Morning Call For August 11, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 -0.54%) are down -0.36% and European stocks are down -1.10% after China unexpectedly devalued the yuan by 1.9%, the most in two decades, which sparked a sell-off in emerging-market currencies, commodities and stocks with exposure to China. The move by the PBOC risks starting a currency war as global demand wanes and fuels speculation that central banks, including the Fed, will keep interest rates lower for longer. European stocks were also undercut after German Aug ZEW investor confidence unexpectedly fell to its lowest in 9 months. Asian stocks closed lower: Japan -0.42%, Hong Kong -0.09%, China -0.01%, Taiwan -0.86%, Australia -0.65%, Singapore -1.36%, South Korea -0.53%, India-0.84%. The action by China to devalue the yuan undercut most Asian equity markets on concern it will weaken exports of China's trading partners and slow their economies.

The dollar index (DXY00 unch) is up +0.09%. EUR/USD (^EURUSD) is up +0.15% at a 1-week high. USD/JPY (^USDJPY) is up +0.26%.

Sep T-note prices (ZNU15 +0.38%) are up +18 ticks as the slide in global equities boost the demand for government debt.

The PBOC unexpectedly cut the yuan's daily fixing by 1.9% today, the most since China ended a dual-currency system in 1994, which sent the yuan tumbling down to a 2-3/4 year low of 6.33 per dollar. The action by the PBOC is seen as weakening the yuan in an attempt to support exporters, although the PBOC said the change was a one-time adjustment.

The German Aug ZEW survey of expectations of economic growth unexpectedly fell -4.7 to 25.0, weaker than expectations of +2.2 to 31.9 and the lowest in 9 months.

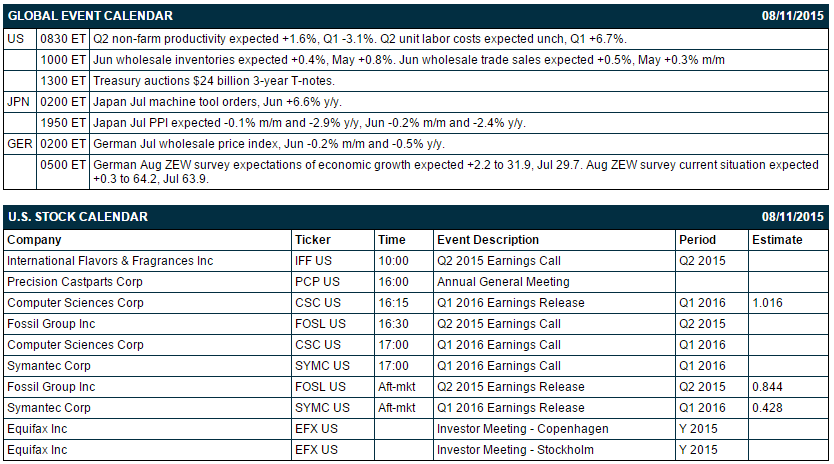

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Q2 non-farm productivity (expected +1.6%, Q1 -3.1%) and Q2 unit labor costs (expected unch, Q1 +6.7%), (2) Jun wholesale inventories (expected +0.4%, May +0.8%), and (3) the Treasury's auction of $24 billion of 3-year T-notes.

There are 3 of the S&P 500 companies that report earnings today: Computer Sciences (consensus $1.02), Fossil Group (0.84), Symantec (0.43).

U.S. IPO's scheduled to price today include: Global Blood Therapeutics (GBT), Conifer Holdings (CNFR), Axalta Coating Systems (AXTA), Acadia Healthcare (ACHC), Bright Horizons Family Solutions (BFAM), QTS Realty Trust (QTS).

Equity conferences during the remainder of this week include: Pacific Crest Global Technology Leadership Forum on Mon-Tue, Goldman Sachs Power, Utility, MLP & Pipeline Conference on Tue, J.P. Morgan Auto Conference on Tue-Wed, Oppenheimer Technology, Internet & Communications Conference on Tue-Wed, Jefferies Industrials Conference on Tue-Thu, Cowen and Co. Communications Infrastructure Summit on Wed, Canaccord Genuity Growth Conference on Wed-Thu, Nomura Media & Telecom Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Valspar (VAL +1.68%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Intuit (INTU -0.43%) was downgraded to 'Sector Perform' from 'Outperform' at RBC Capital.

International Game (IGT +1.23%) reported Q2 adjusted EPS of 35 cents, better than consensus of 28 cents

Google (GOOG -0.25%) was upgraded to 'Buy' from 'Neutral' at Mizuho.

Towers Watson (TW -0.32%) lowered guidance on fiscal 2016 Q1 adjusted EPS to $1.30-$1.35, below consensus of $1.38, and lowered guidance on fiscal 2016 revenue to $870 million-$885 million, below consensus of $891.63 million.

Semiconductor Manufacturing (SMI +4.05%) reported Q2 EPS of 10 cents, double consensus of 5 cents.

Symantec (SYMC +0.93%) reported Q1 EPS of 40 cents, below consensus of 43 cents.

Hertz (HTZ +7.47%) reported Q2 adjusted EPS of 19 cents, right on consensus, although Q2 revenue of $2.69 billion was below consensus of $2.71 billion.

Stifel Financial (SF +1.67%) reported Q2 EPS of 71 cents, below consensus of 73 cents.

Snyder's-Lance (LNCE -0.76%) reported Q2 adjusted EPS of 27 cents, above consensus of 26 cents.

Live Nation ({=LYV reported Q2 revenue of $1.86 billion, higher than consensus of $1.70 billion.

Vipshop (VIPS -0.33%) reported Q2 EPS of 14 cents, better than consensus of 12 cents.

Kraft (KHC +0.45%) reported Q2 EPS of 92 cents, above consensus of 84 cents.

Rackspace (RAX -1.00%) reported Q2 EPS of 20 cents, right on consensus.

The Gap Inc. (GPS +1.06%) reported Jul comparable same-store-sales were down 3%, and then lowered guidance on Q2 adjusted EPS to 63 cents-64cents, below consensus of 66 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU15 -0.54%) this morning are down -7.50 points (-0.36%). Monday's closes: S&P 500 +1.28%, Dow Jones +1.39%, Nasdaq +1.17%. The S&P 500 on Monday closed higher on carry-over support from a rally in Chinese stocks on speculation that China will boost stimulus measures after China Jul PPI fell -5.4% y/y, the biggest decline in 5-3/4 years, and after China Jul exports fell -8.3% y/y, weaker than expectations of-1.5% y/y. Stocks also gained support from increased M&A activity after Berkshire Hathaway bought Precision Castparts for $37.2 billion and from strength in commodity producers as most commodity prices closed sharply higher.

Sep 10-year T-note prices (ZNU15 +0.38%) this morning are up +18 ticks. Monday's closes: TYU5 -14.0, FVU5 -5.00. Sep T-notes on Monday closed lower on reduced safe-haven demand for T-notes after stocks rallied and on supply pressures as the Treasury this week conducts its $64 billion quarterly refunding operation.

The dollar index (DXY00 unch) this morning is up +0.083 (+0.09%). EUR/USD (^EURUSD) is up +0.0017 (+0.15%). USD/JPY (^USDJPY) is up +0.33 (+0.26%). Monday's closes: Dollar Index -0.404 (-0.41%), EUR/USD +0.00532 (+0.49%), USD/JPY +0.429 (+0.35%). The dollar index on Monday fell to a 1-week low and closed lower on dovish comments from Fed Vice Chair Fischer who said he wanted to see the pace of inflation pick up before the Fed begins to raise interest rates. The dollar also saw pressure as the commodity currencies of Canada and Australia rallied on the recovery in commodity prices.

Sep crude oil (CLU15 -1.78%) this morning is down -71 cents and Sep gasoline (RBU15 -1.49%) is down -0.0220 (-1.30%). Monday's closes: CLU5 +1.09 (+2.48%), RBU5 +0.0710 (+4.37%). Sep crude oil and gasoline on Monday closed higher as Sep crude rebounded from a 4-3/4 month low. Crude oil rallied on short-covering, a weaker dollar, and news that China July crude oil imports rose +4.1% m/m to a record 30.71 MMT. Gasoline gained support from unplanned refinery closures after BP's Whiting, Indiana, refinery and Marathon Petroleum's Catlettsburg, Kentucky, refinery both halted production due to unplanned maintenance.

Disclosure: None.