Morning Call For February 2, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.25%) this morning are up +0.38% as energy producers and oil service providers gained in pre-market trading after crude oil jumped to a 2-week high, while European stocks are down -0.12%, led by a plunge in Spanish bank stocks, on concern Spain may try to follow Greece in attempting to renegotiate the country's debt. The leader of Spain's anti-austerity party, Podemos, pledged to restructure Spain's debt if his party can convert its opinion-poll lead into victory in elections later this year. Asian stocks closed mixed: Japan -0.66%, Hong Kong -0.09%, China -2.34%, Taiwan +0.27%, Australia +0.66%, Singapore +0.95%, South Korea +0.29%, India -0.21%. China's Shanghai Stock Index fell to a 1-1/2 week low after a gauge of Chinese manufacturing signaled contraction for the first time in over two years. Commodity prices are mostly higher. Mar crude oil (CLH15 +0.58%) is up +3.11% at a 2-week high and Mar gasoline (RBH15 +2.84%) is up +5.00% at a 1-month high after a strike by oil workers in refineries that account for 10% of U.S. refining capacity enters its second day. Feb gold (GCG15 -0.24%) is down -0.24%. Mar copper (HGH15 +0.12%) is up +0.80%. Agriculture prices are higher. The dollar index (DXY00 -0.07%) is down -0.12%. EUR/USD (^EURUSD) is up +0.25%. USD/JPY (^USDJPY) is up +0.14%. Mar T-note prices (ZNH15 -0.02%) are down -0.5 of a tick.

The China Jan manufacturing PMI unexpectedly fell -0.3 to 49.8, weaker than expectations of +0.1 to 50.2 and the first time manufacturing activity has contracted in 28 months. The Jan non-manufacturing PMI fell -0.4 to 53.7, the slowest pace of expansion in a year.

The German Jan Markit/BME manufacturing PMI was revised downward to 50.9 from the originally reported 51.0.

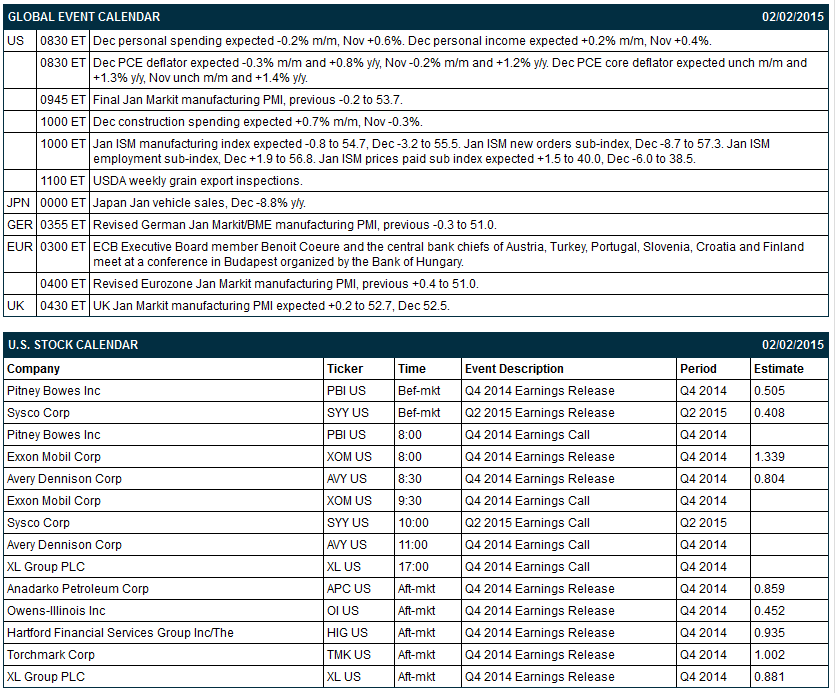

UK Jan Markit manufacturing PMI rose +0.5 from an upward revised 52.7 in Dec to 53.0, better than expectations of +0.2 to 52.7.

Japan Jan vehicle sales fell -18.9% y/y, the biggest decline in 3-1/3 years and the sixth consecutive month sales have fallen.

U.S. STOCK PREVIEW

Today’s Jan ISM manufacturing index is expected to show a -0.8 decline to 54.7, which would be the third monthly decline in a row. Today’s Dec personal income report is expected to show a small increase of +0.2% and the Dec personal spending report is expected to show a decline of -0.2% m/m. Today’s Dec PCE deflator is expected to fall to +0.8% y/y from +1.2% in November. Meanwhile, today’s Dec core PCE deflator is expected to edge lower to +1.3% y/y from +1.4% in November.

There are 9 of the S&P 500 companies that report earnings today: Exxon (consensus $1.34), Pitney Bowes (0.51), Sysco (0.41), Avery Dennison (0.80), Anadarko Petroleum (0.86), Owens-Illinois (0.45), Hartford ((0.94), Torchmark (1.00), XL Group (0.88). Equity conferences this week include: ANS Conference on Nuclear Training and Education on Mon-Tue, In-Pharma Osaka 2015 on Tue, Media Insights & Engagement Conference on Tue-Thu, Cowen and Company Aerospace/Defense Conference & Transport Forum on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

Tenneco (TEN -2.15%) reported Q4 adjusted EPS of $1.05, higher than consensus of 99 cents.

NuStar Energy (NS +3.11%) upgraded to 'Buy' from 'Neutral' at UBS.

Western Gas Partners (WES +1.12%) was reinstated with an 'Overweight' at Barclays with a price target of $84.

Delta Air Lines (DAL -5.78%) and Spirit Airlines (SAVE -7.09%) were both upgraded to 'Strong Buy' from 'Outperform' at Raymond James.

Wyndham (WYN -2.07%) was downgraded to 'Sell' from 'Hold' at Deutsche Bank.

Abercrombie & Fitch (ANF -2.18%) and Guess (GES -4.86%) were both downgraded to 'Sell' from 'Hold' at Evercore ISI.

1-800-Flowers.com (FLWS +3.14%) reported Q2 EPS of 68 cents, below consensus of 80 cents.

Diamond Foods (DMND -9.93%) was upgraded to 'Outperform' from 'Market Perform' at BMO Capital.

Pitney Bowes (PBI -0.29%) reported Q4 EPS of 51 cents, right on expectations

Sysco (SYY -1.83%) reported Q2 EPS of 41 cents, right on consensus.

Shire (SHPG -1.31%) announced that the U.S. FDA approved its Vyvanse Capsules, the first and only medication for the treatment of moderate to severe binge eating disorder in adults.

Nicholas Woodman reported a 44.9% passive stake in GoPro (GPRO -2.14%) .

JPMorgan Chase reported a 6.5% passive stake in Brandywine Realty (BDN -1.66%) .

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +0.25%) this morning are up +7.50 poinrs (+0.38%). The S&P 500 index on Friday closed lower: S&P 500 -1.30%, Dow Jones -1.45%, Nasdaq -0.79%. Negative factors included (1) carry-over weakness from a slide in European stocks on deflation concerns after the Eurozone Jan CPI estimate fell by -0.6% y/y and matched the July 2009 decline as the biggest drop since the euro currency was introduced in 1999, and (2) U.S. economic concerns after U.S. Q4 GDP rose +2.6% q/q annualized, weaker than expectations of +3.0%.

Mar 10-year T-notes (ZNH15 -0.02%) this morning are down -0.5 of a tick. Mar 10-year T-note futures prices on Friday posted a contract high and closed higher and the 10-year T-note yield fell to a 1-1/2 year low of 1.65%. Closes: TYH5 +22.00, FVH5 +14.75. Bullish factors included (1) concern about a slowdown in the U.S. economy after Q4 GDP expanded at a 2.6% pace, weaker expectations of +3.0%, and (2) carry-over support from a rally in German bund prices to a record high on deflation concerns after Eurozone Jan CPI fell -0.6% y/y and matched the biggest drop since the euro currency was introduced in 1999.

The dollar index (DXY00 -0.07%) this morning is down -0.111 (-0.12%). EUR/USD (^EURUSD) is up +0.0028 (+0.25%). USD/JPY (^USDJPY) is up +0.16 (+0.14%). The dollar index on Friday closed higher: Dollar index +0.022 (+0.02%), EUR/USD -0.00400 (-0.35%), USD/JPY -0.765 (-0.65%). Bullish factors included (1) hawkish comments from St. Louis Fed President Bullard who said it is “reasonable” to expect an interest rate increase in June or July, and (2) weakness in EUR/USD on deflation concerns after Eurozone Jan core CPI rose +0.6% y/y, the slowest pace of increase since the euro currency was introduced in 1999.

Mar WTI crude oil (CLH15 +0.58%) this morning is up $1.50 (+3.11%) at a 2-week high and Mar gasoline (RBH15 +2.84%) is up +0.0739 (+5.00%) at a 1-month high. Mar crude oil and Mar gasoline on Friday closed sharply higher with Mar crude at a 1-week high and Mar gasoline at a 1-month high: CLH5 +3.71 (+8.33%), RBH5 +0.0875 (+6.29%). Bullish factors included (1) concern that the recent plunge in crude prices will curb U.S, oil output after the Baker Hughes operating oil rig count sank to a 3-year low of 1,223, (2) the unexpected increase in the Jan Chicago PMI, which spurred short covering in crude, and (3) the better-than-expected +4.3% increase in Q4 U.S. personal consumption, which signals increased fuel demand.

Click on picture to enlarge

Disclosure: None.