Learning Emotional Control From This Year’s Market Moves

Labor Day Weekend has ended, and the year is two-thirds over That means it’s a good time to assess what has happened and where we stand in the markets. It’s also a good time to remember what you might have been feeling earlier in the year when asset classes were behaving differently.Understanding your emotions is a big part of successful investing, and can help you deal with market volatility in the future.

US Stocks In 2008 – Up, Down, and Up

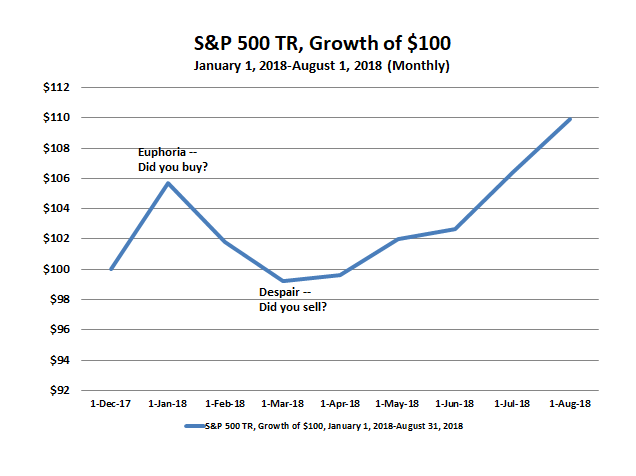

The S&P 500 Index ended August up 9.94% for the year. But that seemingly happy statistic doesn’t indicate what an investor might have felt at various points during the year. After a blistering January during the first three weeks of which it gained nearly 10%, the market melted down in February and March during which it gave back the January gains.

It’s hard to remember now, but many investors were euphoric in January and terrified in March. If you examine our phone logs, they will bear that out. We always get more calls from clients and prospective clients when things look difficult, and our phones were silent in January and ringing non-stop in March. My colleague Danny Ratliff and I also fielded a memorable call on our radio show from an investor in his mid-50s with a balanced allocation whose portfolio was down 5% from its peak. This person was unnerved by that decline, but it didn’t occur to him that he should expect that routinely from a balanced portfolio.

Lessons

The first lesson investors can learn from this year’s market moves is that short term (say, month-to-month) forecasting is virtually impossible. Don’t even try it. We try to manage risk as much as any advisory firm, but no advisor can deliver all of the market’s upside and none of its downside or time every wiggle and squiggle in all asset classes. Some of the burden of achieving good returns falls on you and your ability to control your behavior and to be realistic about volatility.

The person who called in to our radio show probably wasn’t just upset by the 5% decline in his portfolio, but also by the prospect that the declines would continue. And he was right to be thinking about that. Investors should always contemplate a 50% stock market drawdown because that’s how big the last two stock market drawdowns were. That implies a loss in a balanced portfolio on the order of 25%. Accepting volatility is the price of admission to the financial markets. the good news is you can choose how much to accept. Nobody is forcing you to have a lot of stock exposure.

The second obvious lesson is not to get lulled into a false sense of security. The market’s blistering run in January – after a nearly 22% gain in 2017 when the S&P 500 Index experienced no down months – caused investors to be shocked by the February-March declines. But it shouldn’t have. A run like that should have made you suspicious and girded you for volatility. Now that the markets have been calm again through the summer, you should be prepared for volatility again. Nobody knows for sure when it will arrive; the calm may continue for a while longer. But after such calm you’d be foolish to be surprised by turbulence. Stop getting fooled by the same things, and by thinking markets will calm down once and for all at some point. They never calm down once and for all. The calmer they are, and the longer the calm lasts, the more suspicious you should be. You should think that the next big decline is always at hand — and that’s because, often enough, it is. That’s just the way markets work.

The third lesson is to have an asset allocation you can live with. Don’t count on any risk management system to save all your bacon all the time. Investing means taking periodic losses – at least on paper. Get used to it. It’s part of the game. If you’re near retirement or in retirement, and you can’t tolerate losses, there’s nothing to be ashamed of about that. Get yourself into an allocation that will inflict less volatility on you. Reduce your stock exposure for goodness sake. The right amount of stock exposure is the amount you can live with and that will not cause you to sell if the stock market goes down by half. If you’re tempted to sell during declines, you have too much stock exposure. Take this opportunity to think hard about your allocation, and whether it will cause you to do something stupid like sell hard into a decline.

The Case of REITs

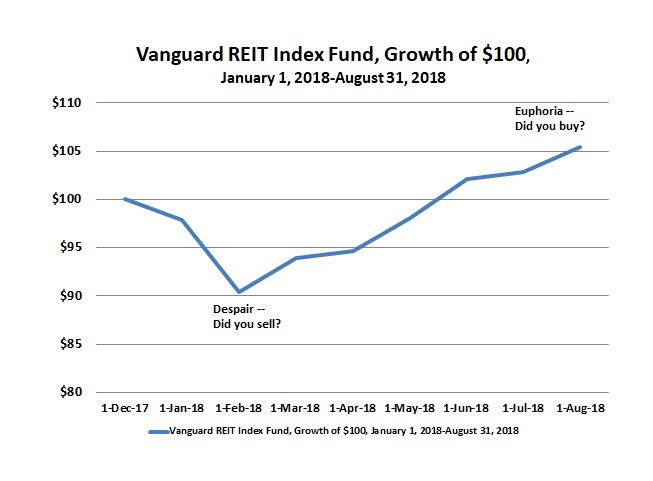

REITs have also had a year of distinctly opposite moves. Unlike the rest of the stock market which roared in January, REITs opened the year poorly. They dropped around 10% in January and February on interest rate fears. REITs are required to pay 90% of their net income as dividends, which gives them some bond-like qualities. That means when rates rise REITs can go down, even if they are the stocks of companies that can pass inflation costs on to tenants in the form of higher rents eventually.

After their 10% drop, REITs began to rebound in late February, and they haven’t looked back since. They are now up around 5% for the year or more than 15% from their lows. But the lessons are the same as with the broader stock market’s moves this year. Don’t try to time every wiggle and squiggle. And now that REITs have put together a strong run, be more suspicious than excited about them. Last, get exposure to them that you can tolerate. Chances are, you won’t time big moves into and out of them well.