Morning Call For February 22, 2016

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH16 +1.02%) are up +1.15% at a 3-week high and European stocks are up % +2.10%. The price of crude oil is up +3.64%, which boosted energy producers with Chevron up 1.5% and Exxon Mobile up 1.1% in pre-market trading. Copper prices are up +2.22% at a 2-week high, which has boosted European mining stocks with Rio Tinto Group and BHP Billiton Ltd. both up more than 5%. Gains in European stocks were limited after manufacturing data showed that the Eurozone Feb Markit manufacturing PMI fell more than expected to its slowest pace of expansion in a year. Asian stocks settled mostly higher: Japan +0.90%, Hong Kong +0.93%, China +2.35%, Taiwan +0.02%, Australia +0.98%, Singapore +0.14%, South Korea -0.14%, India +0.34%. China's Shanghai Composite climbed to a 4-week high after the government replaced the country's securities regulator chairman, which bolstered speculation that he will take steps to improve confidence in China's stock market.

The dollar index (DXY00 +0.96%) is up +0.87% at a 2-week high. EUR/USD (^EURUSD) is down -0.80% at a 2-week low after weaker-than-expected Eurozone PMI data increases the chance that the ECB expands stimulus measures when it meets next month. USD/JPY (^USDJPY) is up +0.59%. GBP/USD is down -2.09% to a 1-month low as a split in the UK's ruling party over European Union membership increases the chance that the UK will exit the EU.

Mar T-note prices (ZNH16 -0.16%) are down -10 ticks.

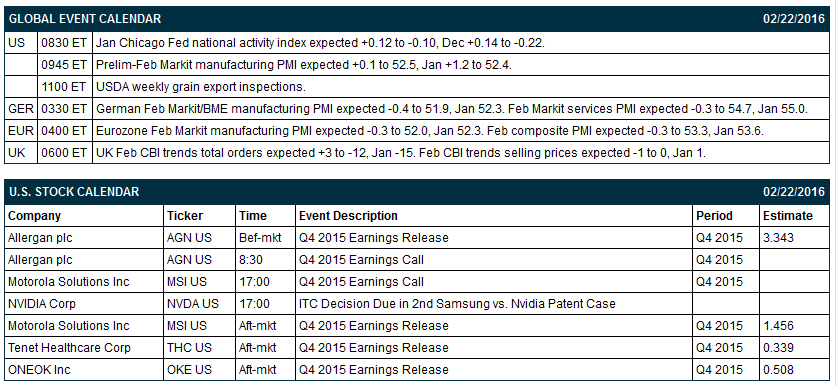

The Eurozone Feb Markit manufacturing PMI fell -1.3 to 51.0, weaker than expectations of -0.3 to 52.0 and the slowest pace of expansion in a year.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Jan Chicago Fed national activity index (expected +0.12 to -0.10, Dec +0.14 to -0.22), and (2) prelim-Feb Markit manufacturing PMI (expected +0.1 to 52.5, Jan +1.2 to 52.4).

There are 4 of the S&P 500 companies that report earnings today: Motorola Solutions (consensus $1.46), Allergan (3.34), Tenet Healthcare (0.34), ONEOK (0.51).

U.S. IPO's scheduled to price today: Advanced Inhalation Therapies (AITP).

Equity conferences this week include: Keefe, Bruyette, & Woods Cards, Payments & Financial Technology Symposium on Mon, Credit Suisse Energy Summit on Tue, Jefferies Media & Communications Conference on Tue-Wed, RBC Capital Markets Health Care Conference on Tue-Wed, IHS Energy CERAWeek Conference on Tue-Thu, Wells Fargo Bank Investors Forum on Wed, Cantor Fitzgerald Internet & Technology Conference on Thu, Gabelli & Company Pump, Valve and Water Systems Symposium on Thu.

OVERNIGHT U.S. STOCK MOVERS

Yahoo! (YHOO +2.11%) rose nearly 2% in pre-market trading after people familiar with the matter said the company will approach potential buyers as soon as today as it seeks bidders for its core business.

Energy producers and energy service companies rallied in pre-market trading as the price of crude oil rose with Chevron (CVX -0.27%) up 1.5%, Exxon Mobile (XOM +0.06%) up 1.1% and Transocean Ltd. (RIG -3.81%) up 2.4%.

Union Pacific (UNP +1.58%) was upgraded to 'Buy' from 'Neutral' at Bank of America.

Lumber Liquidators (LL -1.46%) plunged 14% in pre-market trading after U.S. regulators reversed their own finding from earlier this month and now said that the company's flooring was found to test three times higher the risk of causing cancer than previously stated.

TripAdvisor (TRIP +0.55%) was downgraded to 'Sell' from 'Hold' at Stifel with a 12-month price target of $53.

Flowserve (FLS -4.08%) was downgraded to 'Hold' from 'Buy' at Maxim Group,

Gamco reported a 18.04% stake in Journal Media Group (JMG +0.17%) .

Western Union (WU -0.11%) said it was served a Federal Grand Jury subpoena on gaming from transactions by 43 Nicaraguan agents from Oct 2008-Oct 2013.

Gamco reported a 23.01% stake in Myers Industries (MYE unch) .

Medtronic (MDT +0.55%) failed to win FDA panel backing on its DIAM Spinal Stabilization System after a FDA advisory panel voted 7-0 that benefits of the spinal device do not outweigh the risks.

Pfizer (PFE -0.20%) won FDA approval for treatment of breast cancer with its Ibrance in combination with fulvestrant in women with disease progression following endocrine therapy.

Healthcare insurers rallied in after-hours trading Friday with Anthem (ANTM -0.62%) up +1.5%, UnitedHealth Group (UNH +0.20%) up +1%, WellCare Health Plans (WCG -1.34%) up +0.8% and Aetna (AET -0.89%) up +0.3% after the Centers for Medicare and Medicaid Services (CMS) proposed that U.S. payments to private insurers that provide Medicare coverage will go up by about 1.35% next year.

MARKET COMMENTS

Mar E-mini S&Ps (ESH16 +1.02%) this morning are up +22.00 points (+1.15%) at a 3-week high. Friday's closes: S&P 500 unch, Dow Jones -0.13%, Nasdaq +0.30%. The S&P 500 on Friday closed little changed. Stocks were undercut by the -3% sell-off in crude oil prices, which undercut energy producing stocks, and increased price pressures after U.S. Jan core CPI rose +0.3% m/m and +2.2% y/y, stronger than expectations of +0.2% m/m and +2.1% y/y, which bolstered the case for the Fed to keep raising interest rates. Stocks were boosted by a rally in technology stocks, led by a 7% jump in Applied Materials, and by comments from San Francisco Fed President John Williams who said "the economy is actually doing fine" and he sees a gradual U.S. rate hike path as the "best course."

Mar 10-year T-notes (ZNH16 -0.16%) this morning are down -10 ticks. Friday's closes: TYH6 -0.50, FVH6 -3.00. Mar T-notes on Friday closed little changed. T-notes were boosted by carry-over support from a rally in German bunds to a 1-week high and by a flattening of the yield curve which prompted selling of the short end of the curve and buying of the long end of the Treasury curve. T-notes were undercut by increased price pressures after U.S. Jan core CPI rose +0.3% m/m, stronger than expectations of +0.2% m/m and the fastest monthly pace of increase in 4-1/3 years.

The dollar index (DXY00 +0.96%) this morning is up +0.841 (+0.87%). EUR/USD (^EURUSD) is down -0.0089 (-0.80%) at a 2-week low. USD/JPY (^USDJPY) is up +0.67 (+0.59%). Friday's closes: Dollar Index -0.351 (-0.36%), EUR/USD +0.0023 (+0.21%), USD/JPY -0.61 (-0.54%). The dollar index on Friday fell back from a 1-1/2 week high and closed lower on weakness in USD/JPY as a slide in stocks boosted the safe-haven demand for the yen and on comments from San Francisco Fed President Williams who said that he sees a gradual U.S. rate hike path as the "best course." The dollar index posted a 1-1/2 week high early in the session after U.S Jan CPI rose more than expected, which bolstered the case for the Fed to keep raising interest rates.

Mar WTI crude (CLH16 +3.58%) this morning is up +$1.08 a barrel (+3.64%) and Mar gasoline (RBH16 +3.91%) is up +0.0366 (+3.81%). Friday's closes: CLH6 -1.05 (-3.41%), RBH6 -0.0081 (-0.83%). Mar crude oil and gasoline on Friday closed lower with Mar gasoline at a 1-week low. Crude oil prices were undercut by concern that the crude oil supply glut will persist after Thursday's EIA data showed a +2.147 million bbl increase in EIA crude inventories to a record high 504.1 million bbl and by the sell-off in stocks, which curbs confidence in the economic outlook and energy demand.

(Click on image to enlarge)

Disclosure: None.