Morning Call For April 20, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.43%) this morning are up +0.60% and European stocks are up +0.89% as China boosted stimulus after the PBOC cut banks' reserve ratio requirements by 1 percentage point, the biggest cut since 2008. European stocks also benefitted from an increase in M&A activity as Tenet Group Holding NV jumped over 4% after it bought Belgian mobile-phone business Base for 1.33 billion euros ($1.43 billion). Asian stocks closed mostly lower: Japan -0.09%, Hong Kong -2.02%, China -1.64%, Taiwan -0.a9%, Australia -0.76%, Singapore -0.62%, South Korea +0.10%, India-1.95%. Japan's Nikkei Stock Index fell to a 2-week low on carry-over weakness from Friday's slide in U.S. stocks, while China's Shanghai Composite Index retreated from a 7-year high after Chinese regulators on Friday tightened rules on buying stocks with borrowed money and bolstered short selling of stocks.

Commodity prices are mostly lower as the dollar strengthened. May crude oil (CLK15 -1.51%) is down -0.04% and May gasoline (RBK15 -1.58%) is down -0.27%. Losses were limited on speculation the action by China to boost stimulus will spur economic growth and energy demand. Metals prices are weaker. Jun gold (GCM15 -0.37%) is down -0.35%. May copper (HGK15 -1.48%) is down -1.05%. Agriculture prices are mixed.

The dollar index (DXY00 +0.41%) is up +0.44%. EUR/USD (^EURUSD) is down -0.67% as European leaders continue to wrangle with Greece over how to secure future financing. USD/JPY (^USDJPY) is up +0.13%.

Jun T-note prices (ZNM15 -0.19%) are down -8 ticks as stock rallied.

The PBOC cut the reserve-requirement ratio for banks by 1 percentage point to 18.5% in an attempt to boost lending and stimulate growth. It was the second time this year the PBOC cut banks' reserve requirements and follows Saturday's comments from PBOC Governor Zhou Xiaochuan who said "we have room in the reserve ratio and our interest rates are not zero yet."

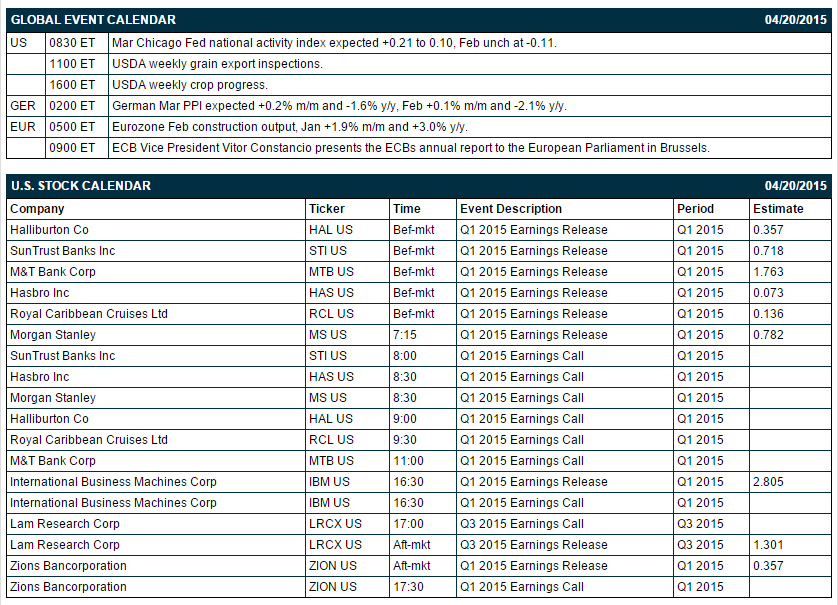

U.S. STOCK PREVIEW

Key U.S. news today includes (1) Mar Chicago Fed national activity index (expected +0.21 to 0.10 after Feb's unch at -0.11).

There are 9 of the S&P 500 companies that report earnings today: Morgan Stanley (consensus $0.78), IBM (2.81), Halliburton (0.36), SunTrust Banks (0.72), M&T Bank (1.76), Hasbro (0.07), Royal Caribbean Cruises (0.14), Lam Research (1.30), Zions Bancorp (0.36).

U.S. IPO's scheduled to price or trade today: none.

Equity conferences this week include: 121 Mining Investment Conference - London on Mon, IPAA Oil & Gas Conference on Mon-Tue, American Association for Cancer Research Meeting on Mon-Wed, IHS CERAWeek Energy Conference on Mon-Thu, Cards & Payments Asia 2015 on Tue, Financial Times Commodities Global Summit on Tue-Wed, Future Bank Asia 2015 on Tue-Wed, American Academy of Neurology Meeting on Wed, Capital Link Closed-End Funds & Global ETFs Forum - Panel on Thu, RSA Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Morgan Stanley (MS -1.63%) reported Q1 EPS of 85 cents, higher than consensus of 78 cents.

Halliburton (HAL -1.97%) reported Q1 EPS of 49 cents, better than consensus of 36 cents.

SunTrust Banks (STI -1.71%) reported Q1 EPS of 78 cents, above conensus of 72 cents.

Nokia (NOK -1.93%) was downgraded to 'Hold' from 'Buy' at Jefferies.

Marathon Oil (MRO -0.59%) was upgraded to 'Overweight' from 'Equal Weight' at Morgan Stanley.

General Mills (GIS -0.25%) was upgraded to 'Neutral' from 'Sell' at Goldman SAchs.

Colgate-Palmolive (CL -1.14%) was downgraded to 'Sell' from 'Neutral' at Goldman Sachs.

HSBC (HSBC -1.25%) was upgraded to 'Conviction Buy' from 'Buy' at Goldman Sachs.

Symantec (SYMC -0.25%) was upgraded to 'Hold' from 'Underperform' at Jefferies.

Alibaba (BABA -2.57%) was initiated with a 'Buy' at Summit Research with a price target of $97.

Hasbro (HAS -0.24%) reported Q1 EPS of 21 cents, well above consensus of 7 cents.

Costco (COST -1.73%) rose over 1% in pre-market trading after the retailer struck a eal with Visa and Citigroup under which its acceptance costs for credit-card payments will be about zero.

Michael Kors Holdings Limited (KORS -0.74%) fell 1% in pre-market trading after Mizuho Financial Group cut it's recommendation on the stock to 'Neutral' from 'Buy.'

MARKET COMMENTS

June E-mini S&Ps (ESM15 +0.43%) this morning are up +12.50 points (+0.60%). Friday's closes: S&P 500 -1.13%, Dow Jones -1.54%, Nasdaq -1.52%. The S&P 500 on Friday fell to a 1-1/2 week low and closed sharply lower on carry-over pressure from the plunge in Chinese stock futures on Chinese government action to clamp down on margin buying and expand short-selling. In addition, the U.S. Mar core CPI rose by +0.1 point to +1.8% y/y, which caused some concern that the Fed might tighten sooner rather than later. Stocks failed to get much support from the +2.9 point rise to 95.9 in the preliminary-April U.S. consumer confidence index from the University of Michigan.

Jun 10-year T-notes (ZNM15 -0.19%) this morning are down -8 ticks. Friday's closes: TYM5 +4.00, FVM5 -0.75. Jun 10-year T-notes on Friday closed higher on the sharp sell-off in stocks and carry-over support as the German 10-year bund yield sank to an all-time low of 0.049%. T-note prices were undercut, however, by the larger-than-expected increase in the April U.S. consumer sentiment index and by the rise in the 10-year T-note breakeven inflation expectations rate to a 5-month high.

The dollar index (DXY00 +0.41%) this morning is up +0.431 (+0.44%). EUR/USD (^EURUSD) is down -0.0072 (-0.67%). USD/JPY (^USDJPY) is up +0.15 (+0.13%). Friday's closes: Dollar Index +0.105 (+0.11%), EUR/USD +0.0042 (+0.39%), USD/JPY -0.096 (-0.08%). The dollar index on Friday recovered from a 1-1/2 week low and closed higher on the stronger-than-expected U.S. prelim-April U.S. consumer confidence index and U.S. March core CPI report of +1.8% y/y.

May WTI crude oil (CLK15 -1.51%) this morning is down -2 cents (-0.04%) and May gasoline (RBK15 -1.58%) is down -0.0052 (-0.27%). Friday's closes: CLK5 -0.97 (-1.71%), RBK5 -0.0055 (-0.30%). May crude oil and gasoline prices Friday closed lower on the rebound in the dollar index, the sharp sell-off in the S&P 500 index, and pre-weekend long liquidation pressure after the month-long recovery rally.

Disclosure: None.