Heightened Volatility A Result Of The Change In The Earnings Growth Rate

Investors are experiencing a market exhibiting a higher level of volatility. This heightened volatility is more normal than the lack of volatility experienced in the few years leading up to 2018 and yet the S&P 500 Index is down less than 2% this year.

Including the last two months of 2017 (November and December) the S&P 500 Index is up just less than 2%. Given some of the financial commentary, one would think the market is down significantly.

Admittedly, I do not have the so-called magic eight ball that provides all the answers; however, some aspects of the market and economy seem to support higher prices ahead. Our firm believes one factor that might be taking place at the moment is the market adjusting to a lower level of earnings growth versus the 20+% growth expected now. The equity market does a pretty darn good job of anticipating and adjusting to earnings growth expectations. As a result, we sometimes tell our clients stock prices tend to follow earnings expectations. As the below chart shows, after the passage of the Tax Cuts and Jobs Act, which largely benefited businesses via lower corporate taxes, the forward or expected earnings growth rate for the S&P 500 Index increased from 9.2% to 20.5% in a few short months.

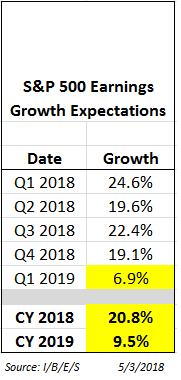

With this spike in the growth rate at the end of 2017, the S&P 500 Index was up nearly 8% at its high in late January. As this earnings excitement wears off, the market ist seems to be adjusting to a more normal low double-digit earnings or high single digit growth rate. As the shaded area on the above chart shows, when the change in the earnings growth rate is negative, i.e., decreasing from 20.5% to 9.5%, the equity market tends to struggle. Below is the anticipated quarterly earnings growth rates along with the calendar years 2018 and 2019. The market tends to look out one year and that puts us at the first quarter of 2019 and earnings growth is expected to equal 6.9% in that quarter.

The one positive today is the fact companies will benefit from a higher earnings level as a result of the cut in the corporate tax rate. It is the higher rate of change that is a one-time event. At least a portion of the excess earnings resulting from the lower tax payments is likely to find its way into the economy via increased capital expenditures over a multi-year period. This higher level of activity, along with a reasonably strong consumer, should benefit stocks in the balance of this year.

Disclosure: None.