Morning Call For April 9, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.06%) this morning are little changed. The Euro Stoxx 50 index is up +0.60% on some optimism after Greece made its 450 million euro IMF payment that was due by today and German industrial production rose +0.2% m/m. Asian stocks today closed mixed: Japan +0.75%, Hong Kong +2.70%, China -0.93%, Taiwan -0.04%, Australia -0.48%, Singapore -0.01%, South Korea -0.07%, India +0.62%, and Turkey -0.01%.

The dollar index (DXY00 +0.27%) is up +0.023 (+0.24%) on an extension of this week's rally. EUR/USD (^EURUSD) is down -0.0012 (-0.11%) and USD/JPY (^USDJPY) is down -0.13 (-0.11%). Jun 10-year T-notes (ZNM15 +0.02%) are up +3 ticks.

Commodity prices are mildly higher by +0.15%. May crude oil (CLK15 +2.06%) is up $1.27 (+2.52%) on a modest rebound after yesterday's -6.6%plunge on the bearish EIA report. May gasoline (RBK15 +1.49%) is up +0.0342 (+1.97%). May natural gas (NGK15 +0.34%) is up +0.025 (+0.95%).

Precious metals prices are trading slightly lower due to the higher dollar: Jun gold (GCM15 -0.37%) -3.5 (-0.29%), May silver (SIK15 -0.72%) -0.144(-0.88%). May copper (HGK15 +0.31%) up +0.016 (+0.59%). Grain prices are trading lower and softs are trading mostly lower.

Alcoa is down -2.3% in overnight trading after yesterday's earnings news, which was better than expected but caused concern since the company said it expects there to be an aluminum oversupply.

Greece reportedly made its 450 million euro payment to the IMF that was due today, which boosted Greek stocks today by +0.4% and caused the 10-year Greek bond yield to drop by 29 bp to 11.25%. Greece's Jan unemployment rate fell by -0.2 points to 25.7% from Dec's 25.9%, while Feb industrial production improved to +1.9% y/y from -0.2% y/y in Jan.

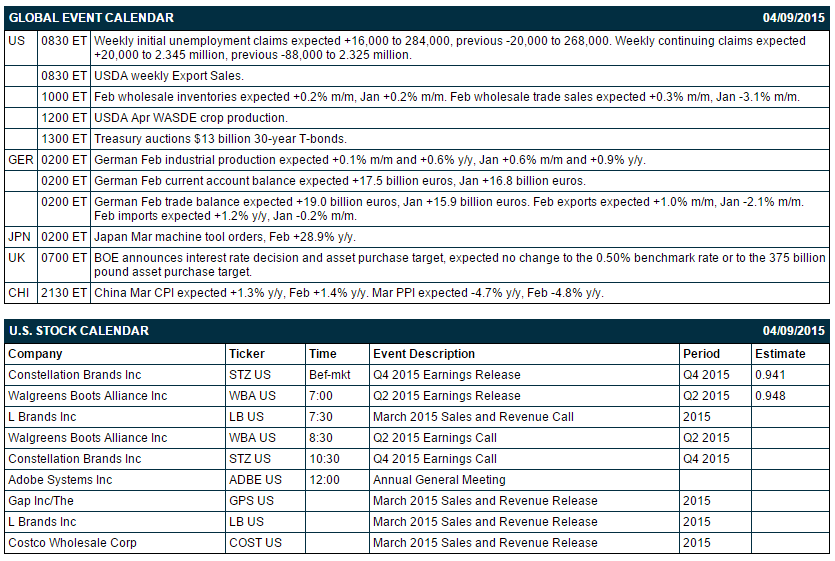

The Bank of England today left its monetary policy unchanged with the base rate at 0.50% and its asset purchase target unchanged at 375 million sterling. That outcome was in line with market expectations.

The Bank of Korea today left its key interest rate unchanged at 1.75%, which was in line with market expectations.

The German Feb industrial production report of +0.2% m/m and -0.3% y/y was slightly better than expectations on a month-on-month basis of +0.1%, although the year-on-year level of -0.3% was weaker than expectations of +0.6%. Jan was revised lower to -0.4% m/m and unchanged y/y from +0.6% m/m and +0.9% y/y.

German exports rose by +1.5% m/m, which was better than market expectations of +1.0% and the Jan report of -2.1%. The German Feb trade balance rose to 19.2 billion euros, which was higher than market expectations of 19.0 billion euros and was up from Jan's 15.9 billion euros.

U.S. STOCK PREVIEW

Key U.S. news today includes (1) the weekly initial claims report (expected +16,000 to 284,000 after last week's -20,000 to 268,000) and continuing claims report (expected +20,000 to 2.345 million after last week's -88,000 to 2.325 million), (2) Feb wholesale inventories (expected +0.2% m/m after Jan's +0.2% m/m), and (3) the Treasury's auction of $13 billion of 30-year T-bonds to conclude this week's $58 billion coupon package.

There are two of the Russell 1000 companies that report earnings today: Constellation Brands (consensus $0.94), Walgreens Boots Alliance (0.95).

U.S. IPO's that price today include: Professional Diversity Network (IPDN).

Equity conferences during the remainder of this week include: Internet of Things (IoT) Asia 2015 on Wed-Thu, and JP Morgan Spring Fling Conference on Thu.

June E-mini S&Ps this morning are trading slightly lower after Alcoa kicked off the earnings season with negative news. Wednesday's closes: S&P 500 +0.27%, Dow Jones +0.15%, Nasdaq +0.83%. The U.S. stock market on Wednesday closed mildly higher on continued optimism about interest rates even though the March 17-18 FOMC minutes said that “several” FOMC members favor a rate hike by June. The overall stock market also help up despite the 6.6% plunge in crude oil prices that hurt the petroleum sector.

OVERNIGHT U.S. STOCK MOVERS

- Alcoa (AA +1.79%) is down more than 2% in pre-opening trade after saying late yesterday that it expects an aluminum surplus.

- Constellation Brands (STZ +0.76%) reported Q4 EPS of $1.03, better than the consensus of 94 cents.

- Walgreens Boots Alliance (WBA +0.46%) reported Q2 adjusted EPS of $1.18, which was better than the consensus of 95 cents.

- Bed Bath & Beyond (BBBY +1.28%) fell more than 3% in after-hours trading after disappointing earnings.

- Brookfield Asset Management (BAM +1.98%) announces 3-for-2 stock split and raised its dividend by 6%.

- Apogee (APOG +2.31%) rallied 6% in after-hours trading after reporting favorable earnings.

- Pier 1 Imports (PIR -0.24%) rallied more than 4% in after-hours trading after reporting favorable earnings.

- Inovio Pharmaceuticals (INO +7.05%) rallied nearly 6% in after-hours trading after news it was selected to lead a $45 million Ebola prevention program.

MARKET COMMENTS

Jun 10-year T-note prices this morning are trading mildly higher by +3 ticks. Wednesday's closes: TYM5 unch, FVM5 -0.5. June 10-year T-note prices on Wednesday closed unchanged as the market basically ignored the FOMC minutes saying that “several” FOMC members favor a rate hike by June. There was no real change yesterday in the market consensus that the Fed will be forced to wait until early 2016 to make its first rate hike. The T-note market held its ground despite supply overhang from this week’s $58 billion coupon package.

The dollar index this morning is up +0.023 (+0.24%) on an extension of this week's rally. EUR/USD is down -0.0012 (-0.11%) and USD/JPY is down-0.13 (-0.11%). Wednesday's closes: Dollar index +0.24 (+0.24%), EUR/USD -0.0033 (-0.31%), USD/JPY -0.15 (-0.12%). The dollar index on Wednesday closed mildly higher after news from the FOMC minutes that “several” FOMC members favor a rate hike as early as June. The Bank of Japan on Wednesday left its monetary policy unchanged, which was in line with market expectations.

May crude oil this morning is up $1.27 (+2.52%) on a modest rebound after yesterday's -6.6% plunge on the bearish EIA report. May gasoline is up +0.0342 (+1.97%). May natural gas is up +0.025 (+0.95%). Wednesday's closes: CLK5 -3.56 (-6.60%), RBK5 -0.1217 (-6.54%). May crude oil and gasoline on Wednesday closed sharply lower after the weekly EIA report showed a massive +10.95 million bbl (+2.3%) increase in U.S. oil inventories to a new record high as well as a +2.1% increase in Cushing crude oil inventories to a new record high. In addition, the EIA report showed that U.S. oil production in the latest reporting week rose by +0.2%, discouraging talk that U.S. oil production might be in for a sustained drop.

Disclosure: None.