (ZNH15 +0.23%) this morning are up +9.5 ticks. Mar 10-year T-note futures prices on Thursday closed lower. Closes: TYH5 -9.00, FVH5 -4.75. Bearish factors included (1) the larger-than-expected decline in U.S. weekly jobless claims to the lowest level in 14-3/4 years, and (2) reduced safe-haven demand for T-notes after stocks rallied.

The dollar index (DXY00 -0.26%) this morning is down -0.328 (-0.35%). EUR/USD (^EURUSD) is up +0.0026 (+0.23%). USD/JPY (^USDJPY) is down -0.62 (-0.52%). The dollar index on Thursday closed higher: Dollar index +0.315 (+0.33%), EUR/USD +0.00324 (-0.29%), USD/JPY -0.3458 (-0.29%). Bullish factors included (1) the larger-than-expected fall in U.S. weekly jobless claims to the lowest level in 14-3/4 years, which signals labor market strength and bolsters speculation the Fed will soon raise interest rates, and (2) the increase in Eurozone Jan economic confidence to a 6-month high, which was supportive for EUR/USD.

Mar WTI crude oil (CLH15 +0.97%) this morning is up +59 cents (+1.32%) and Mar gasoline (RBH15 +0.34%) is up +0.0042 (+0.30%). Mar crude oil and Mar gasoline on Thursday recovered from early losses and closed higher: CLH5 +0.08 (+0.18%), RBH5 +0.0143 (+1.04%). Mar crude posted a 5-3/4 year low on carry-over weakness from Wednesday’s EIA report where U.S. crude inventories climbed to a record high 406.7 million bbl and U.S. crude production rose to 9.213 million bpd, the highest in over 40 years. However, fund short covering near the lows helped crude oil erase its losses and close higher.

Click on picture to enlarge

Disclosure: None.