Morning Call For February 1, 2016

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH16 -0.62%) are down -0.35% and European stocks are down -0.71% as Chinese economic concerns intensified after Chinese manufacturing activity last month contracted by the most in 3-1/3 years. Concerns over a slowdown in China have also undercut crude oil and copper prices and dragged energy and commodity producer stocks lower as well. On the positive side for European stocks, the German Jan Markit/BME manufacturing PMI was revised higher. Asian stocks settled mixed: Japan +1.98%, Hong Kong -0.45%, China -1.78%, Taiwan +0.14%, Australia +0.76%, Singapore -1.02%, South Korea +0.68%, India -0.18%. Japan's Nikkei Stock Index climbed to a 3-week high on positive carryover from Friday's decision by the BOJ to adopt negative interest rates on some of the deposits held at the central bank. The BOJ's action also fueled buying of Japanese government bonds as the 10-year Japan bond yield fell to a record low of 0.05%.

The dollar index (DXY00 -0.23%) is down -0.21%. EUR/USD (^EURUSD) is up +0.31%. USD/JPY (^USDJPY) is up +0.20%.

Mar T-note prices (ZNH16 -0.06%) are down -2 ticks.

The German Jan Markit/BME manufacturing PMI was revised upward to 52.3 from the originally reported 52.1.

The China Jan manufacturing PMI fell -0.3 to 49.4, weaker than expectations of -0.1 to 49.6 and the steepest pace of contraction in 3-1/3 years.

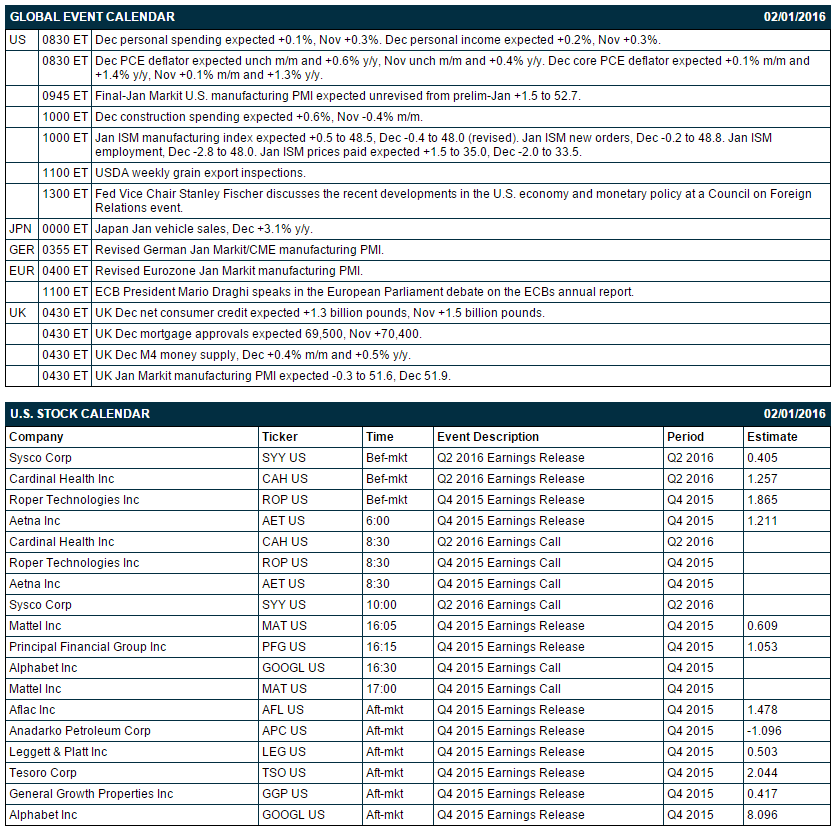

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Dec personal spending (expected +0.1%, Nov +0.3%) and Dec personal income (expected +0.2%, Nov +0.3%), (2) Dec PCE deflator (expected unch m/m and +0.6% y/y, Nov unch m/m and +0.4% y/y) and Dec core PCE deflator (expected +0.1% m/m and +1.4% y/y, Nov +0.1% m/m and +1.3% y/y), (3) Final-Jan Markit U.S. manufacturing PMI (expected unrevised from prelim-Jan +1.5 to 52.7), (4) Dec construction spending expected +0.6%, Nov -0.4% m/m, (5) Jan ISM manufacturing index (expected +0.5 to 48.5, Dec -0.4 to 48.0), and (6) Fed Vice Chair Stanley Fischer discusses the recent developments in the U.S. economy and monetary policy at a Council on Foreign Relations event.

There are 12 of the S&P 500 companies that report earnings today with notable reports including: Alphabet Inc (consensus $8.10), General Growth Properties (0.42), Mattel (0.61), Cardinal Health (1.26), Sysco (0.41).

U.S. IPO's scheduled to price today: none.

Equity conferences this week include: Cowen and Company Aerospace/Defense Conference & Transport Forum on Wed-Thu

OVERNIGHT U.S. STOCK MOVERS

Roper Technologies (ROP +3.51%) reported Q4 EPS of $1.82, below consensus of $1.87.

Dominion Resources (D +1.73%) reported Q4 EPS of 70 cents, less than consensus of 88 cents.

Aetna (AET reported Q4 EPS of $1.37, better than consensus of $1.21.

Genuine Parts (GPC +3.38%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Air Products & Chemicals (APD +6.47%) was upgraded to 'Buy' from 'Neutral' at UBS with a price target of $151.

L-3 Communications (LLL +4.34%) was upgraded to 'Buy' from 'Underperform' at Bank of America.

Northrup Grumman (NOC +2.73%) was upgraded to 'Buy' from 'Neutral' at Bank of America.

Chipolte Mexican Grill (CMG -0.02%) rose over 1% in pre-market trading on reports that the U.S. Centers for DIsease COntrol and Prevention may declare an end to the E. Coli outbreak today that has plagued the restaurant chain over the past couple of months.

Resource America (REXI +1.63%) said it has hired Evercore for strategic, financial options that may include, but aren't limited to, monetizing non-core assets, expanding the stock buyback program, and a partial of full sale of the company.

Apollo Global's (APO +1.12%) co-founder Josh Harris said that Apollo's LBO financing market has "dried up" amid a financing struggle.

Care Capital Properties (CCP +1.35%) filed to offer as much as $250 million in common stock.

According to Platts reports, ArcelorMittal (MT -4.74%) is in discussions on the sale of some of its U.S. long steel mills, including the one in Steelton, PA.

MARKET COMMENTS

Mar E-mini S&Ps (ESH16 -0.62%) this morning are down -6.75 points (-0.35%). Friday's closes: S&P 500 +2.48%, Dow Jones +2.47%, Nasdaq +2.22%. The S&P 500 on Friday rallied to a 2-week high and closed sharply higher on carryover support from a +2.80 rally in the Nikkei Stock Index after the BOJ stepped up stimulus efforts and adopted a negative -0.1% interest rate on reserves held at the BOJ. Stocks were also supported by reduced concerns about a Fed rate hike U.S. Q4 GDP rose by only +0.7%, weaker than expectations of +0.8%.

Mar 10-year T-notes (ZNH16 -0.06%) this morning are down -2 ticks. Friday's closes: TYH6 +17.50, FVH6 +10.25. Mar T-notes on Friday rallied to a contract high on the weaker-than-expected U.S. Q4 GDP of +0.7%, which caused the market to further postpone expectations for the Fed's next rate hike. T-notes also received carryover support from a rally in Japanese 10-year bonds to a new all-time high after the BOJ unexpectedly adopted a negative interest rate for reserves held at the BOJ.

The dollar index (DXY00 -0.23%) this morning is down -0.205 (-0.21%). EUR/USD (^EURUSD) is up +0.0034 (+0.31%). USD/JPY (^USDJPY) is up +0.24 (+0.20%). Friday's closes: Dollar Index +1.096 (+1.11%), EUR/USD -0.0109 (-1.00%), USD/JPY +2.32 (+1.95%). The dollar index on Friday rose to a 1-3/4 month high and closed higher on the sharp rally in USD/JPY to a 1-1/2 month high after the BOJ unexpectedly adopted a negative interest rate for reserves held at the BOJ. The dollar index also saw strength on a decline in in EUR/USD after German Dec retail sales unexpectedly fell -0.2%m/m, weaker than expectations of +0.4% m/m.

Mar crude oil (CLH16 -3.27%) this morning is down -54 cents (-1.61%) and Mar gasoline (RBH16 -2.37%) is down -0.0103 (-0.91%). Friday's closes: CLH6 +0.40 (+1.20%), RBH6 +0.0320 (+2.91%). Mar crude oil and gasoline on Friday closed higher on the rally in the S&P 500 to a 2-week high and the fall in U.S. active oil rigs by 12 to 498, the fewest in 5-3/4 years. Crude oil prices were undercut by the rally in the dollar index to a 1-3/4 month high, the weaker-than-expected U.S. Q4 GDP report of +0.7%, and Russian Energy Minister Novak's comment that "no meeting has been confirmed" between Russia and OPEC, which reduced speculation of a coordinated oil production cut between Russia and OPEC.

Disclosure: None.