Inflation Monitor – December 2016

We have a lot to cover this month in the Inflation Monitor – December 2016. This is the end of 2016. It is a time for reflection for the year past and for pontificating the future. We all know no one can predict the future. And so much is up in the air with the recent populous trend changes, let’s focus on last year.

Let’s start with the US presidential elections. Donald Trump will be our next president (#45) in the US. Some people are happy, and others are sad. Regardless, we have a huge potential shift in the US with the results of the presidential election finalized. The first thing to address is that Trump may or may not pursue the same policies he campaigned on. Every presidential candidate has their platform, but not all of the promises actually happen. Let’s put these in the wait and see category up for discussion after his first 100 days. He will have about 100 days to prove his worth and keep the positive (market-related) momentum going.

While I have seen a lot of positive signs since Trump was elected, the US is overdue for a recession. The S&P 500 had a string of 5 quarters in a row of declining earnings. Apparently, no one noticed. I would consider this a recession, but the markets did not. The markets are always right regardless of what I think. It will be interesting to see what happens once the “new president smell” wears off.

I talk a lot about inflation and deflation in the US and on global scale. There has been a noticeable shift in the past few years from economic expansion (i.e. globalization) to a contraction (i.e. protectionism). This was prior to Trump’s election and may have contributed in part to his popularity. It is clear that the people are fed up with the global elites and globalization (at the expense of the people our politicians claim to represent). It is not just here in the US, but also in Europe. The more recent Italian referendum, which could be a potential problem for the Italian banks, and the UK Brexit show that the citizens of other countries also have the same disdain for their political elites.

People are not happy with their governments selling them out for foreign trade deals which could cause further harm domestically. In the US inflation has been an aggregate of 50% since 1998 and yet our real median household income has not changed at all. In almost 20 years, real income in the US has not changed. This means that we are no wealthier today than we were 19 years ago. The problem is that this does not impact the wealthy, it impacts people on the margins. The poor and the shrinking middle class are affected the most.

The problem is that this does not impact the wealthy, it impacts people on the margins. The poor and the shrinking middle class are affected the most. If a family is just making ends meet and their health insurance costs rise 30%-40% or more as we will see in 2017. How will that affect their disposable income? Quite a bit.

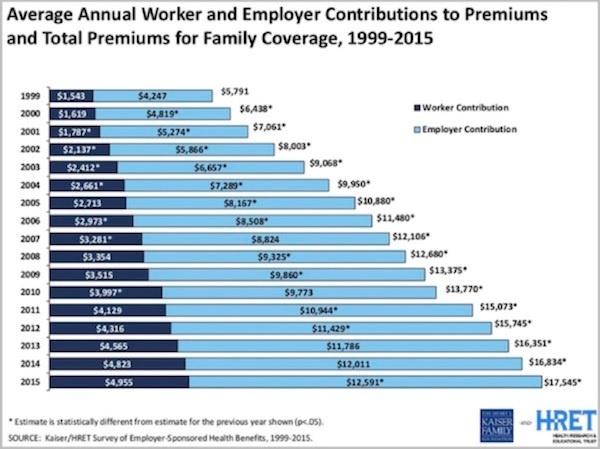

I discussed this problem of our health care system and a potential solution in my last post, A Simple Solution to America’s Health Care Crisis. Since that post was purely data and politics, here are some facts that need to be addressed. The nationwide average increase for health insurance will be 9%. If you live in these states, you are above average: CT 25% increase, TN 62% increase, OK 42% increase. This is just the rates you would pay. The choices are another matter entirely.

Proponents of Obamacare (ACA) claimed there would be a lot of competition and choices. Well in addition to the huge increase in the cost of health insurance, many states also have fewer choices. Nationwide, there are 650 counties with only one insurance provider. In 2016 this number was 225. Personally, I don’t count one insurance provider as a “choice”. That is a monopoly. There is even a county in AZ that had no providers.

Yes, you read that correctly. One county had no providers of health insurance. So in case you are not up to speed, the IRS mandates that you are required to pay for health insurance. If you don’t have health insurance, then you will pay a tax penalty. I don’t think this is what our founding fathers had in mind when they used the word “freedom”.

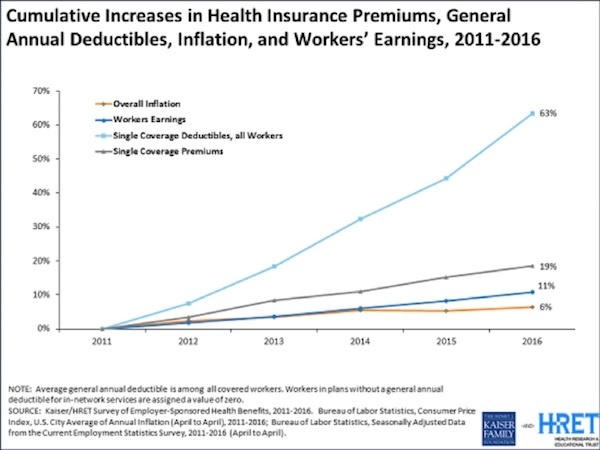

In the past 6 years, insurance premiums rose 3x faster than the rate of inflation. Insurance deductibles have risen 10x faster than inflation. This is in relation to median income which is flat since 1998. Is there any wonder people are mad? Is there any wonder why populism is taking hold in the US and around the world? I’m not surprised. I’m actually surprised it took this long to appear.

If you read my post, you will understand that this system doesn’t work. You cannot charge people for “insurance” on daily costs. Insurance is for large unexpected expenditures, not for common events. Consider my example of having house insurance that covers changing new lightbulbs.

The fact is that the Obamacare law is a mess and made the situation worse in many ways. However, the inflation in health care costs is a real problem. There is no easy solution if you want innovation and progress in medical advancements. In the words of Alan Greenspan, “I don’t know how this is going to resolve, but there’s going to be a crisis.” Even Bill Clinton acknowledges the problem, “You’ve got this crazy system where all of a sudden, 25 million more people have health care, and then the people that are out there busting it – sometimes 60 hours a week – wind up with their premiums doubled and their coverage cut in half.“

Health care in the US is a big problem with the fastest acceleration to a tipping point. Social security is also a problem, but the end game can be pushed much further out, which most politicians tend to do.

Getting back to the inflation-deflation debate…

President-elect Trump needs to make good on some of his campaign promises rather quickly to keep the optimism going. If he does this by pursuing protectionism, thus reversing globalization, this will be inflationary for the US. Globalization is by nature deflationary, so the reverse of this is inflationary. While only a few may balk at the benefits of globalization, if we need inflation, this is one natural path to get it. Of course, this will also cause other problems, such as trade wars, higher domestic prices without equally higher wages, etc. If you are looking at trends, this is one you should keep a close eye on.

Lastly, If you are not aware of the pension crisis we are heading into, you should read up on it. Here is a story I saw recently about the Dallas Police and Fire pension plan. This pension plan allowed a lump sum withdrawal from the plan. In August the board proposed pension benefit cuts so the pensioners exercised their right to take a lump sum withdrawal. After 500 million was taken out, they sought to freeze future withdrawals or they would not have enough to support the plan. While I’m sure there is enough blame to pass around, this is not a unique situation. Public pensions around the country are in danger of not meeting their pension promises. This could be a blog post in itself, so I’ll only go as far to say that much of this problem has to do with low-interest rates. If the pension expects 7.5% and it only gets 3% returns, then the pension will be underfunded. If you have a public pension that you can take as a lump sum, then I highly suggest you consider that option. You can always create an annuitized income stream with the insurance company of your choice.

This article is intended solely for informational purposes only, and in no manner ...

more