Morning Call For August 7, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 -0.17%) are down -0.10% and European stocks are down -0.38% ahead of monthly U.S. payroll data for July that may give clues to the pace and timing of a Fed interest rate increase. European stocks also fell after German Jun industrial production unexpectedly declined at the fastest pace in 10 months. Miners and basic-resource companies also fell after the price of copper (HGU15 -0.21%) slid to a fresh 6-year low. Asian stocks closed mixed: Japan +0.29%, Hong Kong +0.73%, China +2.26%, Taiwan -0.09%, Australia -2.41%, South Korea -0.10%, India -0.22%. Japanese stocks closed higher after the BOJ maintained its overly easy monetary policies following today's 2-day meeting, while China's Shanghai Composite closed up over 2% on speculation the Chinese government will take more measures to stabilize the equity market.

The dollar index (DXY00 -0.06%) is down -0.02%. EUR/USD (^EURUSD) is up +0.03%. USD/JPY (^USDJPY) is down -0.02%.

Sep T-note prices (ZNU15 +0.06%) are up +1.5 ticks.

According to people with knowledge of the matter, the China Securities Finance Corp., the government agency mandated to buy equities to support the market, is seeking to increase its funding by an additional 2 trillion yuan ($322 billion). The extra funding would add to the 3 trillion yuan already made available by the government.

German Jun industrial production unexpectedly fell -1.4% m/m, weaker than expectations of +0.3% m/m and the largest decline in 10 months. Onan annual basis, Jun industrial production rose +0.6% y/y, weaker than expectations of +2.2% y/y.

U.S. STOCK PREVIEW

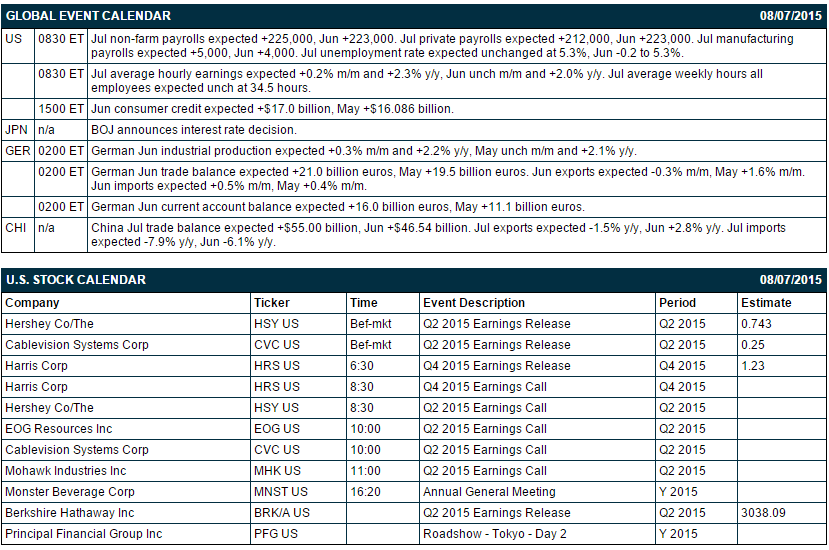

Key U.S. news today includes: (1) July non-farm payrolls (expected +225,000, Jun +223,000) and Jul unemployment rate (expected unchanged at 5.3%, Jun -0.2 to 5.3%), and (2) Jun consumer credit (expected +$17.0 billion, May +$16.086 billion).

There are 4 of the S&P 500 companies that report earnings today: Hershey (consensus $0.74), Cablevision (0.25), Harris Corp (1.23), Berkshire Hathaway (3038).

U.S. IPO's scheduled to price today include: Pixelworks (PXLW).

Equity conferences during the remainder of this week include: none.

OVERNIGHT U.S. STOCK MOVERS

Intel (INTC -0.38%) was downgraded to 'Hold' from 'Buy' at Drexel Hamilton.

Coach (COH -0.54%) was upgraded to 'Buy' from 'Neutral' at UBS.

Hershey (HSY -0.50%) reported Q2 EPS of 78 cents, better than consensus of 74 cents.

Genesis Healthcare (GEN +1.52%) reported Q2 EPS of 14 cents, higher than consensus of 9 cents.

Billionaire investor Carl Icahn reported an 8.18% stake in Cheniere (LNG -0.26%) .

Bio-Rad (BIO -2.98%) reported Q2 EPS of 97 cents, well above consensus of 78 cents.

Nu Skin (NUS -3.62%) reported Q2 EPS of 75 cents, better than consensus of 72 cents.

Sprouts Farmers Markets (SFM -2.21%) fell over 4% in after-hours trading after it reported Q2 adjusted EPS of 22 cents, right on consensus, but then lowered guidance on fiscal 2015 adjusted EPS to 80 cents-82 cents, below consensus of 85 cents.

TESARO (TSRO -5.95%) reported a Q2 EPS loss of -$1.51, a wider loss than consensus of -$1.14.

NVIDIA (NVDA -0.63%) jumped over 8% in after-hours trading after it reported Q2 EPS of 34 cents, over three times consensus of 10 cents.

Monster Beverage (MNST -5.93%) reported Q2 adjusted EPS of 79 cents, weaker than consensus of 91 cents.

EOG Resources (EOG +2.09%) reported Q2 adjusted EPS of 28 cents, well above consensus of 10 cents.

Mohawk (MHK -2.53%) reported Q2 EPS of $2.69, better than consensus of $2.62.

Century Aluminum (CENX -1.08%) reported Q2 adjusted EPS of 25 cents, below consensus of 27 cents.

Nuance (NUAN -1.59%) reported Q3 EPS of 32 cents, higher than consensus of 29 cents, and then raised guidance on fiscal 2015 EPS to $1.20-$1.24, above consensus of $1.19.

MARKET COMMENTS

Sep E-mini S&Ps (ESU15 -0.17%) this morning are down -2.00 points (-0.10%). Closes: S&P 500 -0.78%, Dow Jones -0.69%, Nasdaq -1.60%. The S&P 500 Thursday fell to a 1-week low and closed lower on a slide in media stocks on disappointing Q2 earnings results from Viacom and Twenty-First Century Fox, weakness in energy producers after crude oil tumbled to a 4-1/2 month low, and long liquidation ahead of Friday's monthly U.S. payrolls report.

Sep 10-year T-note prices (ZNU15 +0.06%) this morning are up +1.5 ticks. Closes: TYU5 +8.5, FVU5 +4.50. Sep T-note prices on Thursday closed higher on a decline in the 10-year inflation expectations rate to a 4-1/2 month low due to the continued drop in oil prices and on increased safe-haven demand for T-notes after the S&P 500 fell to a 1-week low.

The dollar index (DXY00 -0.06%) this morning is down -0.017 (-0.02%). EUR/USD (^EURUSD) is up +0.0003 (+0.03%). USD/JPY (^USDJPY) is down-0.02 (-0.02%). Closes: Dollar Index -0.125 (-0.13%), EUR/USD +0.00189 (+0.17%), USD/JPY -0.121 (-0.10%). The dollar index on Thursday closed lower on strength in EUR/USD after German Jun factory orders rose more than expected, and on long liquidation in the dollar ahead of Friday's U.S. payroll report.

Sep crude oil (CLU15 -0.11%) this morning is up +3 cents (+0.07%) and Sep gasoline (RBU15 -0.81%) is down -0.0078 (-0.47%). Closes: CLU5 -0.40(-0.89%), RBU5 -0.0215 (-1.29%). Sep crude oil and gasoline closed lower Thursday with Sep crude at a 4-1/2 month low and Sep gasoline at a 5-1/2 month low. Negative factors included carry-over bearishness from Wednesday's EIA report that showed an unexpected +811,000 bbl increase in weekly EIA gasoline inventories (vs expectations of -200,000 bbl) and a +709,000 bbl increase in EIA distillate inventories to a 3-1/2 year high. Crude oil prices also saw weakness after Goldman Sachs said the global crude oversupply is currently 2 million bpd and that world oil storage may be filled by autumn.

Disclosure: None.