Morning Call For Friday, November 10

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 -0.38%) this morning are down -0.38% on pessimism U.S. legislators will be able to pass tax reform legislation after the Senate revealed Thursday that its tax plan would delay corporate tax cuts until 2019. The U.S. stock market has rallied sharply this year on expectations meaningful tax cuts would be implemented this year. European stocks are down -0.22% at a 2-week low as they followed U.S. stock indexes lower. Asian stocks settled mostly lower: Japan -0.82%, Hong Kong -0.05%, China +0.14%, Taiwan 0.10%, Australia -0.33%, Singapore -0.11%, South Korea -0.35%, India +0.19%. China's Shanghai Composite bucked the negative trend and rallied to a 1-3/4 year high, led by strength in financial stocks, after the government eased foreign ownership caps on banks and other financial companies.

The dollar index (DXY00 +0.05%) is up +0.09%. EUR/USD (^EURUSD) is up +0.03%. USD/JPY (^USDJPY) is down -0.01%.

Dec 10-year T-note prices (ZNZ17 -0.24%) are down -8.5 ticks at a 1-week low on hawkish comments from San Francisco Fed President Williams who expects a Fed rate hike next month and three more rate hikes next year.

San Francisco Fed President Williams said he expects a Fed rate hike at the Dec FOMC meeting and three more rate hikes in 2018 to return the fed funds rate to "a normal level" of about 2.5%.

UK Sep industrial production rose +0.7% m/m, stronger than expectations of +0.3% m/m and the largest increase in 7 months.

UK Sep manufacturing production rose +0.7% m/m, stronger than expectations of +0.3% m/m and the largest increase in 9 months.

UK Sep construction output fell -1.6% m/m, weaker than expectations of -0.9% m/m and the biggest decline in 1-1/2 years.

U.S. STOCK PREVIEW

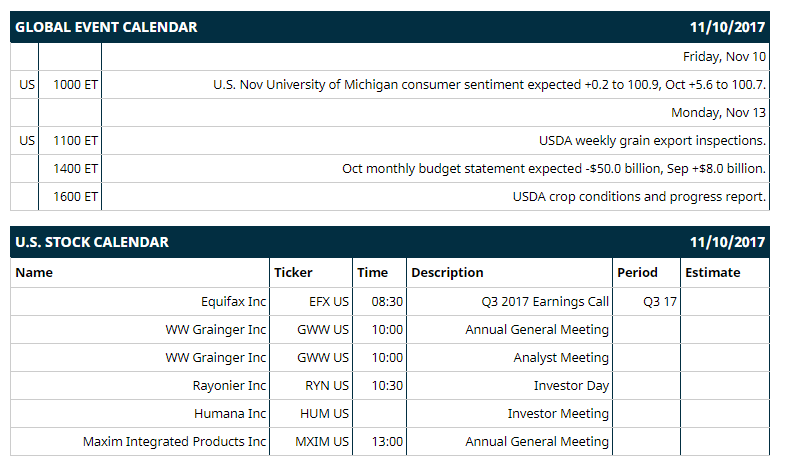

Key U.S. news today includes: (1) U.S. Nov University of Michigan consumer sentiment expected +0.2 to 100.9, Oct +5.6 to 100.7.

Notable Russell 2000 earnings reports today include: none.

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week: none.

OVERNIGHT U.S. STOCK MOVERS

Macy's (M +10.98%) was downgraded to 'Short' from no position at Evercore ISI.

Walt Disney (DIS +1.48%) gained over 1% in after-hours trading after it said in a conference call that it is making another trilogy of 'Star Wars' movies to be released after 2020.

Trade Desk (TTD -3.84%) tumbled 11% in after-hours trading after it said it sees Q4 revenue of $101.0 million, below consensus of $101.8 million.

Nvidia (NVDA -1.84%) gained almost 2% in after-hours trading after it reported Q3 revenue of $2.64 billion, higher than consensus of $2.36 billion, and then said it sees Q4 revenue of $2.65 billion plus or minus 2%, better than consensus of $2.44 billion.

Redfin (RDFN +6.91%) fell nearly 7% in after-hours trading after it reported Q3 revenue of $109.5 million, below consensus of $110.7 million.

Nordstrom (JWN +4.52%) lost nearly 1% in after-hours trading after it reported Q3 gross margin of 34.7%, below consensus of 35.1%.

Ichor Holdings Ltd (ICHR -2.07%) dropped over 4% in after-hours trading after it announced that it acquired Talon Innovations in a stock purchase agreement for $130 million.

Hertz Global Holdings (HTZ -4.67%) climbed 7% in after-hours trading after it reported Q3 adjusted EPS of $1.42, better than consensus of $1.33.

Intrexon (XON +0.51%) fell 3% in after-hours trading after it reported Q3 revenue of $46 million, weaker than consensus of $55.1 million.

Dynavax Technologies (DVAX -3.84%) rallied 14% in after-hours trading after the FDA approved its Heplisav-B vaccine for prevention of infection caused by hepatitis B in adults.

Airgain (AIR -0.62%) dropped 6% in after-hours trading after it reported Q3 adjusted EPS of 5 cents, below consensus of 7 cents.

Immunomedics (IMMU +3.06%) jumped over 8% in after-hours trading after the company appointed former president of hematology and oncology at Celgene, Michael Pehl, as CEO.

Lightpath Technologies (LPTH +0.81%) tumbled 14% in after-hours trading after it reported Q1 revenue of $7.6 million, below consensus of $8.4 million.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 -0.38%) this morning are down -9.75 points (-0.38%). Thursday's closes: S&P 500 -0.38%, Dow Jones -0.43%, Nasdaq -0.53%. The S&P 500 on Thursday closed lower on negative carry-over from a decline foreign equity markets after the Nikkei Stock Index retreated from a 25-3/4 year high and closed lower and after Euro Stoxx 50 fell to a 2-week low. There was also disappointment in the stock market after the Senate revealed that its tax plan would delay cutting corporate taxes until 2019.

Dec 10-year T-note prices (ZNZ17 -0.24%) this morning are down -8.5 ticks at a 1-week low. Thursday's closes: TYZ7 -2.00, FVZ7 +0.50. Dec 10-year T-notes on Thursday closed lower on negative carry-over from a slide in 10-year German bunds to a 1-week low after the European Commission raised its Eurozone 2017 and 2018 GDP estimates, which was hawkish for ECB monetary policy. T-note prices were also undercut by increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 1-1/2 week high. Losses were limited as the slide in stocks boosted the safe-haven demand for T-notes.

The dollar index (DXY00 +0.05%) this morning is up +0.081 (+0.09%). EUR/USD (^EURUSD) is up +0.0003 (+0.03%) and USD/JPY (^USDJPY) is down -0.01 (-0.01%). Thursday's closes: Dollar Index -0.422 (-0.44%), EUR/USD +0.0047 (+0.41%), USD/JPY -0.40 (-0.35%). The dollar index on Thursday closed lower on the slide in USD/JPY to a 1-week low as the decline in global stocks boosted the safe-haven demand for the yen. The dollar was also undercut by strength in EUR/USD after the European Commission raised its Eurozone GDP forecast. The dollar was also hurt by disappointment in the Senate's tax plan, which delays a corporate tax cut until 2019.

Dec crude oil (CLZ17 -0.10%) this morning is down -3 cents (-0.05%) and Dec gasoline (RBZ17 -0.04%) is +0.0003 (+0.02%). Thursday's closes: Dec WTI crude +0.36 (+0.63%), Dec gasoline -0.0016 (-0.09%). Dec crude oil and gasoline on Thursday settled mixed. Crude oil prices were boosted by a weaker dollar and the European Commission's hike in its Eurozone 2017 GDP estimate, which is positive for energy demand. Gasoline closed lower after the crack spread moved lower, which may curb refinery demand for crude oil to refine into gasoline.

Metals prices this morning are mixed with Dec gold (GCZ17 -0.19%) -3.3 (-0.26%), Dec silver (SIZ17 +0.32%) +0.020 (+0.12%) and Dec copper (HGZ17 +0.21%) +0.002 (+0.05%). Thursday's closes: Dec gold +7.9 (+0.62%), Dec silver -0.163(-0.95%), Dec copper -0.0135 (-0.44%). Metals on Thursday settled mixed with Dec copper at a 4-week low. Metals prices were supported by a weaker dollar and by the selloff in global stocks that boosted safe-haven demand for precious metals. Copper closed lower on Chinese demand concerns after Chinese customs data on Tuesday showed China Oct copper imports fell -23% m/m to 330,000 MT.

Disclosure: None.