Can Pepsi Beat On Its Q4 Earnings? Here’s What To Watch

Photo Credit:Peter Bond

PepsiCo, Inc. (PEP) Consumer Staples - Beverages| Reports February 11, Before Market Opens

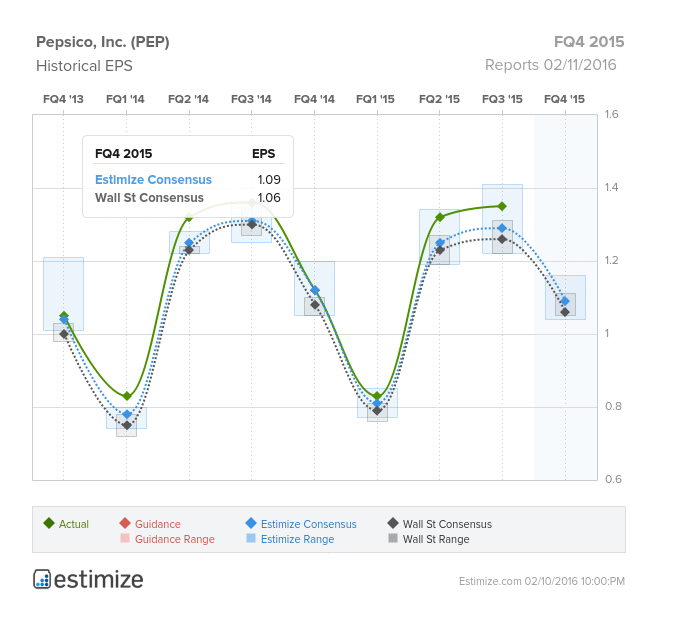

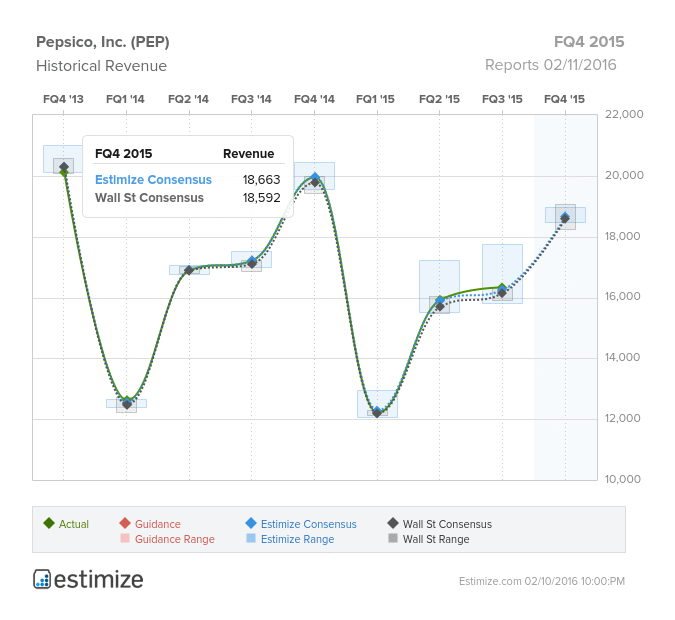

PepsiCo is scheduled to report fourth quarter earnings before the bell on February 10. The soft drink maker is coming off yet another strong quarter of earnings despite a higher than expected impact from currency headwinds. In fact, the company has beat bottom line estimates each of the past 8 quarters. That said, expectations for this quarter are low as beverage sales volume continues to shrink due to the stronger dollar, increasing volatility in emerging markets and a shift in consumer preferences for healthy alternatives. The Estimize consensus is calling for EPS of $1.09 and revenue of $18.663 billion, slightly higher than Wall Street’s estimates of $0.06 and $18.592 billion. Compared to Q4 2014, this represents a projected YoY contraction in EPS and revenue of 2% and 5%, respectively. With around half of its revenues coming from overseas, Pepsi’s sales and profits have been significantly impacted from global volatility. The strength Pepsi’s snack business is expected to help soften the blow from poor international performance.

Growing health concerns have put a damper on PepsiCo’s carbonated drink sales growth. The soda industry has been under pressure as health conscious consumers opt for alternative beverages that do not include sugar or artificial sweeteners. Although Pepsi has increased marketing investments to boost its beverage business, these efforts have yet to result in any meaningful improvement. Moreover, Pepsi expects to continue to face macroeconomic headwinds due to weaker international currency and an economic slowdown in emerging markets. Sales in Latin America, a major PepsiCo market, have largely been stagnant as these countries head into a recession. In the upcoming quarters, currency movements are expected to impact PepsiCo’s top and bottom line by 8%.

Offsetting some of the losses, PepsiCo’s snack business, Frito-Lay, is expected to ring up sales and volume growth. Among all of PepsiCo’s brands, Frito-Lay has been the only segment to consistently turn a profit. Lately, the snack business has been almost twice as profitable for Pepsi than beverages. Besides potato chips, the company is expanding its health brands to meet changing consumer preferences. PepsiCo has shown a propensity to expand and adapt to changing times and notwithstanding weaker macroeconomic conditions, the company could surprise investors.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.