Morning Call For Friday, Feb. 3

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 +0.16%) are up +0.15% and European stocks are up +0.63% ahead of this morning's U.S. payroll report that may provide clues as to the timing of the next Fed rate hike. Mar WTI crude oil (CLH17 +0.19%) is up +0.50% and is giving energy producing stocks a lift after President Trump tweeted this morning that Iran was "playing with fire" following its ballistic missile test this week. European stocks also found support after the Eurozone Jan Markit composite PMI was revised upward to its fastest pace in 3 years. Gains in stocks were contained as mining companies weakened as Mar COMEX copper prices (HGH17 -1.06%) fell -0.89% after a gauge of Chinese manufacturing activity weakened more than expected last month, and after Chinese copper supplies rose after weekly Shanghai copper inventories climbed +10,928 MT to 223,853 MT, an 8-1/2 month high. Asian stocks settled mixed: Japan +0.02%, Hong Kong -0.24%, China -0.60%, Taiwan +0.28%, Australia -0.42%, Singapore -0.07%, South Korea +0.13%, India +0.05%.

The dollar index (DXY00 +0.28%) is up +0.33%. EUR/USD (^EURUSD) is down -0.26% after ECB Executive Board member Praet said "the firming recovery is not yet sufficiently robust to ensure a self-sustained convergence of inflation rates to levels closer to 2%." USD/JPY (^USDJPY) is up +0.33%.

Mar 10-year T-note prices (ZNH17 -0.11%) are down -5.5 ticks.

ECB Executive Board member Praet said that "the firming recovery is not yet sufficiently robust to ensure a self-sustained convergence of inflation rates to levels closer to 2% as underlying inflation dynamics remain subdued, and risks and uncertainties still prevail, especially those related to the geopolitical environment."

The Eurozone Jan Markit composite PMI was revised upward to 54.4 from the originally reported 54.3, the fastest pace of expansion since the data series began in 2014.

The China Jan Caixin (flash) manufacturing PMI fell -0.9 to 51.0, weaker than expectations of -0.1 to 51.8.

U.S. STOCK PREVIEW

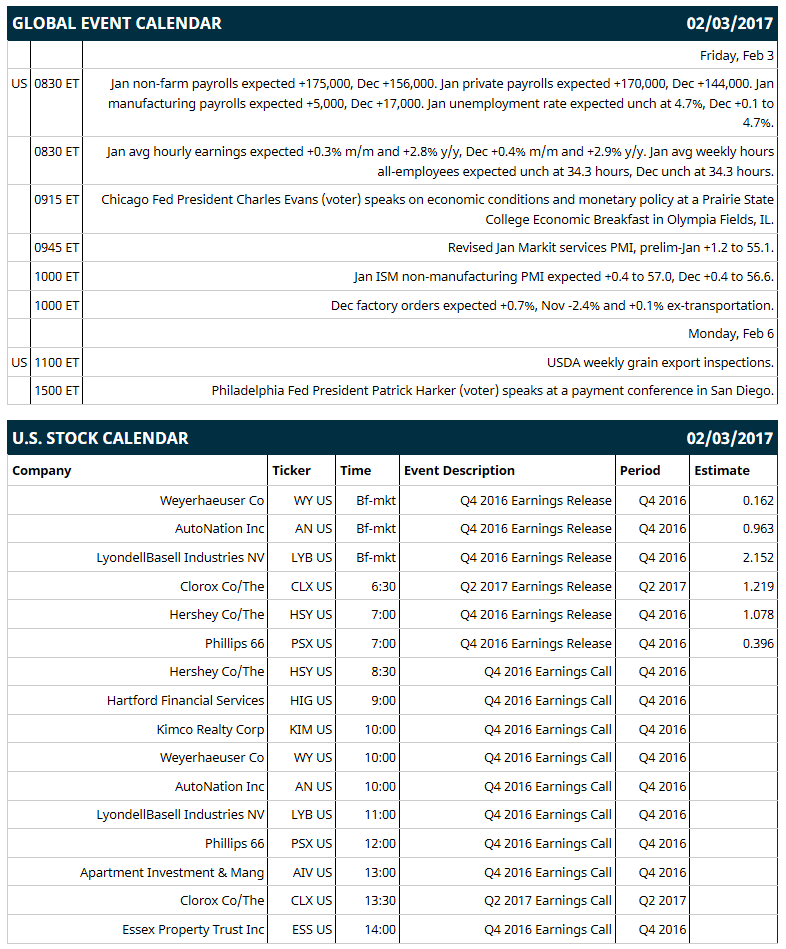

Key U.S. news today includes: (1) Jan non-farm payrolls (expected +175,000, Dec +156,000) and Jan unemployment rate (expected unch at 4.7%, Dec +0.1 to 4.7%), (2) Chicago Fed President Charles Evans (voter) speaks on economic conditions and monetary policy at a Prairie State College Economic Breakfast in Olympia Fields, IL, (3) revised Jan Markit services PMI (prelim-Jan +1.2 to 55.1), (4) Jan ISM non-manufacturing PMI (expected +0.4 to 57.0, Dec +0.4 to 56.6), (5) Dec factory orders expected +0.7%, Nov -2.4% and +0.1% ex-transportation.

Notable S&P 500 earnings reports today include: Weyerhaeuser (consensus $0.16), AutoNation (0.96), LyondellBasell (2.17), Clorox (1.22), Hershey (1.08), Phillips (0.40).

U.S. IPO's scheduled to price today: none.

Equity conferences: none.

OVERNIGHT U.S. STOCK MOVERS

Visa (V -0.17%) rose 3% in after-hours trading after it reported Q1 operating revenue of $4.5 billion, above consensus of $4.3 billion, and then was initiated with an 'Outperform' at RBC Capital Markets with a 12-month target price of $97.

Amazon.com (AMZN +0.91%) fell 4% in after-hours trading after it reported Q4 net sales of $43.7 billion, below consensus of $44.7 billion, and said it sees Q1 net sales of $33.3 billion-$35.8 billion, less than consensus of $36.0 billion.

Esterline Technologies (ESL +0.70%) rallied over 4% in after-hours trading after it reported Q1 adjusted EPS continuing operations of 82 cents, well above consensus of 46 cents.

Tableau Software (DATA -0.52%) surged 13% in after-hours trading after it reported Q4 revenue of $250.7 million, well above consensus of $230.2 million.

Amgen (AMGN -0.06%) rose nearly 3% in after-hours trading after it reported that a Phase 3 trial of its Repatha showed significantly reduced risk of cardiovascular events in patients with atherosclerotic cardiovascular disease.

Computer Sciences (CSC +1.12%) gained 2% in after-hours trading after it reported Q3 adjusted EPS continuing operations of 81 cents, higher than consensus of 70 cents.

Fortinet (FTNT +0.24%) climbed 10% in after-hours trading after it forecast full-year EPS of 87 cents-89 cents, better than consensus of 80 cents.

Cypress Semiconductor (CY -1.58%) rallied 5% in after-hours trading after it reported Q4 adjusted revenue of $530.2 million, higher than consensus of $525.6 million.

athenahealth (ATHN +1.41%) tumbled 7% in after-hours trading after it reported Q4 revenue of $288.2 million, below consensus of $303.7 million.

Hanesbrands (HBI -2.24%) sank over 10% in after-hours trading after it said it sees 2017 adjusted EPS of $1.93-$2.03, below consensus of $2.14.

GoPro (GPRO +3.78%) tumbled 13% in after-hours trading after it said it sees Q1 revenue of $190 million=-$210 million, well below consensus of $267.6 million.

Paylocity Holding (PCTY -1.32%) jumped 8% in after-hours trading after it said it sees fiscal 2017 adjusted EPS of 41 cents-43 cents, stronger than consensus of 38 cents.

Deckers Outdoor (DECK -2.30%) plunged over 20% in after-hours trading after it reported Q3 adjusted EPS of $4.11, below consensus of $4.22, and then cut its 2017 adjusted EPS forecast to $3.45-$3.55 from a prior view of $4.05-$4.25.

Neos Therapeutics (NEOS unch) slumped 14% in after-hours trading after it announced an offering of common stock, although no size was given.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 +0.16%) this morning are up +3.50 points (+0.15%). Thursday's closes: S&P 500 +0.06%, Dow Jones -0.03%, Nasdaq -0.10%. The S&P 500 on Thursday closed slightly higher on the -14,000 decline in U.S. weekly jobless claims (a bigger decline than expectations of -9,000) and the +1.3% increase in U.S. Q4 non-farm productivity (better than expectations of +1.0%). Stocks were undercut by uncertainty regarding the Trump administration’s fiscal and trade policies and by position squaring ahead of Friday's monthly U.S. payrolls report.

Mar 10-year T-notes (ZNH17 -0.11%) this morning are down -5.5 ticks. Thursday's closes: TYH7 +1.50, FVH7 +1.00. Mar 10-year T-notes on Thursday rallied to a 1-week high and closed higher on positive carry-over from Wednesday's post-FOMC meeting statement where policy makers gave no signal as to the timing of another interest rate hike.

The dollar index (DXY00 +0.28%) this morning is up +0.33 (+0.33%). EUR/USD (^EURUSD) is down -0.0028 (-0.26%). USD/JPY (^USDJPY) is up +0.37 (+0.33%). Thursday's closes: Dollar index +0.149 (+0.15%), EUR/USD -0.0010 (-0.09%), USD/JPY -0.45 (-0.40%). The dollar index on Thursday recovered from a 2-1/2 month low and closed higher on the larger-than-expected decline in U.S. weekly initial unemployment claims, a sign of labor market strength, and the larger-than-expected increase in U.S. Q4 non-farm productivity. The dollar index posted an early 2-1/2 month low on negative carry-over from Wednesday's FOMC meeting where policy makers failed to signal the timing of the next Fed interest rate increase.

Mar WTI crude oil prices (CLH17 +0.19%) this morning are up +27 cents (+0.50%) and Mar gasoline (RBH17 -0.11%) is +0.0063 (+0.41%). Thursday's closes: Mar crude -0.34 (-0.63%), Mar gasoline -0.0462 (-2.93%). Mar crude oil and gasoline on Thursday closed lower on concern that ramped-up oil production in Libya and Nigeria may offset cuts in crude production from other OPEC members as Libya's crude output rose to 690,000 bpd, a 2-year high, and Nigerian Jan crude production rose to 1.64 million bpd, up +9.3% m/m. In addition, the slide in the crack spread to a 2-1/4 month low, which may curb refinery demand for crude.

(Click on image to enlarge)

Disclosure: None.

Thanks for sharing