Morning Call For Friday, Jan. 27

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 -0.02%) are down -0.05% and European stocks are down -0.56% as weakness in European banks drags the overall market lower. UBS is down nearly 3% and is leading losses in bank stocks after it reported margins at its wealth management business declined for a third straight quarter. Weakness in crude oil prices is also undercutting energy producing stocks with Mar WTI crude (CLH17 -0.61%) down -0.56% ahead of U.S. weekly rig count data. Baker Hughes reported last week that active U.S. oil rigs rose to their highest in 13-months. Strength in the dollar has also weakened gold prices with Feb COMEX gold (GCG17 -0.54%) down -0.50% at a 2-week low. Asian stocks settled mostly higher: Japan +0.34%, Hong Kong -0.06%, Australia +0.75%, Singapore +0.43%, India +0.63%. Markets in China, Taiwan and South Korea were closed for holiday. Japan's Nikkei Stock Index climbed to a 3-week high as deflation concerns eased after Japan Dec CPI was stronger than expected. Weakness in the yen also gave a boost to Japanese exporter stocks.

The dollar index (DXY00 +0.22%) is up +0.18%. EUR/USD (^EURUSD) is up +0.11% after German Dec import prices rose at their fastest pace in 4-3/4 years, which may spur the ECB to taper QE sooner rather than later. USD/JPY (^USDJPY) is up +0.47%.

Mar 10-year T-note prices (ZNH17 -0.05%) are down -1.5 ticks.

The Japan Dec national CPI rose +0.3% y/y, stronger than expectations of +0.2% y/y. Dec national CPI ex fresh food fell -0.2% y/y, stronger than expectations of -0.3% y/y. Dec national CPI ex food & energy was unch y/y, stronger than expectations of -0.1% y/y.

The German Dec import price index rose 3.5% y/y stronger than expectations of +2.7% y/y and the fastest pace of increase in 4-3/4 years.

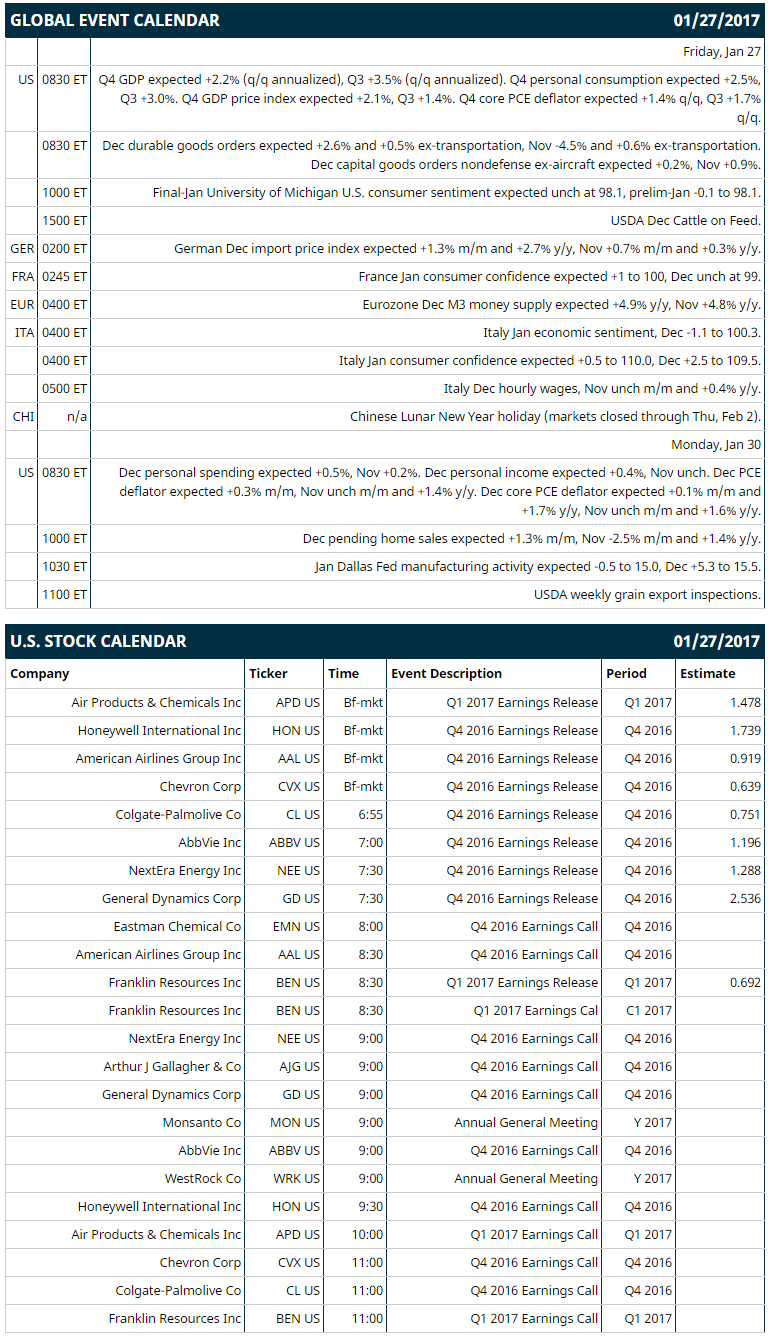

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Q4 GDP (expected +2.2% q/q annualized, Q3 +3.5%), (2) Dec durable goods orders (expected +2.6% and +0.5% ex-transportation, Nov -4.5% and +0.6% ex-transportation), (3) final-Jan University of Michigan U.S. consumer sentiment (expected unch at 98.1, prelim-Jan -0.1 to 98.1), (4) USDA Dec Cattle on Feed.

Notable S&P 500 earnings reports today include: Honeywell (consensus $1.74), American Airlines (0.92), Chevron (0.64), Colgate-Palmolive (0.75), AbbVie (1.20), NextEra Energy (1.29), General Dynamics (2.54).

U.S. IPO's scheduled to price today: none.

Equity conferences: none.

OVERNIGHT U.S. STOCK MOVERS

Alphabet (GOOGL -0.17%) slid nearly 3% in after-hours trading after it reported Q4 adjusted EPS of $9.36, lower than consensus of $9.62.

Starbucks (SBUX -0.41%) dropped over 3% in after-hours trading after it reported Q1 comparable same-store sales up 3.0%, weaker than consensus of +3.7%.

Microsoft (MSFT +0.93%) gained nearly 1% in after-hours trading after it reported Q2 adjusted EPS ex-LinkedIn of 84 cents, higher than consensus of 79 cents.

PayPal Holdings (PYPL -0.50%) fell over 3% in after-hours trading after it forecast 2017 adjusted EPS of $1.69-$1.74, weaker than consensus of $1.74.

Wynn Resorts Ltd (WYNN -0.95%) rallied 7% in after-hours trading after it reported Q4 net revenue of $1.30 billion, better than consensus of $1.27 billion.

Juniper Networks (JNPR -1.49%) dropped over 7% in after-hours trading after it said it sees Q1 adjusted EPS of 38 cents-44 cents, weaker than consensus of 46 cents.

Super Micro Computer (SMCI +0.35%) surged 10% in after-hours trading after it reported Q2 adjusted EPS of 48 cents, better than consensus of 46 cents, and then said it sees Q3 sales of $570 million to $630 million, well above consensus of $552.1 million.

Robert Half International (RHI +0.24%) slid nearly 5% in after-hours trading after it reported Q4 EPS of 61 cents, weaker than consensus of 64 cents.

KLA-Tencor Corp. (KLAC -1.68%) rose 3% in after-hours trading after it reported Q2 adjusted EPS of $1,52, higher than consensus of $1.40.

Proofpoint (PFPT +2.26%) fell 4% in after-hours trading after it reported Q4 billings of $138.4 million, below some analysts' estimates of $140 million.

Valero Energy (VLO -1.40%) gained almost 1% in after-hours trading after it boosted its quarterly dividend to 70 cents a share from 60 cents a share, higher than expectations of 65 cents.

Synaptics (SYNA -2.87%) jumped over 6% in after-hours trading after it reported Q2 net revenue of $461.3 million, above consensus of $451.8 million.

OSI Systems (OSIS -1.66%) climbed 3% in after-hours trading after it reported Q2 adjusted EPS of 68 cents, better than consensus of 61 cents.

Microsemi Corp. (MSCC +0.34%) slipped over 1% in after-hours trading after it reported Q1 adjusted EPS of 86 cents, right on expectations.

Greenhill & Co. (GHL -0.52%) rallied 5% in after-hours trading after it reported Q4 revenue of $101.6 million, higher than consensus of $100.7 million.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 -0.02%) this morning are down -1.25 points (-0.05%). Thursday's closes: S&P 500 -0.07%, Dow Jones +0.16%, Nasdaq +0.11%. The S&P 500 on Thursday fell back from a new all-time high and closed slightly lower. Stocks were undercut by the +22,000 rise in weekly jobless claims (vs expectations of +10,000) and the -10.4% plunge in U.S. Dec new home sales to 536,000, weaker than expectations of -0.7% to 588,000 and a 10-month low. Stocks found support on the +1.2 point rise in the U.S. Jan Markit services PMI to 55.1, stronger than expectations of +0.5 to 54.4 and the fastest pace of expansion in 14 months. There was also strength in energy producing stocks after crude oil prices rallied +1.95% to a 2-week high.

Mar 10-year T-notes (ZNH17 -0.05%) this morning are down -1.5 ticks. Thursday's closes: TYH7 +5.00, FVH7 +4.50. Mar 10-year T-notes on Thursday recovered from a 4-week low and closed higher on the larger-than-expected increase in U.S. weekly jobless claims and the the plunge in U.S. Dec new home sales to a 10-month low. T-notes were undercut by negative carry-over from the plunge in German bund prices to a 1-year low and by the rally in the S&P 500 to a fresh all-time high, which reduced demand for T-notes as a safe-haven.

The dollar index (DXY00 +0.22%) this morning is up +0.18 (+0.18%). EUR/USD (^EURUSD) is up +0.0012 (+0.11%). USD/JPY (^USDJPY) is up +0.54 (+0.47%). Thursday's closes: Dollar index +0.35 (+0.35%), EUR/USD -0.0066 (-0.61%), USD/JPY +1.25 (+1.10%). The dollar index on Thursday closed higher on strength in USD/JPY as the rally in the S&P 500 to an all-time high reduced the safe-haven demand for the yen. The dollar was also boosted by the +1.2 point increase in the U.S Jan Markit services PMI to a 14-month high of 55.1, which bolsters the case for additional Fed rate hikes.

Mar WTI crude oil prices (CLH17 -0.61%) this morning are down -30 cents (-0.56%) and Mar gasoline (RBH17 -0.28%) is -0.0032 (-0.20%). Thursday's closes: Mar crude +1.03 (+1.95%), Mar gasoline +0.0169 (+1.09%). Mar crude oil and gasoline on Thursday closed higher with Mar crude at a 2-week high. Crude oil prices were boosted by comments from Algerian Energy Minister Boutarfa who said that OPEC and other oil producers have cut 1.5 million bpd of oil output and are due to reach the 1.8 million bpd reduction target next month.

Disclosure: None.