Morning Call For August 24, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 +0.05%) are up +0.09% and European stocks are up +0.60% as the markets await Fed Chair Yellen's speech Friday from Jackson Hole, Wyoming, for clues as to when the Fed may raise interest rates. A rally in European bank stocks is leading the overall market higher, although gains were limited as mining stocks and energy producers weakened after crude oil and copper sold-off on signs of rising inventories. Oct WTI crude oil (CLV16 -1.87%) is down -1.64% and Sep COMEX copper (HGU16 -0.59%) is down -0.45% at a 2-month low. API data late Tuesday showed U.S. crude inventories rose 4.46 million bbl last week and LME data today showed LME copper inventories jumped +14,625 MT to a 9-month high of 254,700 MT. LME copper inventories have now surged by 24% over the past week. Asian stocks settled mixed: Japan +0.61%, Hong Kong -0.77%, China -0.12%, Taiwan -0.15%, Australia +0.14%, Singapore +0.67%, South Korea -0.43%, India +0.25%.

The dollar index (DXY00 +0.12%) is up +0.12%. EUR/USD (^EURUSD) is down -0.26%. USD/JPY (^USDJPY) is unchanged.

Sep T-note prices (ZNU16 unch) are little changed, down -0.5 of a tick.

U.S. STOCK PREVIEW

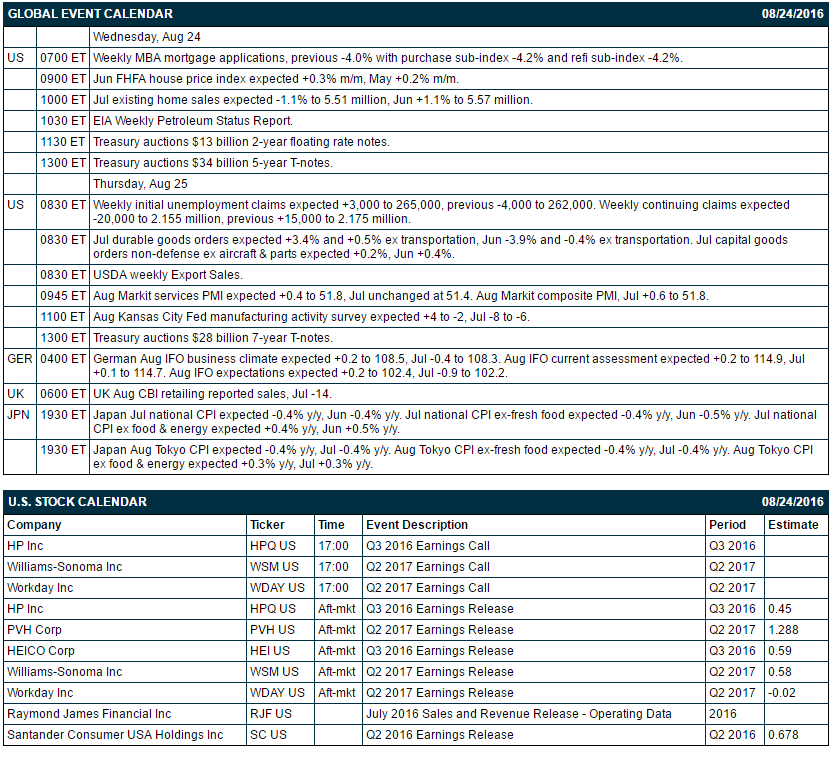

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -4.0% with purchase sub-index -4.2% and refi sub-index -4.2%), (2) Jun FHFA house price index (expected +0.3% m/m, May +0.2% m/m), (3) Jul existing home sales (expected -1.1% to 5.51 million, Jun +1.1% to 5.57 million), (4) Treasury's auction of $13 billion of 2-year floating rate notes, (5) Treasury's auction of $34 billion of 5-year T-notes, and (6) EIA Weekly Petroleum Status Report.

Russell 1000 companies that report earnings today: HP (consensus $0.45), PVH (1.29), HEICO (0.59), Williams Sonoma (0.58), Workday (-0.02), Santander Consumer USA Holdings (0.68).

U.S. IPO's scheduled to price today: none.

Equity conferences this week: Heikkinen Energy Conference 2016 on Wed

OVERNIGHT U.S. STOCK MOVERS

Garmin Ltd. (GRMN +0.96%) was downgraded to 'Sell' from 'Neutral' at Goldman Sachs.

CST Brands (CST +0.30%) was downgraded to 'Market Perform' from 'Outperform' at Wells Fargo.

SEACOR Holdings (CKH +0.88%) was rated a new 'Buy' at Stifel with a 12-month price target of $70.

Dycom Industries (DY +0.70%) dropped 4% in after-hours trading after it said the recently acquired operations of Goodman Networks is now expected to produce lower revenue in fiscal 2017 than initially anticipated.

Lannett (LCI +2.83%) surged nearly 15% in after-hours trading after it reported Q4 adjusted EPS of 73 cents, well above consensus of 59 cents, and then raised its fiscal 2017 revenue estimate to $690 million-$700 million from a prior view of $665.4 million.

Intuit (INTU +1.16%) fell over 4% in pre-market trading after it said that it sees Q1 revenue of $740 million-$760 million, below consensus of $771.9 million.

Wabash National (WNC +0.89%) climbed over 2% in after-hours trading after it was announced that it will replace Enersys in the S&P SmallCap 600 after the close of trading on Thursday, August 25.

OraSure Technologies (OSUR +0.14%) jumped over 9% in after-hours trading after it said it received a 6-year contract worth up to $16.6 million from the U.S. Department of Health and Human Services to advance the company's rapid Zika tests.

La-Z-Boy (LZB +3.59%) tumbled 15% in after-hours trading after it reported Q1 EPS of 28 cents, weaker than consensus of 29 cents.

Nimble Storage (NMBL +1.73%) gained over 2% in after-hours trading after it reported a Q2 adjusted loss of 018 cents, a smaller loss than consensus of-20 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU16 +0.05%) this morning are up +2.00 ponts (+0.09%). Tuesday's closes: S&P 500 +0.20%, Dow Jones +0.10%, Nasdaq +0.21%. The S&P 500 on Tuesday rallied to a 1-week high and closed higher on optimism about the U.S. economic outlook after July new home sales jumped +12.4% to an 8-3/4 year high of 654,000. Stocks were also boosted by a rally in energy producers after a +1.46% rally in crude oil. Stocks were undercut by the -0.8 point decline in U.S. Aug Markit manufacturing PMI to 52.1, weaker than expectations of -0.3 to 52.6.

Sep 10-year T-notes (ZNU16 unch) this morning are down -0.5 of a tick. Tuesday's closes: TYU6 -2.00, FVU6 -1.75. Sep T-notes on Tuesday closed lower on reduced safe-haven demand with the rally in stocks and the jump in U.S. Jul new home sales to their highest level in 8-3/4 years, which bolsters the case for the Fed to raise interest rates. T-notes were also pressured by the Treasury's auction of $101 billion of T-notes and floating rate notes this week.

The dollar index (DXY00 +0.12%) this morning is up +0.111 (+0.12%). EUR/USD (^EURUSD) is down -0.0029 (-0.26%). USD/JPY (^USDJPY) is unch. Tuesday's closes: Dollar index +0.020 (+0.02%), EUR/USD -0.0015 (-0.13%), USD/JPY -0.09 (-0.09%). The dollar index on Tuesday closed slightly higher on the jump in U.S. July new home sales to their highest level in 8-3/4 years. In addition, there was weakness in EUR/USD after Eurozone Aug consumer confidence fell more than expected. The dollar was undercut by the weaker-than-expected U.S. Aug Markit manufacturing PMI report.

Oct crude oil (CLV16 -1.87%) this morning is down -79 cents (-1.64%) and Oct gasoline (RBV16 -0.89%) is down -0.0103 (-0.73%). Tuesday's closes: CLV6 +0.69 (+1.46%), RBV6 +0.0150 (+1.07%). Oct crude oil and gasoline on Tuesday erased early losses and closed higher on a Reuters report saying that Iran is sending "positive signals" that it may support an OPEC initiative to freeze oil production. Crude oil prices were also boosted by expectations for Wednesday's weekly EIA data to show that crude inventories fell by -850,000 bbl.

Disclosure: None.