Morning Call For Friday, October 27

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 +0.21%) this morning are up +0.25% and European stocks are up +0.63% at a 2-year high. U.S. stock index futures rose after the U.S. House passed a resolution that brings tax cuts a step closer. Also, technology stocks gained with Alphabet up 3% in pre-market trading and Amazon.com up 8% in pre-market trading after both companies reported stellar quarterly earnings results. European stocks gained on the slow approach by the ECB to reducing monetary stimulus along with the slump in EUR/USD to a 3-month low that gave European exporter stocks a boost. Asian stocks settled mostly higher: Japan +1.24%, Hong Kong +0.84%, China +0.27%, Taiwan -0.24%, Australia -0.22%, Singapore +0.90%, South Korea +0.69%, India +0.03%. China's Shanghai Composite climbed to a 1-1/4 year high on optimism in the Chinese economic outlook after China Sep industrial profits surged +27.7% y/y, the largest increase in 5-3/4 years. Japan's Nikkei Stock Index rallied to a 21-1/4 year high on strength in financial and telecommunication companies. Also. Japanese exporters surged as the yen fell to a 3-1/2 month low against the dollar, which boosted exporters' earnings prospects.

The dollar index (DXY00 +0.37%) is up +0.28% to a 3-1/4 month high after the U.S. House passed a budget resolution on tax reforms ad on speculation that President Trump will nominate a hawk as the next Fed Chair. EUR/USD (^EURUSD) is down -0.31% at a 3-month low after the ECB extended its QE program to at least Sep of 2018. USD/JPY (^USDJPY) is up +0.12% at a 3-1/2 month high as a rally in global equity markets reduces the safe-haven demand for the yen.

Dec 10-year T-note prices (ZNZ17 +0.01%) are up +1 tick.

As expected, the Bank of Russia cut its benchmark rate by -25 bp to 8.25% from 8.50%.

China Sep industrial profits jumped +27.7% y/y, the most in 5-3/4 years.

German Sep import prices rose +0.9% m/m and +3.0% y/y, stronger than expectations of +0.5% m/m and +2.6% y/y with the +0.9% m/m gain the largest monthly increase in 8 months.

U.S. STOCK PREVIEW

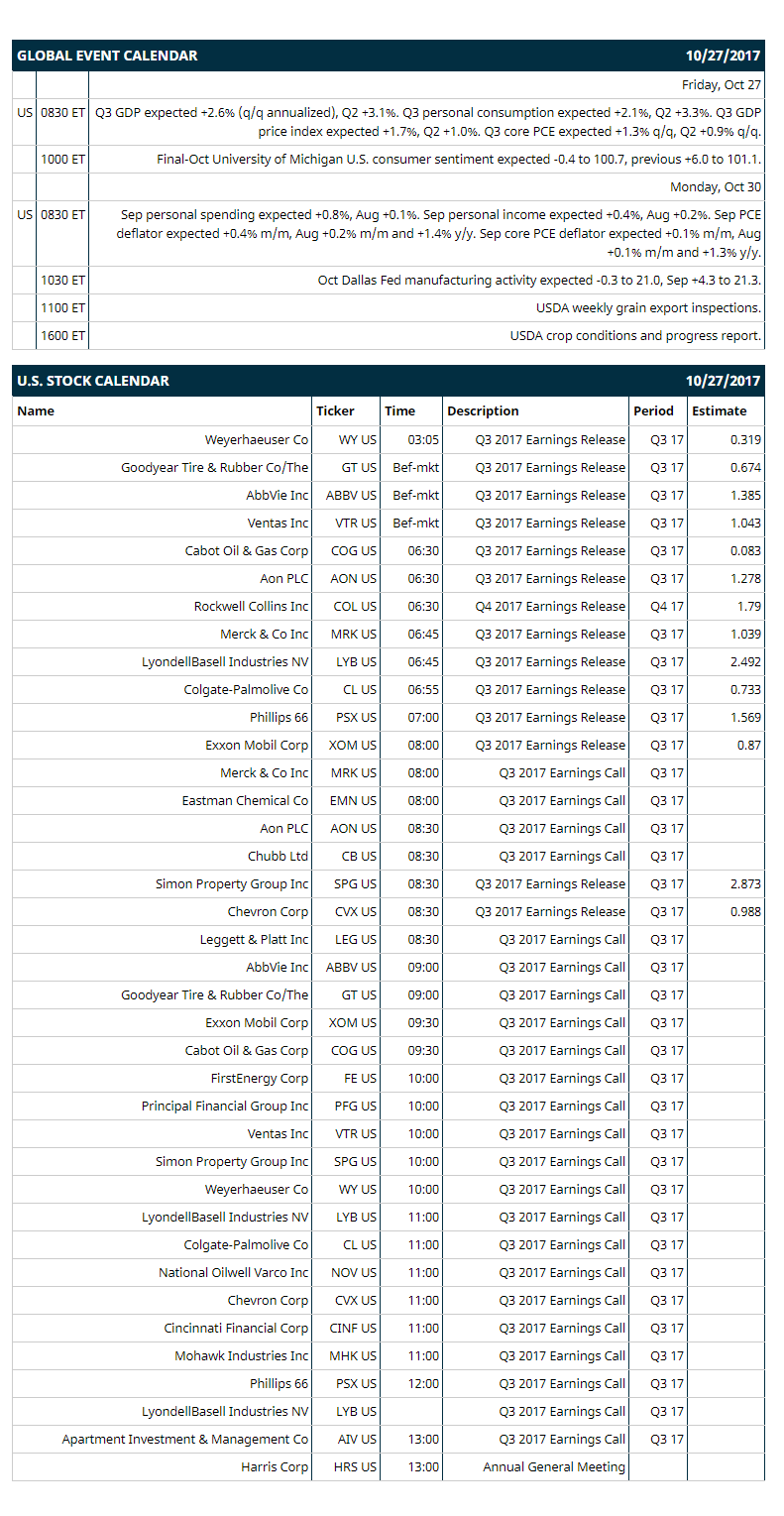

Key U.S. news today includes: (1) Q3 GDP (expected +2.6% q/q annualized, Q2 +3.1%), (2) final-Oct University of Michigan U.S. consumer sentiment (expected -0.4 to 100.7, previous +6.0 to 101.1).

Notable S&P 500 earnings reports today include: Exxon Mobil (consensus $0.87), Phillips 66 (1.57), Colgate-Palmolive (0.73), Merck (1.04), Cabot Oil & Gas (0.08), AbbVie (1.39), Goodyear (0.67), Weyerhaeuser (0.32).

U.S. IPO's scheduled to price today: none.

Equity conferences this week: Society of Women Engineers National Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Alphabet (GOOGL unch) climbed nearly 3% in pre-market trading after it reported Q3 EPS of $9.57, well above consensus of $8.34.

Amazon.com (AMZN -0.05%) jumped 8% in pre-market trading after it reported Q3 EPS of 52 cents, well above consensus of 4 cents.

First Solar (FSLR +1.12%) was upgraded to 'Buy' from 'Hold' at Needham & Co with a 12-month target price of $60.

Gilead Sciences (GILD -2.52%) slipped 3% in after-hours trading after it management said during a conference call that competition from AbbVie's hepatitis C drug Mavyret is undercutting Gilead and will have a bigger impact in Q4 and into next year.

Microsoft (MSFT +0.17%) rose almost 4% in after-hours trading after it reported Q1 EPS of 84 cents, better than consensus of 72 cents.

Intel (INTC +1.40%) gained over 1% in after-hours trading after it reported Q3 adjusted EPS of $1.01, higher than consensus of 80 cents.

Expedia (EXPE -0.37%) slumped 15% in after-hours trading after it reported Q3 adjusted EPS of $2.51, weaker than consensus of $2.62.

Stryker (SYK -0.91%) rose almost 3% in after-hours trading after it reported Q3 adjusted EPS of $1.52, above consensus of $1.49, and he said is seeing full-year adjusted EPS of $6.45 to $6.50, better than consensus of $6.43.

Align Technology (ALGN +0.61%) rallied 13% in after-hours trading after it reported Q3 net revenue of $385.3 million, higher than consensus of $359.8 million, and then said it sees Q4 net revenue of $391 million to $398 million, better than consensus of $368.2 million.

Electronics for Imaging (EFII -1.33%) sank 15% in after-hours trading after it reported Q3 adjusted EPS of 48 cents, below consensus of 58 cents.

Trimble (TRMB +0.02%) climbed 4% in after-hours trading after it reported Q3 revenue of $670 million, above consensus of $660.1 million, and said it sees Q4 revenue of $655 million-$685 million, better than consensus of $653.5 million.

Fortinet (FTNT +1.01%) dropped 9% in after-hours trading after it said it sees Q4 revenue of $404 million-$412 million, below consensus of $416.9 million, and said it sees full-year revenue of $1.48 billion-$1.49 billion, the mid-point below consensus of $1.49 billion.

Mattel (MAT -0.52%) tumbled 19% in after-hours trading after it reported Q3 adjusted EPS of 9 cents, well below consensus of 57 cents.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 +0.21%) this morning are up +6.50 points (+0.25%). Thursday's closes: S&P 500 +0.13%, Dow Jones +0.31%, Nasdaq -0.28%. The S&P 500 on Thursday closed higher on carry-over support from a rally in European stocks after the ECB extended its QE program by 9 months and left open the option for a continuation beyond that. Stocks were also boosted by strong quarterly earnings results from Ford, UPS, and Twitter.

Dec 10-year T-note prices (ZNZ17 +0.01%) this morning are up +1 tick. Thursday's closes: TYZ7 -2.50, FVZ7 -2.00. Dec 10-year T-notes on Thursday closed lower on increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 1-1/2 week high, and by strength in stocks, which curbed the safe-haven demand for T-notes. T-notes found some support on the weaker-than-expected U.S. Sep pending home sales.

The dollar index (DXY00 +0.37%) this morning is up +0.28% to a 3-1/4 month high. EUR/USD (^EURUSD) is down -0.0036(-0.31%) to a 3-month low and USD/JPY (^USDJPY) is up +0.14 (+0.12%) to a 3-1/2 month high. Thursday's closes: Dollar Index +0.901 (+0.96%), EUR/USD -0.0162 (-1.37%), USD/JPY +0.24 (+0.21%). The dollar index on Thursday rallied to a 3-month high and settled higher on weakness in EUR/USD which fell to a 3-month low after the ECB extended its QE program until Sep 2018 and ECB President Draghi said the Eurozone still needs "ample" stimulus.

Dec crude oil (CLZ17 -0.13%) this morning is down -8 cents (-0.15%) and Dec gasoline (RBZ17 -0.17%) is -0.0058 (-0.34%). Thursday's closes: Dec WTI crude +0.46 (+0.88%), Dec gasoline +0.0156 (+0.93%). Dec crude oil and gasoline on Thursday closed higher on comments from Saudi Crown Prince Mohammed bin Salman who said that he backed the extension of OPEC crude production cuts beyond Mar of 2018. Crude oil prices were also supported by the increase in the crack spread to a 1-1/4 month high, which may spur refineries to boost their crude purchases to refine the crude into gasoline. Crude oil prices were undercut by the rally in the dollar index to a 3-month high.

Metals prices this morning are weaker with Dec gold (GCZ17 -0.17%) -1.5 (-0.12%) at a 3-week low, Dec silver (SIZ17-0.78%) -0.106 (-0.63%) at a 3-week low and Dec copper -0.055 (-1.72%) at a 1-1/2 week low. Thursday's closes: Dec gold -9.4 (-0.73%), Dec silver -0.114 (-0.67%), Dec copper (HGZ17 -2.14%) -0.0055 (-0.17%). Metals on Thursday closed lower on the rally in the dollar index to a 3-month high and by strength in stocks that reduced the safe-haven demand for precious metals.

Disclosure: None.