Morning Call For Friday, Sept. 29

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 -0.05%) this morning are little changed, down -0.03%, ahead of U.S. economic data later this morning on Aug personal spending and income and the Aug core PCE deflator, the Fed's preferred gauge of inflation. European stocks are up +0.31% at a 3-month high on strength in the European economy after German unemployment in Sep unexpectedly fell to a record low. Also, inflation in the Eurozone rose at a slower-than-expected pace this month, which may prompt the ECB to delay tapering of its bond purchases. Asian stocks settled mixed: Japan -0.03%, Hong Kong +0.48%, China +0.28%, Taiwan _0.33%, Australia +0.20%, Singapore -0.22%, South Korea +0.77%, India unchanged. China's Shanghai Composite climbed to a 1-week high ahead of next week's Golden Week holidays, which will close the Chinese markets for the entire week. Japanese deflation concerns eased a bit after the Japan Aug national CPI rose a more than expected +0.7% y/y, the fastest pace of increase in 2-1/3 years.

The dollar index (DXY00 -0.02%) is down -0.03%. EUR/USD (^EURUSD) is up +0.24%. USD/JPY (^USDJPY) is up +0.10%.

Dec 10-year T-note prices (ZNZ17 -0.05%) are down -0.5 of a tick.

The German Sep unemployment change fell -23,000 to 2.506 million, stronger than expectations of -5,000. The Sep unemployment rate unexpectedly fell -0.1 to 5.6%, stronger than expectations of no change at 5.7% and the lowest since German reunification in 1990.

The Eurozone Sep CPI estimate rose +1.5% y/y, weaker than expectations of +1.6% y/y. The Sep core CPI rose +1.1% y/y, weaker than expectations of +1.2% y/y.

The Japan Aug jobless rate was unch at 2.8%, right on expectations. The Aug job-to-applicant ratio was unch at 1.52, weaker than expectations of +0.01 to 1.53.

Japan Aug national CPI rose +0.7% y/y, stronger than expectations of +0.6% y/y and the fastest pace of increase in 2-1/3 years. Aug national CPI ex fresh food rose +0.7% y/y, right on expectations. Aug national CPI ex fresh food & energy rose +0.2% y/y, right on expectations and the biggest increase in 7 months.

Japan Aug industrial production rose +2.1% m/m, stronger than expectations of +1.8% m/m.

U.S. STOCK PREVIEW

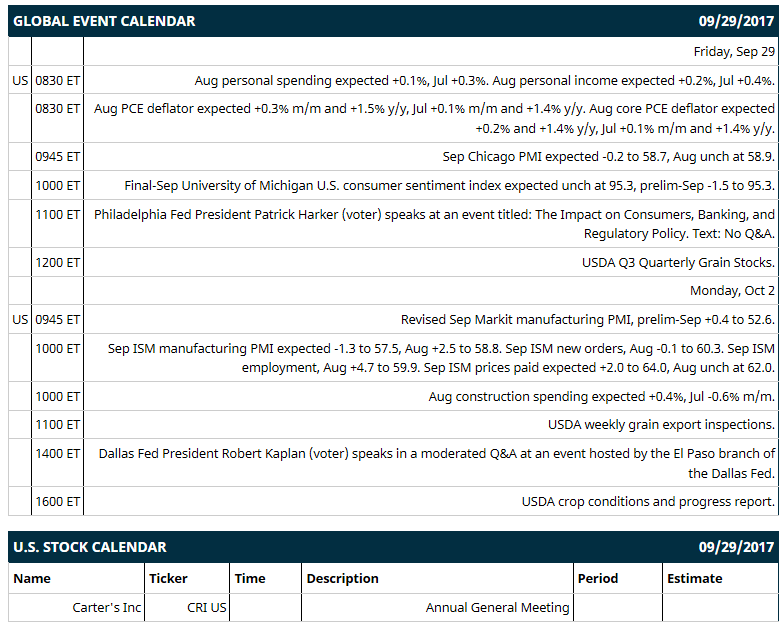

Key U.S. news today includes: (1) Aug personal spending (expected +0.1%, Jul +0.3%) and Aug personal income (expected +0.2%, Jul +0.4%), (2) Aug PCE deflator (expected +0.3% m/m and +1.5% y/y, Jul +0.1% m/m and +1.4% y/y) and Aug core PCE deflator (expected +0.2% and +1.4% y/y, Jul +0.1% m/m and +1.4% y/y), (3) Sep Chicago PMI (expected -0.2 to 58.7, Aug unch at 58.9), (4) final-Sep University of Michigan U.S. consumer sentiment index (expected unch at 95.3, prelim-Sep -1.5 to 95.3), (5) Philadelphia Fed President Patrick Harker (voter) speaks at an event titled: The Impact on Consumers, Banking, and Regulatory Policy, (6) USDA Q3 Quarterly Grain Stocks.

Notable Russell 1000 earnings reports today include: none.

U.S. IPO's scheduled to price today: none.

Equity conferences this week: none.

OVERNIGHT U.S. STOCK MOVERS

Louisiana-Pacific (LPX +0.07%) was downgraded to 'Underperform' from 'Market Perform' at BMO Capital Markets.

Altice (ATUS -3.05%) was initiated with a recommendation of 'Buy' at Redburn with a price target of $35.27.

Mastercard (MA +0.38%) was initiated with a recommendation of 'Overweight' at Cantor Fitzgerald with a 12-month target price of $165.

Vertex Pharmaceuticals (VRTX +0.37%) was initiated with a recommendation of 'Buy' at BTIG LLC with a 12-month target price of $200.

WR Grace (GRA) was initiated with a recommendation of 'Buy' at Loop Capital Markets with a 12-month target price of $81.

Tyson Foods (TSN) rallied over 5% in after-hours trading after it raised guidance on its fiscal 2017 adjusted EPS to $5.20-$5.30 from a prior view of $4.95-$5.05, citing better-than-expected earnings in the beef segment.

Cabot Microelectronics (CCMP) was initiated with a recommendation of 'Buy' at Loop Capital Markets with a 12-month target price of $94.

KB Home (KBH) gained over 1% in after-hours trading after it reported Q3 revenue of $1.14 billion, above consensus of $1.11 billion.

Nexstar Media Group (NXST +1.06%) slid 1% in after-hours trading after a block of 641,000 shares of Nexstar was offered at $61 a share via Raymond James, a -1.93% discount to Thursday's closing price.

Hilton Worldwide Holdings (HLT +0.36%) lost almost 1% in after-hours trading after it announced that it had commenced a secondary offering of 14.61 million shares of its common stock.

Smart Global Holdings (SGH +4.90%) jumped almost 7% in after-hours trading after it reported Q4 net sales of $223 million, better than consensus of $210.6 million.

Zynerba Pharmaceuticals (ZYNE +52.50%) rallied nearly 6% in after-hours trading after it was upgraded to 'Overweight' from 'Neutral' at Piper Jaffray with a target price of $16.

Marinus Pharmaceuticals (MRNS -4.77%) rose over 3% in after-hours trading after Bain Capital Life Sciences Fund reported a 15.9% passive stake in the company.

Aehr Test Systems (AEHR +11.04%) jumped olpx ver 15% in after-hours trading after it reported Q1 revenue of $6.97 million, better than expectations of $6.75 million.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 -0.05%) this morning are doen -0.75 points (-0.03%). Thursday's closes: S&P 500 +0.12%, Dow Jones +0.18%, Nasdaq -0.08%. The S&P 500 on Thursday closed higher on the unexpected upward revision to U.S. Q2 GDP to 3.1% from +3.0%, strongest pace of growth since Q1 2015, and on this week's increased optimism that Republicans may be able to cut corporate taxes. Energy stocks were undercut by the -1.11% sell-off in crude oil prices.

Dec 10-year T-note prices (ZNZ17 -0.05%) this morning are down -0.5 of a tick. Thursday's closes: TYZ7 +3.50, FVZ7 +3.25. Dec 10-year T-notes on Thursday recovered from a 2-1/2 month low and closed higher on some short-covering due to strong demand for the Treasury's $28 billion auction of 7-year T-notes that had a bid-to-cover ratio of 2.70, above the 12-auction average of 2.53. T-notes were undercut by the unexpected upward revision in U.S. Q2 GDP to 3.1% from 3.0% and by increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 4-1/2 month high.

The dollar index (DXY00 -0.02%) this morning is down -0.024 (-0.03%). EUR/USD (^EURUSD) is up +0.0028 (+0.24%) and USD/JPY (^USDJPY) is up +0.11 (+0.10%). Thursday's closes: Dollar Index -0.276 (-0.30), EUR/USD +0.0041 (+0.35%), USD/JPY -0.50 (-0.44%). The dollar index on Thursday closed lower on strength in EUR/USD after Eurozone Sep economic confidence rose +1.1 to 113.0, a 10-1/4 year high. The dollar was also undercut by the decline in T-note yields, which undercut the dollar's interest rate differentials.

Nov crude oil (CLX17 -0.12%) this morning is up +4 cents (+0.08%) and Nov gasoline (RBX17 -0.27%) is +0.0001 (+0.01%). Thursday's closes: Nov WTI crude -0.5 (-1.11%), Nov gasoline -0.0072 (-0.44%). Nov crude oil and gasoline on Thursday closed lower on the decline in the crack spread to a 1-month low, which may curb refinery demand for crude to refine into gasoline, and on negative carry-over from Wednesday's EIA data that showed U.S. crude production last week rose to a 2-year high.

Metals prices this morning are mixed with Dec gold (GCZ17 +0.16%) +3.3 (+0.26%), Dec silver (SIZ17 +0.11%) +0.043 (+0.26%) and Dec copper (HGZ17 -0.50%) -0.013 (-0.44%). Thursday's closes: Dec gold -13.9 (-1.07%), Dec silver -0.056 (-0.33%), Dec copper +0.0105 (+0.36%). Metals on Thursday closed higher on a weaker dollar, the upward revision to U.S. Q2 GDP to +3.1% from +3.0% that was positive for industrial metals demand, and the -3,525 MT decline in LME copper inventories to a 2-week low of 298,425 MT.

(Click on image to enlarge)

Disclosure: None.