Morning Call For December 17, 2014

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.56%) this morning are up +0.61% ahead of the outcome of today's FOMC meeting, while European stocks are down-0.92%, led by a decline in bank stocks on concern of their exposure to Russian debt. The Russian ruble has stabilized temporarily near 66 per dollar, above yesterday's record low of near 80 per dollar, after Russian Economy Minister Ulyukayev denied speculation the government would impose restrictions to stop Russians from converting rubles into dollars. The ruble has plunged 52% against the dollar so far this year as the weight of international economic sanctions along with the plunge in crude to a 5-1/2 year low has decimated the ruble. Asian stocks closed mixed: Japan +0.38%, Hong Kong -0.37%, China +1.73%, Taiwan -1.37%, Australia +0.18%, Singapore +0.38%, South Korea -0.29%, India -0.27%. Chinese stocks closed higher and received a boost on speculation the government will expand stimulus after the PBOC rolled over a portion of a 3-month lending facility from September that was set to expire. Commodity prices are mixed. Jan crude oil (CLF15 -2.50%) is down -1.70% after Russian Energy Minister Novak said that the price of crude oil "will stabilize itself" and Russia will not cut crude production and will keep output steady near the current 10.6 million bpd. Jan gasoline (RBF15 -1.18%) is down -0.91%. Feb gold (GCG15 +0.39%) is up +0.54%. Mar copper (HGH15 -0.89%) is down -0.93% at a 2-week low. Agriculture prices are mixed. The dollar index (DXY00 +0.16%) is up +0.17%. EUR/USD (^EURUSD) is down -0.43%. USD/JPY (^USDJPY) is up +0.63%. Mar T-note prices (ZNH15 -0.17%) are down -5 ticks.

ECB Executive Board member Coeure said in an interview with the L'Opinion newspaper that "there is a broad consensus in the ECB Governing Council to do more and we are now discussing the instruments to use."

The Japan Nov trade balance widened to a deficit of -891.9 billion yen from a downward revised -736.9 billion yen deficit in Oct, a smaller deficit than expectations of -992.0 billion yen. Japan Nov exports rose +4.9% y/y, less than expectations of +7.0% y/y, and Jan imports unexpectedly fell -1.7% y/y, weaker than expectations of +1.6% y/y and the biggest decline in 6 months.

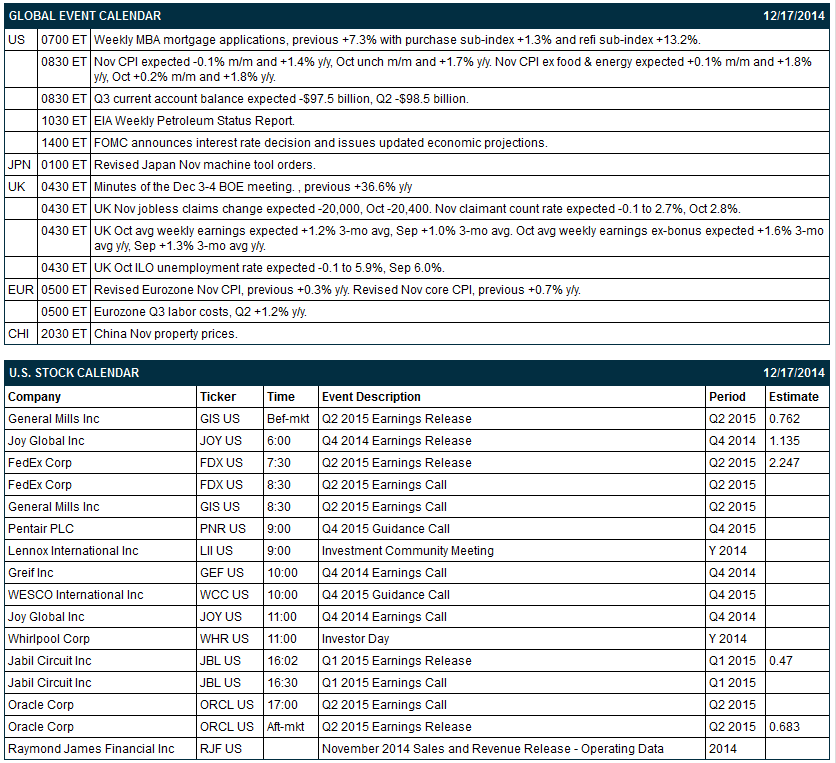

Eurozone Q3 labor costs rose +1.3% y/y, a smaller increase than the upward revised +1.4% y/y from Q2.

The UK Nov jobless claims fell -26,900, more than expectations of -20,000. The Nov claimant count rate fell -0.1 to 2.7%, right on expectations and the lowest in 6-1/3 years.

UK Oct avg weekly earnings rose +1.4%3-mo avg, better than expectations of +1.2% 3-mo avg and the most in 7 months. Oct avg weekly earnings ex-bonus rose +1.6% 3-mo avg, right on expectations and the most in 2 years.

U.S. STOCK PREVIEW

The 2-day FOMC meeting concludes today. Today's headline Nov CPI is expected to fall to +1.4% y/y from +1.7% in October. Excluding food and energy, however, today’s Nov core CPI is expected to be unchanged from October at +1.8% y/y. Today’s Q3 current account deficit is expected to narrow slightly to -$97.5 billion from -$98.5 billion in Q2. There are 5 of the Russell 1000 companies that report earnings today: Oracle (consensus $0.68), General Mills ($0.76), Joy Global (1.14), FedEx (2.25), Jabil Circuit (0.47). Equity conferences today include: Sanford C. Bernstein Technology Innovation Summit on Tue-Wed.

OVERNIGHT U.S. STOCK MOVERS

General Mills (GIS -0.66%) reported Q2 EPS of 80 cents, better than consensus of 76 cents.

FedEx (FDX -1.14%) reported Q2 EPS of $2.14, below consensus of $2.22.

JPMorgan Chase keeps an 'Overweight' rating on CVS Health (CVS +2.72%) and raises the price target on the stock to $108 from $92.

Consolidated Edison (ED +0.14%) was downgraded to 'Sell' from 'Hold' at Deutsche Bank.

PG&E (PCG -0.76%) was downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Joy Global (JOY +0.30%) reported Q4 EPS of $1.25, higher than consensus of $1.14.

Northrop Grumman (NOC +1.33%) was awarded a $657.4 million government contract that will provide the Republic of Korea four RQ-4B Block 30 Global Hawk air vehicles, two spare engines, and the applicable Ground Control Environment elements.

GIC Private reported a 7.07% passive stake in UBS (UBS +0.23%) .

Colfax (CFX -1.52%) lowered guidance on fuscal 2015 EPS to $2.20-$2.40, below consensus of $2.58 and said it sees fiscal 2015 revenue of $4.53 billiob-$4.68 billion, less than consensus of $4.8 billion.

Gabelli reported an 11.09% stake in Griffin (GRIF +1.16%) .

Thermo Fisher (TMO -1.76%) was initiated with a 'Buy' at KeyBanc with a price target of $144.

Ruby Tuesday (RT -1.10%) reported Q2 company-owned Same-Store-Sales down 1%, weaker than same-store-sales guidance provided on October 8 of up 1%-2% for Q2.

Darden Restaurants (DRI -2.26%) rose over 1% in after-hours trading after it reported Q2 EPS of 28 cents, better than consensus of 27 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +0.56%) this morning are up +12.00 points (+0.61%). The S&P 500 index on Tuesday fell to a 1-1/2 month low and closed lower: S&P 500 -0.85%, Dow Jones -0.65%, Nasdaq -1.63%. Bearish factors included (1) Chinese economic concerns after the China Dec HSBC manufacturing PMI fell -0.5 to a 7-month low of 49.5, weaker than expectations of -0.2 to 49.8, (2) the unexpected -1.6% decline in U.S. Nov housing starts to 1.028 million, and (3) the ongoing meltdown in the ruble and fears that a Russian financial crisis could spread into Europe and the U.S. A positive factor was a rally in energy producers after crude oil recovered from a 5-1/2 year low and closed slightly higher.

Mar 10-year T-notes (ZNH15 -0.17%) this morning are down -5 ticks. Mar 10-year T-note futures prices on Tuesday posted a 2-month high: TYH5 +12.50, FVH5 +9.00. Bullish factors included (1) the fall in crude oil to a 5-1/2 year low, which prompted the 10-year breakeven inflation expectations rate to fall to a 4-1/4 year low, and (2) increased safe-haven demand from financial turmoil in Russia after the Russian ruble sank to a record low of 79 per dollar.

The dollar index (DXY00 +0.16%) this morning is up +0.154 (+0.17%). EUR/USD (^EURUSD) is down -0.0054 (-0.43%). USD/JPY (^USDJPY) is up +0.73 (+0.63%). The dollar index on Tuesday fell to a 2-week low and closed lower. Closes: Dollar index -0.335 (-0.38%), EUR/USD +0.00739 (+0.59%), USD/JPY -1.427 (-1.20%). Bearish factors included (1) strength in EUR/USD which rallied to a 3-week high after German Dec ZEW survey expectations of economic growth rose to an 8-month high and after Eurozone Dec Markit manufacturing PMI rose to its best level in 5 months, and (2) the fall in USD/JPY fell to a 4-week low after a slide in global stocks boosted the safe-haven demand for the yen.

Jan WTI crude oil (CLF15 -2.50%) this morning is down -95 cents (-1.70%) and Jan gasoline (RBF15 -1.18%) is down -0.0140 (-0.91%). Jan crude and Jan gasoline prices Tuesday posted new 5-1/2 year lows but recovered and settled mixed. Closes: CLF5 +0.02 (+0.04%), RBF5 -0.0393 (-2.49%). Supportive factors included (1) the slide in the dollar index to a 2-week low, and (2) expectations for weekly EIA crude stockpiles on Wednesday to fall-2.65 million bbl. The main bearish factor centers on signs of ample global crude supplies amid expectations that OPEC will refrain from cutting production.

Disclosure: None