Inflation Or Deflation? And How To Cope With Both

I’ve been thinking about the problem of increasing inflation, and preparing for it. Here’s a run-down of the major asset classes, and how they typically respond to inflation (or have been responding to rising rates and inflation fears lately).

Bonds – except the shortest term bonds or the most cash-like bonds – their value declines because they’re paying a fixed dollar return and, sort of by definition, are not keeping up with inflation. But short term bonds and cash are decent choices. Short term bonds and cash instruments like money markets just tend to pay higher and higher interest rates when rates are going up. In our own portfolios, we use short-duration bonds, floating rating investments and CD’s for liquidity needs as they mature quickly to capture new, higher rates when rates move up.

We’re seeing those yields move up now as the yield on the 2-year US Treasury is up to 2.5% or so. That doesn’t sound like much, but it’s a huge jump from where it was a year or two ago TIPS (Treasury inflation-protected bonds)also protect against inflation. Their principal gets adjusted according to the consumer price index (CPI), which is the main indicator of inflation.

Stocks tend to produce better-than-inflation returns over long periods of time, but not necessarily when inflation is running at its highest clip, and not necessarily from high starting valuations (such as we have now). Stocks didn’t do well in the 1970s, for example. Over time companies pass through higher costs, but that’s not always reflected in the stock prices immediately. That’s because higher interest rates tend to send all financial asset prices down. And that’s probably why the stock market has been more volatile this year.

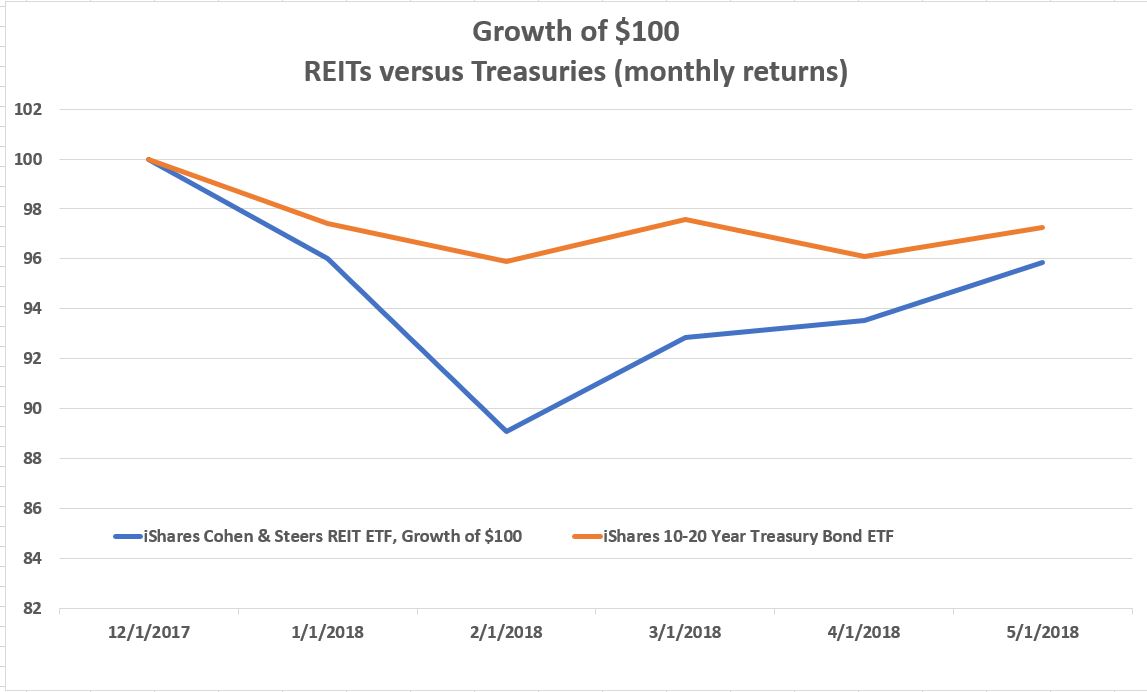

REITs act mostly like stocks in the long run. (And they are, in fact, stocks or ownership units.) They will pass through the higher costs over time by charging higher rents, but that won’t necessarily be reflected in stock prices immediately. And the truth is we’ve already had a lot of rent inflation since the financial crisis that hasn’t been captured in the official inflation numbers in my opinion. Residential rents have been skyrocketing for a long time now. They’ve been in such a long cycle that they are actually slowing down a lot in NYC and SF. I think REITs are just to expensive now, and they are reacting badly this year to inflation fears. They’ve tended to trade more like long-term bonds in recent years, which they do from time to time, and have faltered every time rates have moved up this year. That doesn’t bode well for how they might perform if we get higher inflation. Early this year, when rates were moving higher (inflation fear), REITs stumbled badly. Only when rates stopped going up, did REITs recover a bit. The following graph shows that REITs have been more volatile than Treasuries, but have moved somewhat in line with them this year.

That leaves commodities. In standard asset allocation models, around 5% of the portfolio in normally allocated to commodity type funds. However, over time, commodities don’t do so well though, so manage commodity exposure very carefully. A bet on commodities is, in some sense, a bet against human ingenuity, after all.

Last, keep in mind the economy is still kind of tepid, despite the very low unemployment numbers. The Labor Force Participation Rate is low, and middle class incomes aren’t rising. The most interesting question is whether we’ll get deflation because of a sluggish economy (and we haven’t had a recession in a while) or inflation because of the reasons you state – a lot of money printing, growing deficits, and tariffs. We have to be prepared for different scenarios, and we’ve structured the portfolio to withstand a variety of outcomes.