Knowing When To Sell Real Estate Investments

by Keith Jurow, Capital Preservation Real Estate Report

For nearly five years, I have offered compelling analysis that the so-called real estate recovery is an illusion. While this evidence has been largely ignored by Wall Street and the pundits, those who heeded my advice in an earlier article to sell certain REITs (VNO, GGP, SPG) and the ETF IYR fared well.

In this article, I will focus directly on the importance of knowing when to sell a real estate investment. I will also look at how the equity REITs I discussed in March have done.

Last November, I wrote an in-depth article about the dangers of euphoria for wealthy investors. I showed that there was a very widespread consensus that the real estate collapse of 2008-2010 had ended. Most investors were quite confident that they no longer need fear a repeat of that calamity.

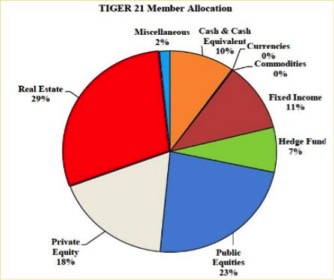

Recent data shows that high net worth investors are more enmeshed than ever in this deadly web of optimism. Here is the first quarter 2015 asset allocation for the more than 300 wealthy members of Tiger 21.

Source: Tiger 21

The average allocation to real estate is now 29%. That is up by 2 percentage points from a year ago and is the highest since Tiger 21 began publishing its member asset allocation in 2007. Complacency of wealthy investors with their real estate portfolios is at dangerous levels.

Further confirmation of this euphoria comes from the results of Savills' latest Wealth Briefing survey, which came out in June. It reported that 91% of wealth managers and private bankers said their clients planned to either increase or maintain their direct real estate holdings in 2015. In addition, 87% intended to increase or maintain their indirect holdings. That is incredibly optimistic.

Why am I so concerned about the excessive bullishness of Tiger 21 members? Back in mid-2008, members had raised their real estate allocation to 26% just as the commercial real estate crash was commencing. Wealthy investors were not helped by their advisors, many of whom had maintained a bullish attitude throughout 2007. Risk management was not a high priority then. The portfolios of high net worth investors who were heavily allocated to real estate were subsequently smashed.

Were lessons learned from the real estate collapse?

Let's be very clear about this: Wall Street trains investors to buy, not to sell. Advisors and their clients need to be constantly reminded that Wall Street rarely makes a recommendation to sell an investment. After all, it got the appellation of "the sell side" for a reason. Wealthy investors had better look somewhere else for advice on when to sell.

Last year, I gave a presentation at a major conference in New York City on risk and liquidity. The title of my talk was "The Wisdom of Knowing When to Sell."

For two days, I mingled with the institutional attendees to get a good feel for what concerned them. Their focus was on what to buy in their search for yield. Hardly a word was said about what to sell or when to sell holdings in their portfolios. That was the furthest thing from their minds. I suspected that getting across my key points in the presentation would be a challenge.

As I ran through my presentation about risks that institutional investors were probably not aware of, I scanned the room for reactions from the audience. What I saw was a stunned "deer-in-the-headlights" look. What I was saying was important for their portfolios, but they were too shocked to show much response.

In the last part of my presentation, I explained my views about selling. Having observed markets for a long time, I had seen over and over again that the exit door for large institutional investors is very narrow. I emphasized that this door could close very quickly and made it very clear that the only safe exit for large institutions is to sell sooner rather than later.

Feedback from attendees was positive, yet I doubted that many would take any action. Why not? They were at the conference to find out what to buy, not when to sell.

Timing matters to investors

We hear a lot of talk these days that trying to spot the top of a market is a losing proposition. Perhaps, but that is really a straw man. No one can really call the absolute top of a long-term bull market. The wise thing is to sense that a market is excessively risky and that valuations are no longer connected to fundamentals. To decide that selling off some or all of one's holdings and raising cash levels is a prudent precaution in that environment.

During the beginning of the credit crisis in 2008, wealthy investors were still caught up (like nearly everyone else) in the frothy optimism of the bull market in equities and had not even considered that the real estate bubble could pop. They had at least a year to lighten up their real estate portfolios, and smart investors did just that. Unfortunately, most of them could not shake their euphoria, and their portfolios were crushed in 2008 and 2009.

It is very rare today to see any serious discussion of the investment risks in real estate.

Treasure your cash when investors are euphoric

Back in 2012, Morgan Stanley's head of wealth management had the temerity to assert that holding cash was unsafe. Really? Of course, he meant that the opportunity costs during a bull market were very high. Unfortunately, that view resonates with wealthy and not-so-wealthy investors.

Widespread investment euphoria causes even savvy investors to lose the necessary vigilance. Market and credit risks are brushed aside or, even worse, not examined at all. There is a very dangerous assumption held by real estate investors that the worst is over. Risk is no longer a major consideration. The only important question: What is the appropriate asset allocation?

Investors have apparently been duped by Wall Street's claim that they need to be fully invested now. This is confirmed by the April figures for NYSE margin debt, which showed a record level of $507 billion.

Morgan Stanley's June 2015 asset allocation recommendation for investors with net worth less than $30 million suggested a 1% cash position for those with a moderate risk comfort level. Of course, they do not explain why this might be a high-risk proposition. This sounds like more of "the coast is clear" that we have heard for several years now. Remember, this is the "sell side" talking.

The puzzling thing is that the wealthy members of Tiger 21 completely disregard this recommendation. Their latest asset allocation survey showed an average cash level of 10%. Although this cash allocation was down from 14% at the end of 2011, that could indicate Wall Street has less influence over high net worth investors than we think.

Further evidence comes from U.S. Trust's 2015 Insights on Wealth and Worth. It surveyed roughly 640 wealthy investors with investable assets greater than $3 million and found that 62% held more than 10% of their total portfolio in cash. That would appear to confirm the Tiger 21 figure. But it is not so simple.

The U.S. Trust survey also found that more than half of those investors surveyed were focused more on growing their portfolio than on asset preservation. More than a third of them were willing to take on higher risk to obtaining greater returns. That percentage was down only slightly from a couple of years ago.

The percentage of those surveyed who were optimistic about the stock market climbed from 40% in 2014 to 45% in this year's survey. You may think that this percentage of optimists is low. However, a mere 6% of these wealthy investors were pessimistic. That is bullish euphoria. Nothing was specifically asked about how concerned those surveyed were about current risks to their portfolio.

Knight Frank is one of the largest real estate consulting firms in the world with headquarters in London. In its 2015 Wealth Report, the company found that 37% of UHNW clients surveyed had increased their exposure to real estate in 2014. The same percentage expected that to continue in 2015. The report also revealed that their younger wealthy clients were even more interested in property investing than their parents.

Follow the smart sellers

During times of bullish euphoria, it is prudent not to follow what buyers are doing. Instead, take a good look at what smart sellers are doing.

Back in the middle of the real estate bubble in 2005, money had been flooding into equity REITs at a record pace. Asking prices on all kinds of properties were soaring. More than one article in 2005 pointed out that the smart money was starting to get out of commercial real estate.

As I have explained in several previous articles, once again the smart investors are unloading their properties very briskly in the major metros. These are mainly wealthy investors who understand real estate risks and treat their hard-earned assets with great care. They are able to discern when real estate markets lose touch with the fundamentals and are driven by money managers willing to take great risks with the money of their institutional clients.

This attitude of selling while the markets are hot is not easy to develop and maintain. The bullish advice from Wall Street and many advisors is difficult to disregard. It takes discipline and a belief in the prudence of selling now to resist these siren calls.

Update on equity REITs

Back at the end of March, I wrote an in-depth article on the risks posed by equity REITs. I explained how all these REITs had plunged during the bubble collapse of 2008-2009. My goal was to show how the fundamentals did not support either the high P/Es of the major REITs or their share prices. I urged advisors to encourage their clients to unload long REIT positions to avoid a repeat of the bubble disaster.

What has happened since the article came out?

Let's first look at Vornado (VNO), a large REIT that owns office buildings and retail properties. Its share price had plunged from $130 to $26 during the post-bubble collapse. After clawing its way back, VNO shares climbed sharply last year as interest rates declined. I pointed out that the prices hit a peak of $115.7 in late January of this year. When my article appeared two months later, it sported a P/E ratio of 80. Because the fundamentals of the DC office market had weakened, I indicated that the share price was very vulnerable.

The share price has declined by 18% to $94.9 as of June 30. Because the fundamentals remain weak, it is still overvalued and subject to further price declines. I suggest selling VNO while you still have profits.

I also discussed General Growth Properties (GGP), another huge REIT that owned more than 100 domestic regional malls. I emphasized that its share price totally collapsed from $50 to 18 cents. That's right - 18 cents. By early 2015, it had managed to struggle all the way back to $31.70. That gave it a P/E ratio of 78 - nearly as lofty as Vornado. I warned advisors to get their clients out of this REIT as well. GGP shares have declined to $25.6 as of June 30.

The third REIT I discussed in that article is Simon Property Group (SPG). They are the largest REIT component of both the Vanguard REIT ETF (VNQ) and the iShares U.S. Real Estate Index (IYR). Like the other equity REITs, SPG shares plunged during the 2008-2009 collapse - from $111 to $22.

Although the firm has been heavily leveraged for years and had had a terrible 2013, investor euphoria reached truly excessive levels over the past two years. The share price hit $206.3 in January 2015. I indicated that the price of this REIT had also become unhinged from fundamentals and that prudent investors should unload their shares. Since that peak, the shares have declined by 16% to $172.9 as of June 30.

Finally, how has the most-actively traded REIT ETF fared? Shares of Blackrock's iShares U.S. Real Estate ETF (IYR) turn over entirely about once every seven days. It has become a tool of short-term traders.

In my previous article, I pointed out that like all other REIT investments, IYR shares plunged during the post-bubble collapse - from a high of $95 to $21. Similar to the major REITs, IYR peaked this year at the end of January - $83.5. Since then it has steadily declined and closed at $71.4 on June 30, down 15% from the January peak.

My warning about the excessive valuations of these REITs has been borne out by the share price action since then. While it is possible that these REIT investments could turn around, the safe play is to unload them before your profits disappear.

How do you know when to sell?

Real estate articles that discuss when you should sell often focus on the investor's time horizons. Is your goal to hold commercial property for five years, ten years or more? Should you avoid selling as long as there is a positive cash flow?

Rarely does the author take a serious look at the state of the real estate market. This continues to puzzle me. It is very likely due to the widespread consensus that the recovery is firmly in place. Why worry about a possible decline of prices when everyone knows that the worst is over?

There would be little need to think about market risks if this euphoria were based on something solid. However, as I have tried to show investors for several years, the bullish consensus about the real estate recovery is only a mirage.

Because this bullish consensus is still so pervasive with real estate and stock investors, it is very challenging to make the case for selling. Even a stock market analyst as thorough as John Hussman is reluctant to advise investors to sell everything. This may be due to the fact that stocks are so much more liquid than real estate. Except for very rare crashes, investors can change their minds and quickly get out of most stocks that are not thinly traded.

That is not the case with real estate. It takes months to get a property ready for sale. At the bottom of the collapse in the spring of 2009, there were a few months when bids on even good properties could not be obtained. Investors were simply unable to sell their property.

To unload real estate at a good price means selling before the market weakness becomes obvious. That requires bucking the bullish complacency and risking the scorn of friends, colleagues and advisers as well.

Dangers below the surface

When the lookout on the Titanic spotted the iceberg on the surface, he could not see the danger that lurked beneath it. That is the situation today with investors. Few of them are aware of the risks that are not clearly visible.

On June 10 of this year, USA Today published a very important article about risks in the stock market that most investors did not know. The author explained that a year ago, a mere 10 stocks in the S&P 500 were in bear markets - down more than 20% from their highs. When he reviewed things a year later, he was shocked to find that 100 stocks in the S&P 500 were down more than 20% -- a ten-fold increase. This was totally hidden from analysts who looked only at the index number alone.

Like the author of that article, I was also surprised by his revelation about the deterioration in the S&P 500, yet it also confirmed what I had been seeing in other indicators.

Risks that are not obvious are often disregarded by Wall Street and by investors. That does not make them less dangerous. The insidious thing about market risk is that during times of bullish euphoria, discussing them is often dismissed as fear mongering. My previous article - which I thoroughly researched and carefully explained - was described by one reader as "Jurow's rants."

Conclusion

Alerting investors that they are heading toward a cliff is especially important if they cannot see the cliff. The Titanic disaster is very apt for the lessons it teaches us. Although the lookout on the Titanic sounded the alarm, the ship was moving too fast to avoid the fatal impact. Why? Bruce Ismay - Chairman of the White Star Line who was traveling on the ship's maiden voyage - had rejected the idea of slowing down to safely steer through the ice field. He was much more interested in breaking the speed record for crossing the Atlantic Ocean.

The greatest risk facing the Titanic was that Ismay saw no danger in the icebergs that were known to be in the north Atlantic in April.

For several years, I have been warning investors in commercial real estate about the hollowness of the so-called recovery. These warnings have largely fallen on deaf ears because investors see signs of apparent strength - increasing sales and rising prices. The risk that underwater property owners might be unable to refinance close to $1 trillion in mortgages over the next 2 ½ years has been dismissed as unimportant and very unlikely.

My advice is to learn from the folly of Ismay aboard the Titanic. Lock in profits and preserve capital by selling before the iceberg is spotted.

Disclosure: None.