Morning Call For December 11, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.17%) this morning are up +0.10% as energy producers gained in pre-market trading after the price of crude oil rose from a 5-1/3 year low. U.S. stocks also found support on expectations that today's data on U.S. Nov retail sales will be positive. European stocks are down -0.15% after mining companies fell with Anglo American Plc down more than 2% to a 5-year low and Glencore Plc down over 3%. The 10-year German bund yield fell to a record low of 0.656% on speculation the ECB will have to revert to large-scale quantitative easing after the ECB's second round of targeted loans to Eurozone banks fell short of expectations. The Bank of Russia raised its key interest rate by +1.0 point to 10.5% from 9.5%, although that failed to stop the slide in the ruble which fell to a record low of 55.4747 per dollar, Asian stocks closed lower: Japan -0.89%, Hong Kong-0.90%, China -1.20%, Taiwan -0.21%, Australia -0.53%, Singapore -0.21%, South Korea -1.53%, India -0.82%. Commodity prices are mixed. Jan crude oil (CLF15 +0.77%) is up +1.10%. Jan gasoline (RBF15 +0.61%) is up +1.03%. Feb gold (GCG15 -0.36%) is down -0.54%. Mar copper (HGH15+0.33%) is up +0.41%. Agriculture prices are mixed. The dollar index (DXY00 -0.12%) is down -0.05%. EUR/USD (^EURUSD) is up +0.10%. USD/JPY (^USDJPY) is up +0.45%. Mar T-note prices (ZNH15 +0.18%) are up +5 ticks at a 1-week high on carry-over support from a rally in 10-year German bunds to an all-time high.

The ECB allotted 130 billion euros ($161 billion) to Eurozone banks at a fixed interest rate of 0.15% in its second round of targeted longer-term refinancing operations (TLTROs). That was below market expectations of 148 billion euros in TLTROs and bolsters the case for the ECB to start large-scale quantitative easing.

The German Nov CPI (EU harmonized) was left unrevised at unch m/m and +0.5% y/y.

Japan Oct machine orders fell -6.4% m/m and -4.9% y/y, a larger drop than expectations of -1.7% m/m and -0.3% y/y and the biggest decline in 5 months.

The Japan Oct tertiary industry index fell -0.2% m/m, right on expectations and Sep was revised higher to +1.3% m/m from the originally reported +1.0% m/m.

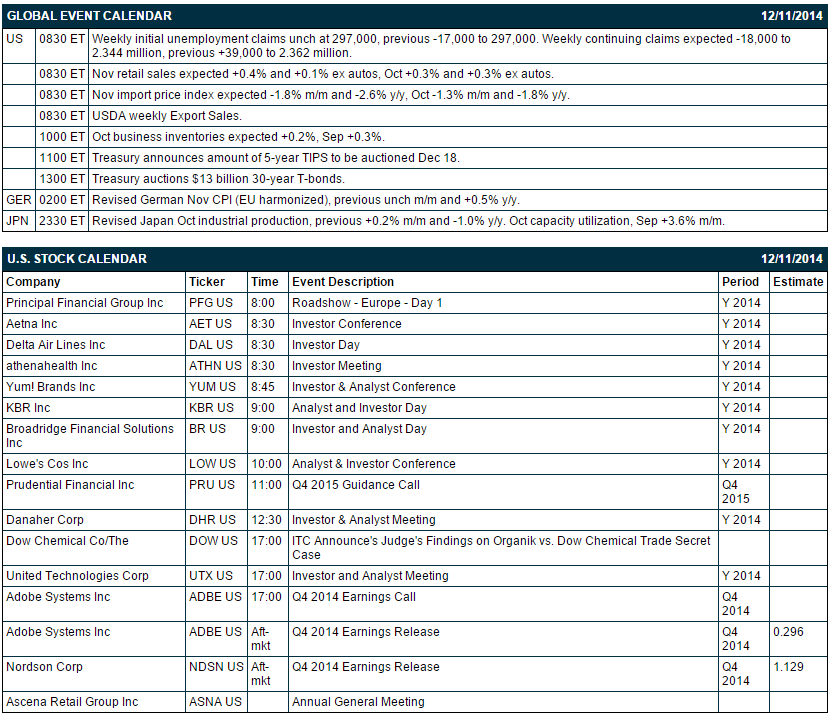

U.S. STOCK PREVIEW

Today's weekly initial unemployment claims report is expected to be unchanged at 297,000 following last week's decline of -17,000 to 297,000. Today's continuing claims report is expected to show a decline of -18,000 to 2.344 million, reversing part of last week's +39,000 increase to 2.362 million. Today’s Nov retail sales report is expected to show a firm overall increase of +0.4%, adding to the +0.3% increase seen in October. The Treasury today will sell $13 billion of 30-year T-bonds

There are 2 of the Russell 1000 companies that report earnings today: Adobe Systems (consensus $0.30), Nordson (1.13). Equity conferences during the remainder of this week include: Bank of America Merrill Lynch US Basic Materials Conference on Wed-Thu, Capital One Southcoast Energy Conference on Wed-Thu, Bank of America Merrill Lynch Animal & Dental Health Summit on Thu, and Desjardins Securities Materials Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM -2.83%) was upgraded to 'Outperform' from 'Underperform' at CLSA.

Eli Lilly (LLY -1.61%) was upgraded to 'Overweight' from 'Underweight' at Morgan Stanley.

RadioShack (RSH -3.51%) reported a Q3 EPS loss of -$1.58, a much bigger loss than consensus of -$1.04.

Travelers (TRV -0.72%) was downgraded to 'Neutral' from 'Buy' at UBS.

Starboard Value reported a 5.1% stake in Staples (SPLS +2.42%) .

Toll Brothers (TOL -7.85%) was downgraded to 'Underperform' from 'Sector Perform' at RBC Capital.

Janus Capital reported a 10.6% passive stake in Rexnord (RXN -4.07%) .

Lowe's (LOW -1.08%) said it sees fiscal 2014 EPS about $2.68, better than consensus of $2.67.

lululemon (LULU -2.16%) reported Q3 EPS of 42 cents, better than consensus of 38 cents.

Burlington Stores (BURL +0.50%) fell over 1% in after-hours trading after it filed to sell 8 million shares of common stock for its holders.

According to the WSJ, ebay (EBAY -0.23%) is considering a plan to eliminate at least 3,000 jobs, or 10% of its total work force, early next year as the company gets ready to separate its PayPal payments unit.

Men's Wearhouse (MW -3.39%) reported Q3 adjusted EPS of 83 cents, less than consensus of 87 cents.

Third Avenue reported a 3.11% passive stake in Covanta (CVA -1.67%) .

Casey's General Stores (CASY -1.16%) rose nearly 2% in after-hours trading after it reported Q2 EPS of $1.28, higher than consensus of $1.17.

Restoration Hardware (RH -0.25%) jumped over 5% in after-hours trading after it reported Q3 adjusted EPS of 49 cents, better than consensus of 48 cents, and then raised guidance on fiscal 2014 adjusted EPS view to $2.33-$2.35 from $2.29-$2.33, above consensus of $2.33.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.17%) this morning are up +2.00 points (+0.10%). The S&P 500 index on Wednesday fell to a 1-month low and closed lower: S&P 500 -1.64%, Dow Jones -1.51%, Nasdaq -1.63%. Bearish factors included (1) a slide in energy producers after crude oil prices slid to a 5-1/3 year low, (2) Chinese growth concerns after China Nov CPI eased to a 5-year low of +1.4% y/y, less than expectations of +1.6% y/y, and (3) weakness in financial stocks led by a drop in JPMorgan Chase which fell after it said it expects a year-on-year percentage drop in the “high teens” in Q4 trading revenue.

Mar 10-year T-notes (ZNH15 +0.18%) this morning are up +5 ticks at a 1-week high. Mar 10-year T-note futures prices on Wednesday rose to a 1-week high and closed higher: TYH5 +16.00, FVH5 +9.75. Bullish factors included (1) carry-over support from a rally in German bunds to a record high on speculation the ECB will implement QE as soon as next month, and (2) increased safe-haven demand for Treasuries after stocks moved lower.

The dollar index (DXY00 -0.12%) this morning is down -0.044 (-0.05%). EUR/USD (^EURUSD) is up +0.0012 (+0.10%). USD/JPY (^USDJPY) is up +0.53 (+0.45%). The dollar index on Wednesday closed lower. Closes: Dollar index -0.419 (-0.47%), EUR/USD +0.00737 (+0.60%), USD/JPY -1.879(-1.57%). The main bearish factor was weakness in USD/JPY as a drop in stocks boosted safe-haven demand for the yen. Strength in EUR/USD was limited as speculation was bolstered that the ECB will boost stimulus after ECB Executive Board member Coeure said there are “risks, substantial risks” from inflation being too low for too long.

Jan WTI crude oil (CLF15 +0.77%) this morning is up +67 cents (+1.10%) and Jan gasoline (RBF15 +0.61%) is up +0.0169 (+1.03%). Jan crude and Jan gasoline prices plummeted Wednesday with Jan crude at a 5-1/3 year low and Jan gasoline at a 5-year low. Closes: CLF5 -2.88 (-4.51%), RBF5-0.0781 (-4.53%). Bearish factors included (1) the unexpected +1.45 million bbl increase in weekly EIA crude inventories, more than expectations of a-2.7 million bbl draw, (2) the +8.2 million bbl surge in EIA gasoline stockpiles to a 4-month high of 216.76 million bbl vs expectations of +2.5 million bbl, and (3) the +1.02 million bbl increase in crude supplies at Cushing, OK, the delivery point for WTI futures, to a 7-1/2 month high.

Disclosure: None