Markets: Exhaust

The exhaustion of the week should not be ignored. Sure we get the jobs report, and its as usual all-important to understanding the risk/rewards of the weekend and week ahead. Either there is wage inflation in the US or there isn’t. Higher real growth with a stronger consumer balance sheet may make the flurry of worry about the FOMC reaction to stocks reverse. The noise of weather in the report is always a concern and one snowflake doesn’t make a blizzard. The ADP miss yesterday puts the whispers closer to 185,000 NFP rather than 200,000. There are overnight, plenty of stories that make for a smog filled day even before the US labor report. First is that China and the US are still talking and that the US trade deficit yesterday made clear that tariffs haven’t really changed things yet.

Second is that US energy independence makes the OPEC issues even more difficult. The US is now net exporting oil and refined fuel. Third is that the US rate curve inversion is less scary– as more analysts argue its about 3M-10Y not 2Y to 5Y that matters. Finally, we also got a host of little data stories that were mixed showing weaker Japan household spending and weaker German industrial production –all of which makes the higher global growth story into 2019 look harder to believe unless you see China and the US jumpstart things. The most interesting moves in markets – and there weren’t many overnight – come from the UK as Brexit politics and odds get reflected in Gilts and the GBP. All of which puts the risk barometer of GBP/JPY as my favorite to watch into the weekend as it captures oil, trade and politics all in one. This is still a bear market for risk but we should all learn to enjoy the bounces and not to breathe the exhaust.

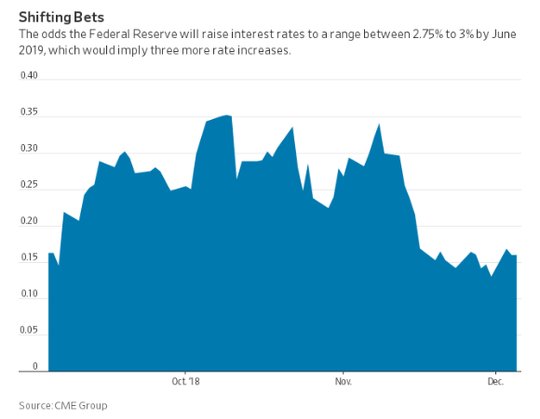

Question for the Day: Is the unwind of the FOMC hikes justified? The short answer is yes – but it’s not stock markets. There are two drivers for the market unwinding Fed hike fears – oil and financial conditions. Moving from normalization to neutral means the FOMC is in data reaction mode and it will wait and see if they think the kink in the 2-5Y rate curve and the noise of the financial conditions suggest we are closer to neutral at 2% than 3%. The shifting bets on the FOMC hit the USD and helped the equity market yesterday. The bounce back in equities has put in a double bottom formation for risk. The FOMC reaction function isn’t just about inflation from wages, it’s also about oil. The lower prices at the pump will help 1Q growth and its going to matter to the outlook for pass-through. Perhaps we all are getting the Powell S&P500 put wrong and its really a WTI put that he has with crude at $50 being the neutral rate.

What Happened?

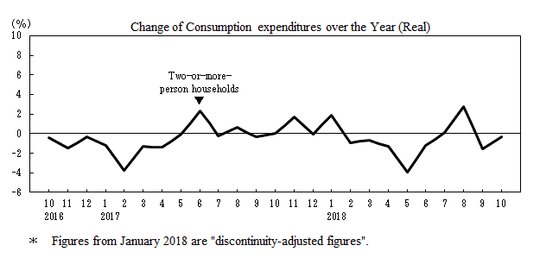

- Japan October Household Spending -0.3% y/y after -1.6% y/y – weaker than +1.6% y/y bounce expected. The government noted that higher prices of fresh vegetables hurt. Also home renovations fell and demand for warmer clothing fell due to better weather. The average of monthly income per household stood at 515,729 yen, up 2.9% in nominal terms and up 1.2% in real terms from the previous year.

- Japan October LEI 100.5 from 99.6 – weaker than 104.8 expected. The coincident index 104.5 from 101.6 – weaker than 114.3 expected.

- China November FX reserves rise $9bn to $3.062trn after -$33.93bn to $3.053trn - better than $16bn drop expected – first gain since July. The CNY gained 0.2% in November vs. USD. The value of China’s gold reserves rose to $72.122 billion from $71.968 billion at the end of October.

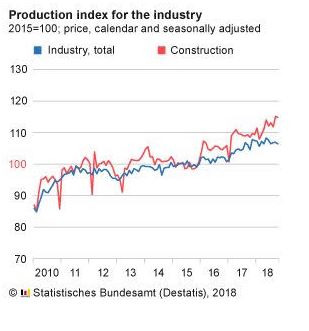

- German October industrial production -0.5% m/m after revised +0.1% m/m - weaker than +0.3% m/m expected. September revised from +0.2% m/m. Ex-energy and construction production fell 0.4% m/m. Capital goods rose 0.3%, intermediate goods rose 0.2% but consumer goods -3.2% and energy was -3.2% m/m. Construction fell 0.3%.

- French October industrial production up 1.2% m/m after -1.6% m/m revised – better than +0.8% m/m expected. September revised from -1.8% m/m. Still by sector (q/q/) Food products -1.2%, energy up 8.1%, transport -1.7%, Water/mining up 0.3%

- French October trade deficit E4.1bn after E5.4bn - better than E6.1bn expected. The Current Account deficit narrows to E0.7bn after E1.9bn – better than E2.1bn expected.

- Italy October retail sales up 0.1% m/m, +1.5% y/y after -0.8% m/m, -2.5% y/y - better than the -0.2% m/m, 1% y/y expected.

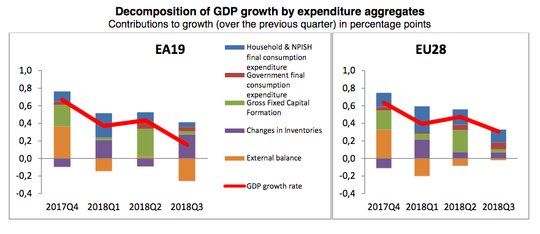

- Eurozone 3Q GDP unrevised at 0.2% q/q, +1.6% y/y after 0.4% q/q, 2.2% y/y – less than the 1.7% y/y expected. Household consumption up 0.1%, capex up marginally, inventories added 0.3pp.

- Eurozone 3Q employment change up 0.2% q/q, 1.3% y/y after 0.4% q/q 1.5% y/y – as expected. In 3Q, Malta and Cyprus were the biggest job gainers in the eurozone while Italy, France lagged. In the EU28 Eastern Europe was weakest.

Market Recap:

Equities: The US S&P500 futures are off 0.4% after losing 0.15% yesterday. The Stoxx Europe 600 up 1.1% - still off nearly 3% on the week. The MSCI Asia Pacific bounced

- Japan Nikkei up 0.82% to 21,678.68

- Korea Kospi up 0.34% to 2,075.76

- Hong Kong Hang Seng off 0.35% to 26,063.76

- China Shanghai Composite up 0.03% to 2,605.89

- Australia ASX up 0.37% to 5,757.90

- India NSE50 up 0.87% to 10,693.70

- UK FTSE so far up 1.3% to 6,789

- German DAX so far up 0.5% to 10,865

- French CAC40 so far up 1.2% to 4,840

- Italian FTSE so far up 0.8% to 18,797

Fixed Income: Bonds are lower with equity bounce but the undoing of Fed Dec hike fears still key and jobs report driving. The UK Gilts are reflecting some Brexit hopes, Italy same for budget deals – 10Y UK yields up 3bps to 1.27%, Italy off 5bps to 3.15% while Spain is flat at 1.47%, Portugal up 1bps to 1.80%, Greece flat at 4.22%. Core EU bonds – German Bund up 3bps to 0.25% and France up 3bps to 0.68%.

- US Bonds are lower with curve unchanged– 2Y up 1bps to 2.76%, 5Y flat at 2.75%, 10Y up 1bps to 2.888%, 30Y up 1bps to 3.15%

- Japan JGBs see curve steepen – focus is on US. 2Y up 1bps to -0.14%, 5Y flat at -0.12%, 10Y up 0.8bps to 0.061%, 20y up 3bps to 0.59%, 30Y up 3bps to 0.81%.

- Australian bonds mixed with focus on China/US trade– 3Y off 1bps to 1.93%, 10Y off 1bps to 2.45%.

- China PBOC skips open market operations, bonds rally further– 2Y off 1bps to 2.79%, 5Y off 1bps to 3.09%, 10Y off 3bps to 3.31%.

Foreign Exchange: The US dollar index is flat at 96.80.

- EUR: 1.1370 flat. Range 1.1360-1.1383 – stuck in a holding pattern ahead of jobs with 1.13-1.14 still key.

- JPY: 112.80 up 0.15%. Range 112.62-112.93 with EUR/JPY 128.30 up 0.2%. Modest equity bounce and US rates holding with 112.40-113.50 key.

- GBP: 1.2755 off 0.2%. Range 1.2740-1.2786 with EUR/GBP .8915 up 0.25%. Weekend politics driving with 1.2650-1.2950 still keys

- AUD: .7225 off 0.25%. Range .7207-.7241. Doing nothing fast with commodities key. NZD up 0.1% to .6880 watching .6840-.6900 for breakouts.

- CAD: 1.3395 up 0.1%. Range 1.3382-1.3399 – waiting for US jobs and watching oil/rates.

- CHF: .9940 up 0.15%. Range .9918-.9943 with EUR/CHF 1.1300 up 0.1% with 1.1280 key base against 1.1320 and USD .9880 against 1.00 still.

- CNY: 6.8825 flat with range 6.8673-6.8886 – most now forecast 7.0 break into 1Q 2019.

Commodities: Oil mixed, Gold up, Copper up 1.5% to $2.8110

- Oil: $51.45 off 0.1%.Range $50.60-$51.83 with equities/OPEC the key drivers and $50 the pivot still. Brent up 0.5% to $60.34 with $58-62 consolidation.

- Gold: $1242 up 0.3%.Range $1237.50-$1243 with focus on USD and rates again with $1236 the pivotal base for $1250 and $1268 retests. Silver up 0.4% to $14.44.

Conclusions: Does a data-dependent Fed mean more volatility? The answer is only when the data is a surprise. The shift from a forward guidance that rates would be low for longer to one where they gradually normalize was the gift of Yellen to Powell. The problem is the credibility of a forward guidance becomes one of how accurate forecasts for the economy prove out to be. The reaction to data makes the risks revolve around surprise results. Today is no exception.

Economic Calendar:

- 0830 am US Nov non-farm payrolls 250k p 200k e / earnings 0.2%p 0.3%e / rate 3.7%p 3.7%e

- 0830 am Canada Nov jobs change 11.2k p 15k e / unemployment rate 5.8%p 5.85%e/ participation 65.2%p 65.5%e

- 1000 am US Dec Michigan consumer sentiment 97.5p 97.0e

- 1000 am US Oct wholesale inventories 0.6%p 0.3%e

- 1215 pm Fed Brainard speech

- 0300 pm US Oct consumer credit $10.92bn p $15.1bn e

View TrackResearch.com, the global marketplace for stock, commodity and macro ideas here.