Changing Expectations And The S&P 500 In Week 2 Of November 2018

Seven trading days into our redzone forecast for the S&P 500, and so far, it's holding, with the closing value of the S&P 500 (Index: SPX) falling within our target range on six of seven of those days.

(Click on image to enlarge)

The trajectory of the S&P 500 has also been consistent with our unadjusted standard model's projection associated with the expectations that investors have for 2019-Q1 in setting today's stock prices during this period. Since that trajectory reflects the echo of the volatility that stock prices experienced in October 2018, which arises from our model's use of historic stock prices as the base reference points from which it projects potential future stock prices, we had developed the redzone forecast to compensate for its effect. Our redzone forecast assumes that investors will largely keep their forward looking attention on 2019-Q1.

Just because we've assumed that will happen does not mean that it will. It is possible that investors may shift their attention toward other points of time in the future.

Speaking of which, the large decline in oil prices and growing signs of economic slowdowns elsewhere in the world have greatly influenced investor expectations during the last two weeks, particularly where the future for interest rate hikes by the Fed are concerned.

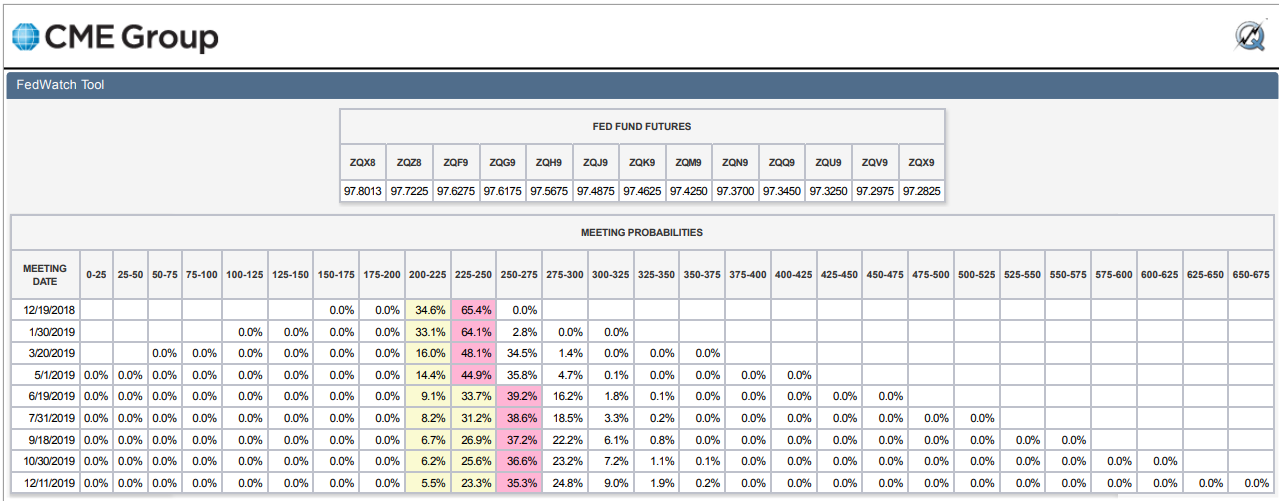

Back then, investors were confident in their expectations that the Fed would hike its Federal Funds Rate by a quarter point in December 2018, in March 2018 and were giving just over a 50% chance they would again in September 2018.

But now, they appear to be backing off those expectations, where they would appear to now anticipate quarter point rate hikes in December 2018 and just one more in 2019, in June, according to the CME Group's FedWatch tool.

(Click on image to enlarge)

Meanwhile, the news headlines of the past week suggest that some influential Fed officials are backing off plans to steadily hike U.S. short term interest rates into 2019, which accounts in part for those changing expectations....

Monday, 12 November 2018

- Oil prices rise by 1 pct after Saudi announces Dec. supply cut

- China stimulus: China will step up tax cuts: finance minister

- Fed's Daly says too soon to know if December rate hike needed

- Wall Street tumbles, S&P falls as much as 2 percent

Tuesday, 13 November 2018

- Oil slumps 7 percent to one-year low as rout extends to 12 days

- S&P, Dow lose ground as crude plunge punishes energy stocks

Wednesday, 14 November 2018

- Oil rebounds from steep sell-off as OPEC, partners discuss supply cut

- U.S. consumer inflation rises; oil prices may slow momentum

- Fed's Powell says press conference at every meeting means all sessions are 'live'

- S&P 500 falls for fifth day as financials drag

Thursday, 15 November 2018

- Oil rebounds on lower U.S. stockpiles, possible drop in OPEC supply

- Fed plans review of how it pursues inflation, employment goals

- Wall Street climbs on hopes of easing trade tensions

Friday, 16 November 2018

- Oil edges up in volatile session but falls for sixth straight week

- China stimulus: Weak credit growth raises odds of first China rate cut in years

- Trump says U.S. may not impose more tariffs on China

- Fed nods to concerns but still sees U.S. rate hikes

- S&P, Dow advance on trade optimism; Nvidia sinks Nasdaq

For a broader picture of what happened in the week that was, Barry Ritholtz found five positives and five negatives among the week's major economy and market-related events.

Disclaimer: Materials that are published by Political Calculations can provide visitors with free information and insights regarding the incentives created by the laws and policies described. ...

more