Data Suggests More Upside

Coming off a weekend of political disappointment, it’s easy to get caught up in the emotions of it all. As I pointed out, the market was due for a pullback, and it got a reason to. We can “beat a dead horse” and dissect all of the “what-if” scenarios and implications of the failure. But none of this will be fruitful for your investment decisions. We know that pullbacks and corrections are an inevitable part of investing. And once in awhile we get a major decline, usually due to a recession. The key question is does the data suggest a business cycle peak?

The short answer is no.

(Click on image to enlarge)

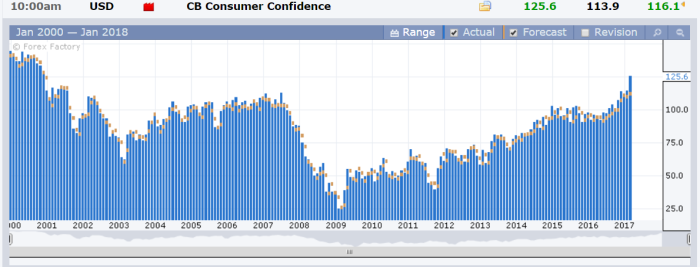

Consumer confidence numbers just came out at a high not seen since November 2000.

(Click on image to enlarge)

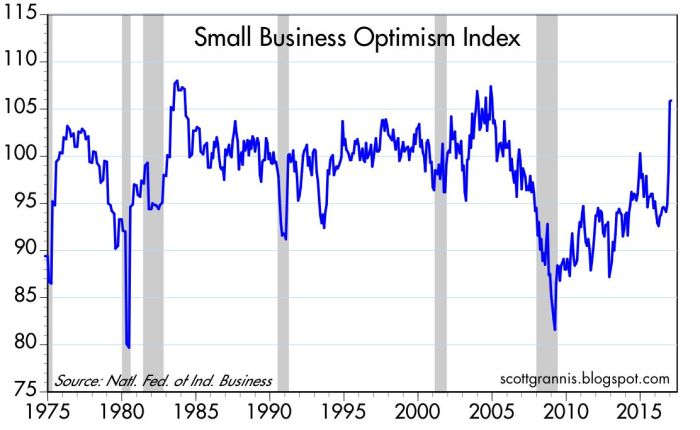

Scott Grannis points out that Small Business Optimism has soared post election and is near all time highs.

(Click on image to enlarge)

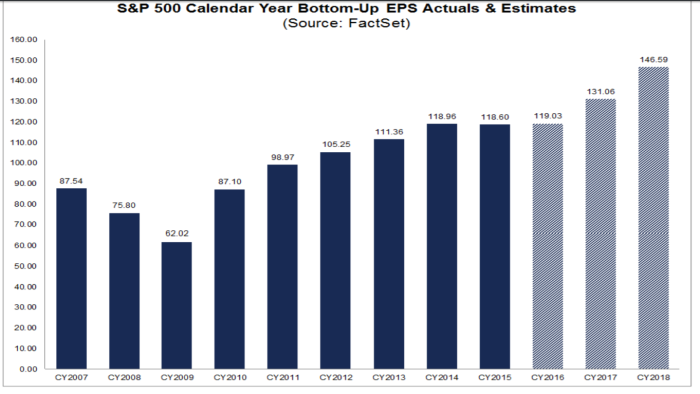

Earnings growth is finally back and is projected to be around 9-11% for 2017. This would be the largest annual increase in earnings since 2011. And this doesn’t even factor in the potential for tax reform and repatriation.

And interest rates are still very low. The earnings yield on the S&P 500 is currently 5.59%, while the 10 year treasury bond yield sits at 2.38%. Even the Fed’s overly optimistic projection suggests the real Federal Funds rate won’t even turn positive until another two years or so. So, even though valuations are on the high side and interest rates have risen quite a bit post elections, stocks still present an attractive risk premium.

(Click on image to enlarge)

An interesting chart to follow going forward is the ten year yield. Post election the 10 year yield has risen on the assumption of pro-growth policies of the new administration. Since then a trading range between 2.3% and 2.62% has been formed. An upside breakout suggests all is clear, while a breakdown suggests that more of the President’s agenda may be in jeopardy.

Time will tell. But for now, things are looking pretty good to me. But I parse this by saying we’re probably closer to the end of the bull market, than we are to the beginning. The stock market and the economy don’t always correlate. We’ve had great performance in stocks over the last 8 years, while the economy largely under-performed. I wouldn’t be surprised if, going forward, we experience a situation where the economy starts to outperform, while stock performance slows down to an eventual crawl.

The great thing about diversification and asset allocation is that we don’t have to be prophetic. We stick to our strategy and re-balance when necessary. It’s that simple, but certainly not easy.

Disclosure: None.

Nothing on this article should be misconstrued as investment advice. Trading and ...

more