I’ve been yapping my trap about these vol-selling monkeys for some time—we may have finally reached peak vol absurdity.

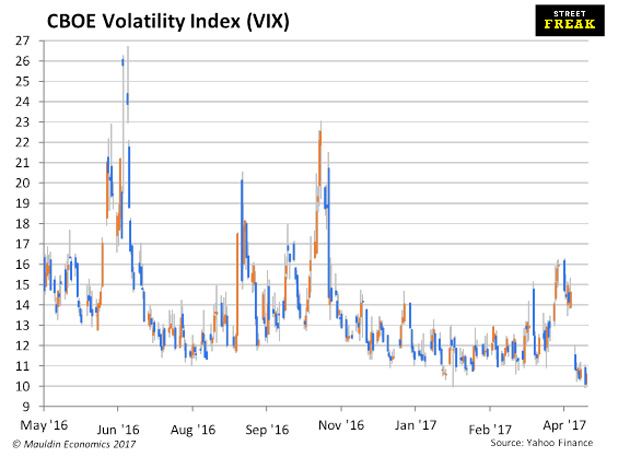

As you may have seen, the VIX dipped under 10 on an intraday basis the other day:

Meanwhile, short interest has reached an all-time high in VXX, the ETN that is supposed to track the VIX.. Remember, if you buy VXX you are getting long volatility, so basically what we are seeing is an overabundance of people rushing in to sell volatility… at the all-time lows.

Source: Zerohedge

No bubble here.

We spent last week talking about bubbles—is there a bubble in short volatility strategies? I think there might be.

Please stop and read this terrific piece by Dean Curnutt, CEO of Macro Risk Advisors, on Bloomberg View. In it, he talks about the idea that financial insurance is different than conventional insurance. With insurance against hurricanes or fires, for example, the event you are trying to insure against is truly exogenous. Hurricanes (for all intents and purposes) are independent events, and occur without respect to how many people buy insurance.

But that is not the case with financial markets insurance (like options). As opposed to earthquakes, which are exogenous events, a crash (caused by a rapid unwinding of positions) can be an endogenous event, as Curnutt explains. People put on a trade, it works, which encourages more and more people to pile in… until it eventually stops working. Then everyone will want to get out—all at once.

As I have written before, selling volatility has worked so well for so long that many people believe it to be free money. Shorting VXX works when volatility goes down and the term structure of volatility steepens. What happens if volatility goes up and the term structure inverts—and stays inverted? Road pizza.

I try not to bring this up in mixed company, but this is just one of many dashboard warning lights that are flashing magenta right now. The other ones I talk about all the time are overheated housing markets in Canada, Australia and Sweden—it appears that Canada is cresting as we speak. But what I really want to talk about is the idea that we might possibly have an indexing bubble.

Is There An Indexing Bubble?

Everyone knows by now that assets have been fleeing actively managed funds into passively managed mutual funds and ETFs. It’s an old story. Everyone knows about the popularity of Vanguard. Some people have made their reputations on this. The story is compelling—invest in this product that usually beats most competitors but costs a lot less. Where do I sign up?

I’ll poke holes in that logic some other time. For now, I want to talk about the idea that this strategy has become so popular that it is a bubble in and of itself. This is a frequent topic of discussion online. The index fund bulls/promoters usually point out that just a small fraction of assets have switched to passive—there could be a lot more to go. That is true. The index fund bears/detractors point out all the distortions that are happening from indexing, like:

- It has ruined long/short strategies

- It is screwing up corporate governance

- It is causing valuation distortions

Entertain this thought for a moment. If you lived through the dot-com crisis, you remember what that was like. People day-trading at their desks at work, cab drivers giving you stock tips, all that kind of stuff. Mania. The stuff we were talking about two weeks ago.

What if indexing is a mania unto its own?

Clearly, there isn’t the euphoria there was in 1999, but people are pretty excited about their index funds. Excited enough that Vanguard gets $2 billion in new assets a day. Meanwhile, long-short guys have a tough time scratching together $50 million for a launch.

People aren’t bullish on stocks--they are bullish on the stock market. And philosophically, nobody is really thinking about the S&P 500 stocks as 500 stocks. They are thinking about it as an asset unto itself. It has a price. And, when people talk about indices, they don’t talk about the benefits of diversification anymore.

Remember how this stuff works—you don’t necessarily need an exogenous shock for this trade to fall apart. As previously described, greed takes over, and it can just stop working and unwind.

What would an indexing unwind look like? Down 20%--thought you were diversified!

Disclosure: Follow Mauldin as he uncovers the truth behind, and beyond, ...

more

Disclosure: Follow Mauldin as he uncovers the truth behind, and beyond, the financial headlines in his free publication, Thoughts from the Frontline. The publication explores developments overlooked by mainstream news to help you understand what’s happening in the economy and navigate the markets with confidence.

The article was excerpted from John F. Mauldin’s Thoughts from the Frontline.

Copyright 2016. Follow John Mauldin on Twitter.

The article How Big the Gig Economy Really Is was originally published at mauldineconomics.com.

To subscribe to John Mauldin's Thoughts from the Frontline e-newsletter and a selection of other free newsletters, please click here:& ;http://www.mauldineconomics.com/subscribe

To change your email address, please click here: http://www.mauldineconomics.com/change-address

Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Millennium Wave Advisors, LLC MWA which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC MWA, which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.

less

How did you like this article? Let us know so we can better customize your reading experience.