It's Time To Fix The Stock Buyback "Con Game"

Stock buybacks have hit record levels – but what's driving the growth is dangerous for you and our economy.

Total stock buybacks for 2014 amounted to $696 billion, or 4% of U.S. gross domestic product (GDP), according to Research Affiliates. That's a lot spent on a practice that used to be tightly regulated by the U.S. Securities and Exchange Commission because it was considered manipulative.

You see, even though they're common now, buybacks are manipulative. They make sense for some companies, but now they're often used to inflate stock prices – and make executives rich.

In fact, most of today's stock buybacks are not only unproductive for the long-term health of corporations, but destructive in terms of economic growth.

Here's how bad the stock buyback "con game" has become – and how we can fix it…

How Stock Buybacks Became "Good"

Companies used to not be allowed to buy back their shares in the open market. The Securities Exchange Act of 1934 implied large-scale stock repurchases by a company could be construed as an attempt to manipulate its stock price.

That was "fixed" in 1982.

Newly appointed SEC Chairman John S.R. Shad, a former vice chairman of E.F. Hutton & Co. who sat on 17 corporate boards, pushed through Rule 10b-18. This rule gives companies a "safe harbor" for buying back shares, meaning manipulation charges would not be filed if they followed certain purchase guidelines.

Now, not all stock repurchase programs are bad. They make sense if a corporation's earnings history is steady, if its future earnings prospects are good, and if its share price is currently undervalued.

The cost of buybacks should be weighed against a company's free cash flow (FCF). You find that by taking operating cash flow minus capital expenditures from fixed assets and cash dividends paid.

Apple Inc. (Nasdaq: AAPL) is a good example of a company that can justify massive buyback programs.

Apple has repurchased $56 billion of its own stock in the past 12 months. Even after that, Apple is still sitting on over $200 billion in cash. It has also raised its dividend out of its increasing free cash flow and spent $7 billion on capital expenditures in 2014.

Apple can easily argue its stock is undervalued since it's trading at a trailing price/earnings multiple of about 13.2. Competitors trade at much higher multiples. Google, now known as Alphabet Inc. (Nasdaq: GOOGL), trades at a PE of 35.7. The market trades at about 18.5.

But now companies repurchase shares because they're unable to organically grow earnings by reinvesting cash back into the business. When managers see declining return on capital from operations, or when they see no worthwhile mergers or acquisitions to grow core business lines, they turn to buybacks. They can financially engineer higher earnings per share without boosting gross earnings or net income.

Looking at their cash flow shows the unhealthy consequence of buying back too much stock…

This Ratio Is Creeping to a Dangerous Level

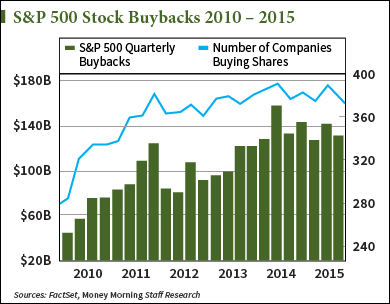

Since 2004, U.S. corporations have bought back more than $7 trillion worth of stock, according to the Academic Industry Research Network. The trend has accelerated over the past few years.

In just the second quarter of 2015, stock buyback value hit $134.4 billion, according to FactSet. For the trailing 12-month period buyback value totaled $555.5 billion.

The total buyback amounts are staggering – and what's more worrisome is where the money is coming to pay for them…

For the trailing 12-months ending in July 2015, free cash flow at S&P 500 companies totaled $514.4 billion, a 28.6% decline from the previous 12-month period. Companies' free cash flow in Q2 2015 was the lowest since Q3 2009.

As free cash flow has been falling, the buybacks-to-free-cash-flow ratio has been rising.

FactSet reported that the Q2 dollar amount of buybacks-to-FCF ratio exceeded 100%. That's the highest ratio since October 2009.

What's worse is when the dollar amount of buybacks exceeds a company's free cash flow, like it has lately, debt is issued to keep the buying binges humming along. And some corporations are going into serious debt to finance their stock buybacks.

According to The Wall Street Journal, in the first nine months of 2015, U.S. corporations issued $1.2 trillion of debt. Proceeds from some of the largest issuers, including Microsoft Corp. (Nasdaq: MSFT), Qualcomm Inc. (Nasdaq:QCOM), and Oracle Corp. (NYSE: ORCL), were "earmarked for share repurchases and dividends."

But buybacks are no guarantee that bid-up share prices will stay up…

Last year International Business Machines Corp. (NYSE: IBM) spent almost $20 million in buybacks when its stock was around $190. And whatever IBM spent in 2015 has been a total waste of money. Its stock is trading around $138 now.

Exxon Mobil Corp. (NYSE: XOM) spent $13.2 billion on buybacks in 2014, when its stock was in the mid-$90s. Whatever it spent in 2015 so far hasn't helped the stock, which traded below $70 a couple of weeks ago, and is only back up around $83.

And since companies are wasting billions on buybacks in the later stages of an extraordinary bull market, they pay increasingly higher prices for their shares.

This is money that could go to employees and to business growth. Instead, it drives only short-term gains. This at a time when economic growth has been averaging an anemic 2.4% and most of the employment gains have been part-time and low-wage jobs.

But they continue because of who is benefiting the most from record-high stock buybacks…

CEO Compensation Drives the Stock Buyback Con

Some corporate executives have been increasingly demanding about getting compensation packages based on stock issuance and stock option grants, and less on salary.

The Harvard Law School Forum on Corporate Governance and Financial Regulation recently published a report that stated, "Stock awards continue to increase their share within the pay mix, while other compensation components, such as base salary, annual bonus and stock options, are going in the opposite direction. According to 2014 disclosure, stock awards represent 42.3 percent of CEO pay at the average S&P 500 company."

That means higher share prices can trigger fat payout packages.

Remember SEC Rule 10b-18? According to a 2014 Harvard Business Review piece titled "Profits Without Prosperity" by William Lazonick, "because (under Rule 10b-18) corporations aren't required to disclose daily buyback activity, it gives executives the opportunity to trade, undetected, on inside information about when buybacks are being done."

In other words, through aggressive open-market buying, executives can lift share prices and sell their shares at advantageous prices.

Plus, another SEC rule change in 1991 further enriched corporate masterminds of the buyback game.

Previously, executives who exercised their options and bought stock (below current market prices) had to hold the stock for six months or pay "short-swing" gains if they sold before six months. The new allowance let top executives sell their new stock from options grants immediately without penalty gains – reinforcing their interest in higher stock prices.

The reason boards of directors allow this and encourage it is because most boards are stacked with corporate executives from other companies who all play the same game of "buyback shares to increase our compensation." Con-gamers justify each other's excessive compensation packages by publicly spinning the "peer group benchmarking" mantra. That argument postulates that CEOs and top executives have to be compensated based on what peers make, otherwise top talent will gravitate to where they are paid the most.

The stock buyback con game doesn't have to continue. There is a better way.

How to End the Stock Buyback Con Game

Here's what I propose:

- For starters, a bipartisan Congressional panel, including academics and labor executives (but not the pandering SEC), should study what buybacks have done to corporations, shareholders, capital formation, and the U.S. economy, since at least 1991.

- Academic economists and labor representatives should have seats on boards and be included in executive compensation committees.

- Shares created out of exercised options grants should be calculated into EPS metrics and transparently enumerated on all quarterly and annual reports.

- Quarterly and annual reports should include how many shares executives sell at what average prices, and how many shares were bought back at what average prices, on a daily basis.

- Short-swing profit rules for executives selling stock garnered from exercised options grants should be restored.

- The tax code should be changed.

Instead of wasting money on buybacks, corporations should be encouraged to pay more dividends. Paying regular dividends makes stocks better investments in the long run. Dividends can be reinvested into more shares, or invested elsewhere and compounded, no matter what the stock price does over a long-term holding period.

To do that, corporations should be allowed to deduct from taxable income the cash dividends they pay to shareholders.

Further, why not eliminate any tax on dividend income for individuals, or joint-filers, with gross income of less than $100,000? That would encourage average Americans – who desperately need better retirement options – to invest in stocks that pay steady dividends. This would have the added benefit of applying more discipline on corporate managers.

The Bottom Line

Today's stock buyback con game is nothing more than an extraordinarily egregious corporate executive perk. Buybacks don't make corporations stronger, don't extend anywhere through the economy or to workers who don't get options grants, and are a waste of what could be otherwise smartly applied capital.

It's time to blow the whistle on the game.