Morning Call For August 30, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.03%) are little changed, down -0.01%, as a nearly 2% loss in Apple in pre-market trading limits the upside in U.S. stocks. Apple retreated after it was ordered to pay back $14.5 billion when the European Commission said Ireland illegally slashed Apple's tax bill. European stocks are up +0.85% at a 2-week high led by gains in bank stocks and with strength in European exporters as EUR/USD tumbled to a 2-week low. Gains in European equities were limited as mining stocks fell after the price of copper (HGU16 +0.17%) dropped -0.02% to a 2-1/4 month low. Asian stocks settled mostly higher: Japan -0.07%, Hong Kong +0.55%, China +0.15%, Taiwan unch, Australia +0.17%, Singapore -0.04%, South Korea +0.39%, India +1.59%. Japanese stocks closed lower, despite a rally in USD/JPY to a 3-week high, after stronger-than-expected data on consumer spending and the labor market reduced the chances of additional BOJ easing.

The dollar index (DXY00 +0.20%) is up +0.22% at a 2-week high. EUR/USD (^EURUSD) is down -0.20% at a 2-week low. USD/JPY (^USDJPY) is up +0.43% at a 3-week high.

Sep T-note prices (ZNU16 -0.07%) are down -3.5 ticks on hawkish comments from Fed Vice Chair Fischer who said next month's interest rate decision by the FOMC is not necessarily "one and done."

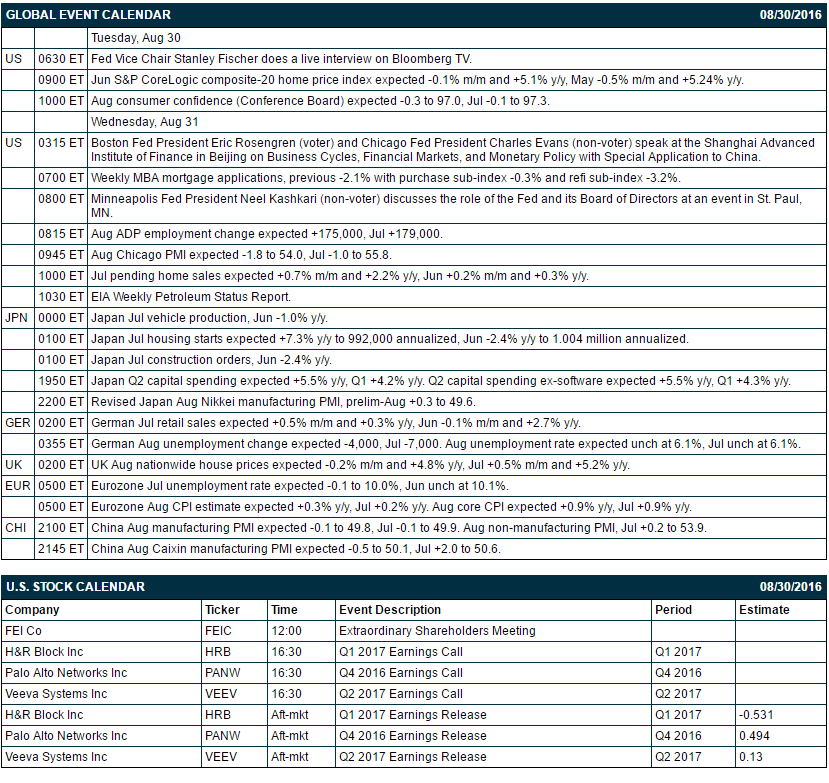

Fed Vice Chair Fischer said the U.S. is close to full employment and that next month's interest rate decision is not necessarily "one and done." He added that the Fed "can choose the pace" of rate increases based on the economic data.

Eurozone Aug economic confidence fell -1.0 to 103.5, weaker than expectations of -0.5 to 104.1 and the lowest in 5 months.

The Japan Jul jobless rate unexpectedly fell -0.1 to 3.0%, stronger than expectations of no change at 3.1% and the lowest in 21 years.

Japan Jul retail sales of +1.4% m/m and -0.2% y/y was stronger than expectations of +0.8% m/m and -0.9% y/y.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Fed Vice Chair Stanley Fischer does a live interview on Bloomberg TV, (2) Jun S&P CoreLogic composite-20 home price index (expected -0.1% m/m and +5.1% y/y, May -0.5% m/m and +5.24% y/y), (3) Aug consumer confidence from the Conference Board (expected-0.3 to 97.0, Jul -0.1 to 97.3).

Russell 1000 companies that report earnings today: H&R Block (consensus -$0.53), Palo Alto Networks (0.49), Veeva Systems (0.13).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week include: European Society of Cardiolog Meeting on Mon-Tue, 2016 Farm Progress Show on Mon-Wed, Longbow Industrial Manufacturing & Technology Conference on Tue, Simmons European Energy Conference on Tue-Wed, Jefferies LLC Semiconductor, Hardware and Communications Infrastructure Summit on Wed.

OVERNIGHT U.S. STOCK MOVERS

Apple (AAPL -0.11%) is down nearly 2% in pre-market trading after it was ordered to pay 13 billion euros ($14.5 billion) plus interest as the European Commission said Ireland illegally cut Apple's tax bill.

First Data Corp. (FDC -0.38%) was rated a new 'Buy' at Craig Hallum with a 12-month price target of $20.

VMware (VMW +1.32%) was upgraded to 'Buy' from 'Neutral' at SunTrust Robinson Humphrey with a 12-month price target of $92.

Rackspace Hosting (RAX -0.13%) was downgraded to 'Underperform' from 'Outperform' at Raymond James.

Coeur Mining (CDE +1.10%) was upgraded to 'Sector Perform' from 'Sector Underperform' at CIBC.

Flextronics International (FLEX +1.00%) rose over 1% in after-hours trading after its board authorized a buyback of up to $500 million in company stock.

Catalent (CTLT +0.36%) slid almost 5% in after-hours trading after it reported Q4 adjusted EPS of 52 cents, below consensus of 53 cents.

Skyworks Solutions (SWKS +0.51%) dropped 2% in after-hours trading after CFO Donald Palette retired and was replaced by Kris Sennesael.

American Airlines Group (AAL -0.17%) lost 1% and United Continental Holdings (UAL +0.17%) gained over 1% in after-hours trading after American Airlines president Scott Kirby left the company for the same role at United Continental.

ScanSource (SCSC +1.18%) slumped over 12% in after-hours trading after it reported Q4 adjusted EPS of 51 cents, well below consensus of 71 cents, and said it sees Q1 adjusted EPS of 60 cents-68 cents, weaker than consensus of 75 cents.

Phibro Animal Health (PAHC +3.19%) gained almost 1% in after-hours trading after it reported Q4 adjusted EPS of 40 cents, higher than consensus of 38 cents.

Hershey (HSY +0.71%) tumbled over 10% and Mondelez International ({=MDLZ rose over 3% in after-hours trading after Mondelez International said it is no longer seeking a merger with Hershey.

Syros Pharmaceuticals (SYRS -0.43%) surged over 18% in after-hours trading after it said its research published in the scientific journal Nature Chemical Biology shows a promising approach to treating several cancers through its CDK12 and CDK 13 inhibitors.

MARKET COMMENTS

Sep E-mini S&Ps (ESU16 -0.03%) this morning are down -0.25 of a point (-0.01%). Monday's closes: S&P 500 +0.52%, Dow Jones +0.58%, Nasdaq +0.15%. The S&P 500 on Monday closed higher on carryover support from a sharp +2.3% rally in Japanese stocks on speculation the BOJ may expand stimulus after BOJ Governor Kuroda said the BOJ "will act decisively as we move on." The market was also pleased with the as-expected increases of +0.3% in U.S. Jul personal spending and +0.4% in Jul personal income, which bolstered confidence in the economic outlook.

Sep 10-year T-notes (ZNU16 -0.07%) this morning are down -3.5 ticks. Monday's closes: TYU6 +18.50, FVU6 +10.50. Sep T-notes on Monday rebounded from a 1-month low and closed higher on benign price pressures after the July core PCE rose +1.6% y/y, below the Fed's 2.0% target, and on the weaker-than-expected Aug Dallas Fed manufacturing index of -4.9 to -6.2 (vs expectations of -2.6 to -2.9).

The dollar index (DXY00 +0.20%) this morning is up +0.207 (+0.22%) at a 2-week high. EUR/USD (^EURUSD) is down -0.0022 (-0.20%) at a 2-week low. USD/JPY (^USDJPY) is up +0.44 (+0.43%) at a 3-week high. Monday's closes: Dollar index +0.014 (+0.01%), EUR/USD -0.0009 (-0.08%), USD/JPY +0.08 (+0.08%). The dollar index on Monday climbed to a 2-week high but fell back and settled little changed. The dollar was boosted by carryover support from last Friday's comments from Fed Chair Yellen and Fed Vice Chair Fischer that boosted the odds for a Fed rate hike this year. In addition, USD/JPY rallied to a 2-1/2 week high after BOJ Governor Kuroda said there's "ample space for additional easing" and that the BOJ will bolster stimulus "without hesitation" if warranted. The dollar was undercut by the decline in the Aug Dallas Fed manufacturing index.

Oct crude oil (CLV16 +0.68%) this morning is up +32 cents (+0.68%) and Oct gasoline (RBV16 -0.16%) is down -0.0053 (-0.38%). Monday's closes: CLV6 -0.66 (-1.39%), RBV6 -0.0326 (-2.28%). Oct crude oil and gasoline on Monday closed lower on the rally in the dollar index to a 2-week high and on doubts about whether OPEC will be able to agree on a production freeze at next month's informal meeting in Algiers after Iranian Oil Minister Bijan Zanganeh said that while Iran supports action to stabilize the oil market, it won't participate in a freeze in output before regaining its pre-sanction share of OPEC production.

Disclosure: None.