Morning Call For December 18, 2014

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +1.15%) this morning are up +1.06% and European stocks are up +2.35% as energy producers gained as crude oil rallied and on carry-over support from yesterday's FOMC meeting where the Fed pledged patience on raising interest rates. European stocks also received a boost after German investor confidence rose for a second month to a 4-month high. European government bonds rose after the Swiss National Bank (SNB) introduced negative interest rates for the first time since the 1970s as the Russian financial crisis and the threat of further ECB stimulus pressured the Swiss franc. Asian stocks closed mostly higher: Japan +2.32%, Hong Kong +1.09%, China -0.44%, Taiwan +0.57%, Australia +0.95%, Singapore +0.51%, South Korea +0.04%, India +1.56%. Commodity prices are higher. Jan crude oil (CLF15 +3.22%) is up +2.32% Jan gasoline (RBF15 +3.23%) is up +2.59%. Feb gold (GCG15 +0.95%) is up +1.05%. Mar copper (HGH15 -0.05%) is up +0.35%. Agriculture prices are stronger with Mar corn at a 5-1/2 month high and Mar wheat at a 6-3/4 month high. The dollar index (DXY00 -0.01%) is down -0.10%. EUR/USD (^EURUSD) is down -0.28% at a 1-week low as the action by the SNB to introduce negative interest rates that applies on the same date as the next ECB meeting boosted speculation the ECB will expand stimulus. USD/JPY (^USDJPY) is down -0.02%. Mar T-note prices (ZNH15 -0.21%) are down -7.5 ticks.

The German Dec IFO business climate rose +0.8 to 105.5, right on expectations and the highest in 4 months. The Dec IFO current assessment was unchanged at 110.0, weaker than expectations of +0.4 to 110.4. The Dec IFO expectations rose +1.3 to 101.1, better than expectations of +0.8 to 100.5.

The Swiss National Bank (SNB) imposed a negative interest rate of -0.25% on slight deposit account balances at the SNB that will apply as of Jan 22, The SNB also expanded the target range for the 3-month Libor to -0.75% to 0.25%.

UK Nov retail sales ex autos rose +1.7% m/m, stronger than expectations of +0.3% m/m and the largest increase in 11 months. On an annual basis, Nov retail sales ex autos rose +6.9% y/y, better than expectations of +4.5% y/y. Nov retail sales including autos rose +1.6% m/m and +6.4% y/y, with the +6.4% y/y increase the largest annual gain in 10-1/2 years.

Eurozone Oct construction output rose +1.3% m/m and +1.4% y/y.

U.S. STOCK PREVIEW

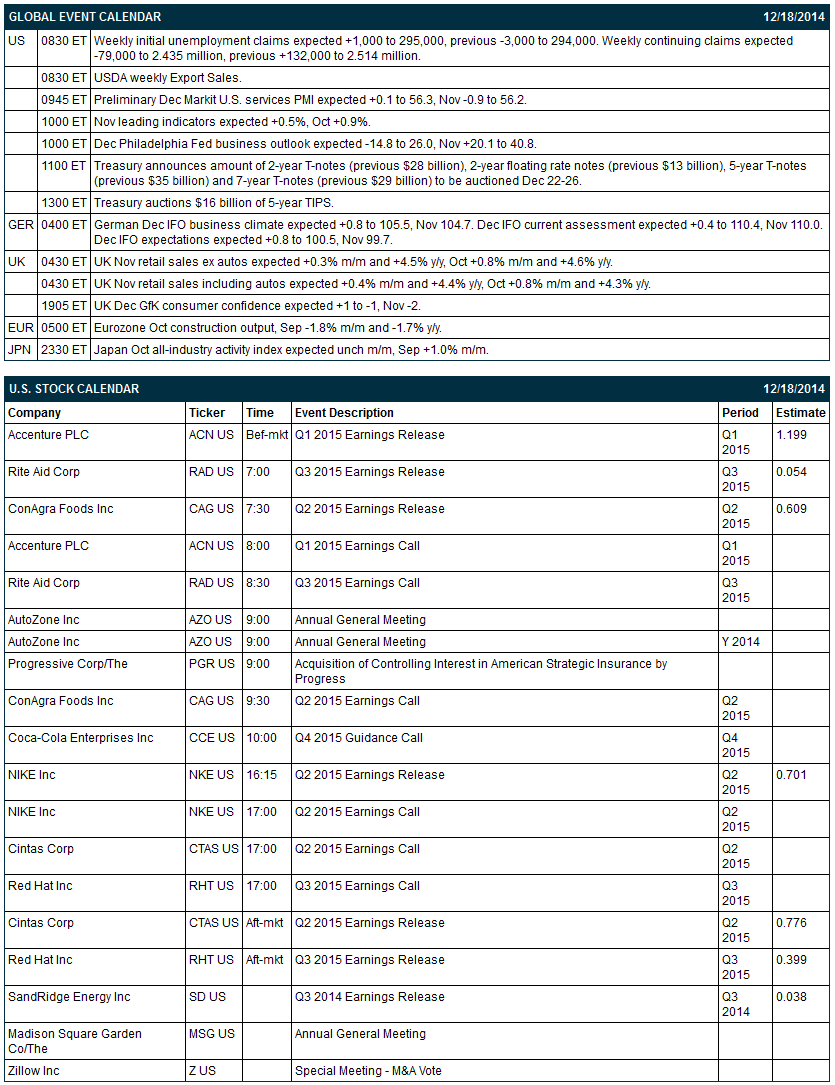

Today’s initial unemployment claims report is expected to show a small +1,000 increase to +295,000 and the continuing claims report is expected to show a -79,000 decline to 2.435 million. Today’s Nov leading indicators report is expected to show another solid increase of +0.5%, adding to the sharp increase of +0.9% seen in October. Today’s Dec Philadelphia Fed business outlook index is expected to show a sharp -14.8 point decline to 26.0. There are 7 of the Russell 1000 companies that report earnings today: Nike (consensus $0.70), Accenture (1.20), Rite Aid (0.05), ConAgra (0.61), Cintas (0.78), Red Hat (0.40), SandRidge Energy (0.04). There are no equity conferences today.

OVERNIGHT U.S. STOCK MOVERS

Rite Aid (RAD +4.30%) reported Q3 EPS of 10 cents, double consensus of 5 cents, and then raised guidance on fiscal 2015 EPS view to 31 cents-37cents, better than consensus of 31 cents.

Joy Global (JOY +0.20%) was upgraded to 'Neutral' from 'Underperform' at Longbow.

Starwood (HOT +1.01%) was initiated with a 'Buy' at Evercore ISI with a price target of $87.

Accenture PLC (ACN +2.93%) reported Q1 EPS of $1.29, higher than consensus of $1.20.

Exxon-Mobile (XOM +3.02%) climbed over 2% in pre-market trading as crude oil rose over +$1.00 a barrel.

Navistar (NAV +4.26%) gained over 2% in after-hours trading after activist investor Carl Icahn reported a 19.99% stake in the company.

AK Steel (AKS +6.11%) climbed over 5% in after-hours trading after it said it sees Q4 EPS of 5 cents-10 cents, above consensus of 4 cents.

Discover (DFS +3.31%) was initiated with a 'Buy' at Jefferies with a price target of $75.

Sally Beauty (SBH +2.11%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $37.

Tupperware Brands (TUP -0.02%) was initiated with an 'Overweight' at Piper Jaffray with a price target of $77.

Jabil Circuit (JBL +1.93%) jumped over 4% in after-hours trading after it reported Q1 core EPS of 55 cents, higher than consensus of 48 cents, and then raised guidance on fiscal 2015 core EPS view to $1.85-$2.15, above consensus of $1.79.

Herman Miller (MLHR +3.29%) slid 6% in after-hours trading after it reported Q2 EPS ex-items of 51 cents, below consensus of 52 cents.

Oracle (ORCL +1.30%) rose over 4% in after-hours trading after it reported Q2 EPS of 69 cents, beter than consensus of 68 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +1.15%) this morning are up +21.25 points (+1.06%). The S&P 500 index on Wednesday closed sharply higher: S&P 500 +2.04%, Dow Jones +1.69%, Nasdaq +1.85%. Bullish factors included (1) slack inflation pressures after U.S. Nov CPI fell -0.3% m/m, weaker than expectations of -0.1% m/m and the largest monthly decline in nearly 6 years, (2) strength in energy producers after crude oil rallied, and (3) the post-FOMC meeting statement that said the Fed will be “patient” in its approach to raising interest rates.

Mar 10-year T-notes (ZNH15 -0.21%) this morning are down -7.5 ticks. Mar 10-year T-note futures prices on Wednesday closed lower: TYH5 -22.00, FVH5 -15.00. Bearish factors included (1) the post-FOMC statement that said the labor market “improved further” and that “underutilization of labor resources continues to diminish,” which signals policy makers are a step closer to raising interest rates, and (2) reduced safe-haven demand after stocks rallied.

The dollar index (DXY00 -0.01%) this morning is down -0.089 (-0.10%). EUR/USD (^EURUSD) is down -0.0034 (-0.28% at a 1-week low. USD/JPY (^USDJPY) is down -0.02 (-0.02%). The dollar index on Wednesday posted a 1-week high and closed higher. Closes: Dollar index +1.008 (-0.38%), EUR/USD -0.01688 (-1.35%), USD/JPY +2.240 (+1.92%). Bullish factors included (1) the post-FOMC meeting statement that said the labor market “improved further,” which signals the Fed is closer to raising interest rates, and (2) weakness in EUR/USD on signs the ECB may soon expand stimulus after ECB Executive Board member Coeure said “there is a broad consensus on the ECB Governing Council to do more and we are now discussing the instruments to use.”

Jan WTI crude oil (CLF15 +3.22%) this morning is up +$1.31 (+2.32%) a barrel and Jan gasoline (RBF15 +3.23%) is up +0.0406 (+2.59%). Jan crude and Jan gasoline prices Wednesday closed higher. Closes: CLF5 +0.54 (+0.97%), RBF5 +0.0252 (+1.64%). The main bullish factor was fund short covering after prices failed to take out Tuesday’s 5-1/2 year lows. Negative factors included (1) the +5.25 million bbl surge in weekly EIA gasoline inventories to a 9-month high of 222 million bbl, three times more than expectations of +1.75 million bbl, and (2) the +2.92 million bbl increase in crude supplies at Cushing, OK, the delivery point of WTI futures, to an 8-1/2 month high of 27.8 million bbl.

Click on picture to enlarge

Disclosure: None