Morning Call For Aug. 13, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 +0.47%) this morning are up +0.49% on expectations that today's U.S. Jul retail sales will be strong and European stocks are up +1.00% on better-than-expected earnings results from E.ON SE and Swiss Life Holdings AG. Asian stocks closed mostly higher: Japan +0.35%, Hong Kong +0.81%, China +0.08%, Taiwan +0.74%, Australia -0.28%, Singapore -0.06%, South Korea +0.98%, India +0.15%. China's Shanghai Stock Index recovered losses and rose to an 8-month high after weaker-than-expected Chinese economic data on new loans, industrial production and retail sales boosted speculation the government will increase economic stimulus measures. Commodity prices are mixed. Sep crude oil (CLU14 -0.10%) is up +0.04%. Sep gasoline (RBU14 -0.37%) is down -0.29%. Dec gold (GCZ14 -0.10%) is down -0.14%. Sep copper (HGU14-0.67%) is down -0.59% at a 1-1/2 month low. Agriculture and livestock prices are mixed with Oct cattle down -0.19% at a 2-month low and Oct hogs down -0.64% at a 4-3/4 month low. The dollar index (DXY00 +0.13%) is up +0.16%. EUR/USD (^EURUSD) is down -0.07% after Eurozone Jun industrial production unexpectedly declined for a second month. USD/JPY (^USDJPY) is up +0.20%. GBP/USD slid to a 2-1/4 month low after BOE Governor Carney said that global political risks and weakness in the Eurozone might weigh on Britain's recovery and that the BOE won't raise interest rates too soon or too fast. Sep T-note prices (ZNU14 -0.06%) are down -4 ticks.

China Jul new yuan loans were 385.2 billion yuan, less than half of expectations of 780.0 billion yuan and the smallest increase in 4-1/2 years.

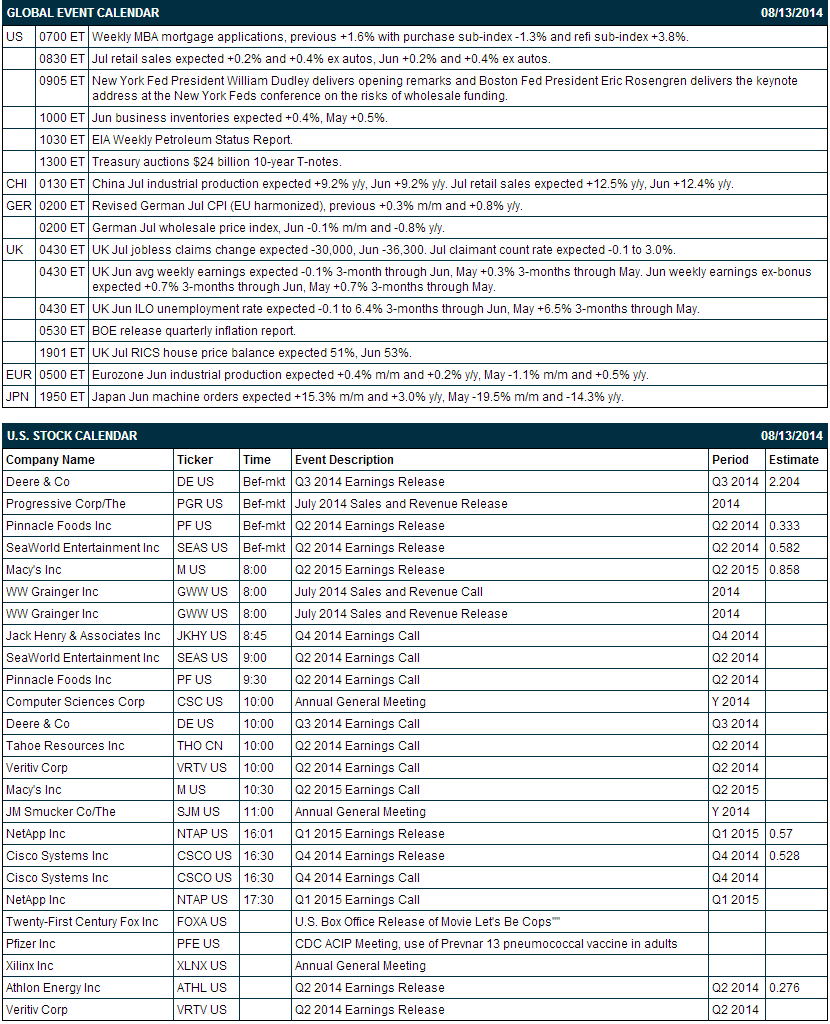

China Jul industrial production rose +9.0% y/y, less than expectations of +9.2% y/y.

China Jul retail sales rose +12.2% y/y, less than expectations of +12.5% y/y.

Eurozone Jun industrial production unexpectedly fell for a second month as it dropped -0.3% m/m, weaker than expectations of +0.4% m/m. On an annual basis, Jun industrial production was unchanged y/y, weaker than expectations of +0.2% y/y.

UK Jul jobless claims fell -33,600, more than expectations of -30,000. The Jul claimant count rate fell -0.1 to 3.0%, right on expectations and the lowest in 5-3/4 years.

The UK Jun ILO unemployment rate fell -0.1 to 6.4% for the 3 months through Jun, right on expectations and the lowest in 5-1/2 years.

UK Jun avg weekly earnings fell -0.2% in the 3 months through Jun, a bigger decline than expectations of -0.1% and the largest decrease in 5 years. Jun weekly earnings ex-bonus rose +0.6% in the 3 months though Jun, less than expectations of +0.7%.

Japan Q2 GDP fell -6.8% q/q annualized, the largest pace of contraction in 3-1/2 years, although less than expectations of -7.0% q/q annualized. The Q2 GDP deflator rose +2.0% y/y, more than expectations of +1.6% y/y and the fastest pace since the data were first complied in 1995.

U.S. STOCK PREVIEW

Today’s July retail sales report is expected to show a moderate increase of +0.2% and +0.4% ex-autos, thus matching June’s report of +0.2% and +0.4% ex-autos. The Treasury today will sell $24 billion of 10-year T-notes. There are 4 of the S&P 500 companies that report earnings today: Deere (consensus $2.20), Macy's (0.86), NetApp (0.57), Cisco Systems (0.53). Equity conferences during the remainder of this week include: Jefferies Global Industrials Conference on Mon-Thu, Oppenheimer Technology, Internet & Communications Conference on Tue-Wed, JP Morgan Auto Conference on Wed, Canaccord Genuity Growth Conference on Wed-Thu, and Barclays Summer Utilities Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Deere & Co. (DE -0.78%) reported Q3 EPS of $2.33, higher than consensus of $2.20, but then said worldwide sales of agriculture and turf equipment are forecast to decrease by about 10% for fiscal-year 2014.

SeaWorld (SEAS +0.32%) reported Q2 EPS of 43 cents, well below consensus of 59 cents.

Southern Company (SO +0.37%) was downgraded to 'Underweight' from 'Equal Weight' at Morgan Stanley.

Demandware (DWRE +1.04%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs.

Ford (F +0.23%) was upgraded to 'Buy' from 'Hold' at Stifel.

CSR (CSRE +0.25%) was downgraded to 'Hold' from 'Buy' at Jefferies.

Fossil (FOSL -0.93%) reported Q2 EPS of 98 cents, better than consensus of 96 cents.

JDSU (JDSU -0.50%) reported Q4 adjusted EPS of 14 cents, higher than consensus of 13 cents.

King Digital (KING +0.17%) plummeted over 20% in after-hours trading after it reported Q2 adjusted EPS of 59 cents, right on consensus, but reported Q2 revenue of $593.5 million, below consensus of $605.67 million.

Cree (CREE -0.99%) slipped 7% in after-hours trading after it reported Q4 EPS of 42 cents, better than consensus of 41 cents, but then lowered guidance on Q1 EPS to 40 cents to 45 cents, below consensus of 46 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.47%) this morning are up +9.50 points (+0.49%). The S&P 500 index on Tuesday closed lower: S&P 500 -0.16%, Dow Jones -0.06%, Nasdaq -0.13%. The main bearish factor was negative carry-over from a slide in European stocks after the German Aug ZEW survey expectations of economic growth slumped -18.5 to 8.6, a much bigger decline than expectations of -10.1 to 17.0 and the lowest in 20 months. Stock losses were contained on signs of strength in the U.S. labor market after U.S. Labor Department data showed U.S. employers posted 4.67 million job offers in June, up +2.1% m/m and the most monthly job openings in 13-1/2 years.

Sep 10-year T-notes (ZNU14 -0.06%) this morning are down -4 ticks. Sep 10-year T-note futures prices on Tuesday closed lower. Bearish factors included (1) signs of strength in the U.S. labor market after Labor Department data showed U.S. employers posted 4.67 million job offers in June, the most in 13-1/2 years, and (2) slack demand for the Treasury’s $27 billion auction of 3-year T-notes that had a bid-to-cover ratio of 3.03, well below the 12-auction average of 3.34. Closes: TYU4 -3.00, FVU4 +0.50.

The dollar index (DXY00 +0.13%) this morning is up +0.133 (+0.16%). EUR/USD (^EURUSD) is down -0.0009 (-0.07%) and USD/JPY (^USDJPY) is up +0.20 (+0.20%). The dollar index on Tuesday closed higher on bullish factors that included (1) weakness in EUR/USD after the German Aug ZEW investor confidence fell to the lowest in 20 months, and (2) increased safe-haven demand for the dollar as stocks fell. Closes: Dollar index +0.034 (+0.04%), EUR/USD -0.00159 (-0.12%), USD/JPY +0.071(+0.07%).

Sep WTI crude oil (CLU14 -0.10%) this morning is down -4 cents (-0.04%) and Sep gasoline (RBU14 -0.37%) is down -0.0079 (-0.29%). Sep crude and gasoline prices on Tuesday closed lower: CLU4 -0.76 (-0.77%), RBU4 -0.0174 (-0.63%). Bearish factors included (1) demand concerns after the IEA cut its 2014 global oil demand estimate by -180,000 barrels a day and cut its 2015 global oil demand estimate by -90,000 barrels a day, and (2) dollar strength. Losses were contained on expectations that Wednesday’s weekly EIA data will show crude stockpiles declined for the seventh consecutive week.

Disclosure: None