May US/World Wheat Update

Market Analysis

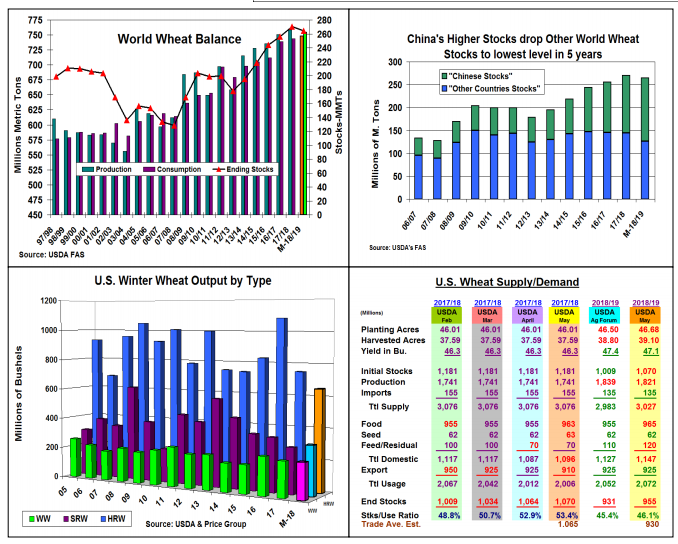

May’s USDA World wheat stocks showed their first drop since the 2012/13 crop year last week. As suspected, the Ag Department reduced its world output forecast by 10.6 mmt to 748 mmt. Russia and the EU are the world export competitors projected to have lower output while Argentina, Australia, and Canada are the countries with modest increases in 2018. This year’s US crop is also forecast to be up 2.2 mmt. The USDA did raise their 2018/19 world demand by 1.4% to 753 mmt this year. This tightens their world’s carryover forecast by 6 mmt to 264.3. Because of computer programming issues, the USDA didn’t separate China out of the world data as expected. However, China’s USDA crop size is projected to remain stable at 129 mmt while consumption may rise by 3 mmt to 120 mmt. This will result in their stocks increasing 11.8 mmt to 138.6 mmt. This means China will make up 52% of the world stocks while the balance of world’s stocks is projected to be the lowest since 2012/13 at 125.7 mmt. In practical terms, this means an 18 mmt drop in non-Chinese stocks leaving the current available tradeable supplies at their 6-year lows in 2018/19.

Given 2018’s extensive SW drought & the Kansas crop tour results, trade ideas for the 1st USDA winter wheat crop were low. The USDA’s 1.192 billion bu. estimate was 14 million higher than the average guess. May’s hard red and white wheat levels were similar to the trade while the initial soft red forecast was higher. Another difference was the USDA assigning a 630 million bu. output to spring/durum seeding vs. the trade using a 600 million bu. level for this portion of the crop. Overall, the USDA reduced some old-crop export demand while it upped some domestic food demand resulting in 1.07 billion bu. stocks. The USDA also upped its new-crop food and feed usage, but left exports at Ag Forum levels for 2018/19 yielding a 955 million bu. stocks level.

What’s Ahead

Given 2018’s the late development of hard red crop in the S Plains, the market has remained sensitive to this region’s growing conditions since the report. After last week’s heat, rains have been in the forecast for the coming week since the May report. This outlook and conditions in the Black Sea will be main price factors over the next 4- 6 weeks. Have 40-45 percent of 2018/19 crop sold or hedged at this time.

Disclaimer: The information contained in this report reflects the opinion of the author and should not be interpreted in any way to represent the thoughts of The PRICE Futures Group, any of its ...

more